Why parametric insurance fits DeFi

Decentralized finance operates at a speed that traditional indemnity insurance simply cannot match. When a smart contract exploits or a protocol suffers a technical failure, the window for recovery is measured in minutes, not months. Traditional insurance models are built on subjective loss assessment and lengthy claims processes. By the time an adjuster verifies the damage, the capital is often gone, and the ecosystem has moved on. This friction makes indemnity coverage impractical for the high-stakes, high-velocity nature of DeFi risk transfer.

Parametric insurance solves this timing problem by removing the need to prove loss severity. Instead of waiting for an investigation, payouts are triggered automatically when a specific, pre-defined event occurs. As noted by Aon, this model is a "simple, straightforward and fast-paying risk transfer solution" that relies on objective data points rather than subjective judgment. In DeFi, this means a smart contract can release funds the moment a price oracle drops below a set threshold or a bridge contract is compromised, providing immediate liquidity to mitigate further damage.

The core value proposition here is transparency and speed. Because the trigger conditions are coded into the smart contract, the payout logic is visible to all participants. There is no hidden adjuster discretion or ambiguous policy language to dispute. This aligns perfectly with the ethos of decentralized systems, where code is law and outcomes are deterministic. For high-stakes assets, this certainty is not just convenient—it is essential for maintaining trust and stability in volatile markets.

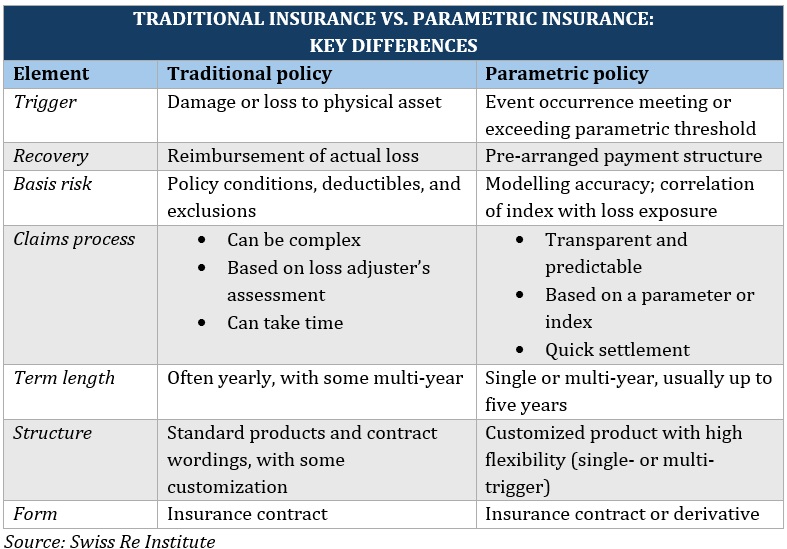

This approach expands coverage beyond physical assets to fill protection gaps left by indemnity insurance, such as deductibles, excluded perils, or scarce resources, as highlighted in Swiss Re's comprehensive guide to parametric insurance. For DeFi protocols, this means they can secure coverage for specific technical failures or market anomalies that traditional insurers might view as too unpredictable or complex to underwrite using conventional methods.

Designing effective onchain triggers

Building a parametric insurance strategy for DeFi risk transfer relies entirely on the precision of its triggers. Unlike traditional insurance, which requires lengthy claims processing and damage assessment, onchain parametric policies execute automatically when predefined conditions are met. The mechanics of this system hinge on two pillars: selecting reliable data sources (oracles) and defining clear, immutable parameters. When these elements align, the policy reduces basis risk—the gap between the trigger event and the actual financial loss experienced by the user.

Selecting Reliable Oracles

The oracle is the nervous system of any parametric insurance contract. It feeds external data into the blockchain, determining whether a payout occurs. If the oracle is compromised, delayed, or manipulated, the insurance becomes worthless. For DeFi protocols, the most common triggers involve price drops or liquidity pool imbalances. Therefore, the data source must be robust enough to withstand market volatility and potential manipulation attempts.

Using multiple oracle feeds can mitigate single-point failures. For example, a protocol might aggregate price data from Chainlink and Pyth Network to ensure accuracy. This redundancy ensures that a temporary glitch in one feed does not trigger a false payout or, worse, fail to pay out during a genuine crisis. The goal is to create a data stream that is as immutable and transparent as the smart contract itself.

Defining Immutable Parameters

Once the data source is secured, the next step is defining the trigger parameters. These are the specific thresholds that activate the insurance. Common parameters in DeFi include:

- Price Drops: A token’s price falling below a certain percentage within a specific time window.

- Gas Spikes: Average transaction costs exceeding a set threshold, indicating network congestion.

- Exploit Detection: A sudden, anomalous change in a contract’s state variable, such as a massive token transfer.

These parameters must be immutable once the policy is deployed. Changing them mid-contract would introduce uncertainty and potentially allow the insurer to avoid payouts. Clarity is paramount; the trigger should be binary—either the condition was met, or it was not. This eliminates ambiguity and speeds up the claims process to milliseconds.

Mitigating Basis Risk

The greatest challenge in designing onchain triggers is basis risk. This occurs when the trigger event does not perfectly correlate with the user’s actual loss. For instance, if an insurance policy is triggered by a general market crash but the user’s specific asset remains stable due to unique fundamentals, the user may still suffer losses elsewhere without receiving the payout. Conversely, a trigger might activate even if the user’s specific position was unaffected.

To minimize basis risk, trigger design must be as specific to the user’s exposure as possible. Instead of a broad market index, insurers can use protocol-specific metrics, such as the health factor of a specific lending position. This precision ensures that the payout aligns closely with the actual financial impact, making the parametric insurance a more effective risk transfer tool. The following chart illustrates how a hypothetical price drop might trigger a payout event, highlighting the importance of precise threshold definition.

Top parametric insurance infrastructure

DeFi parametric insurance relies on a specific stack of smart contracts, oracles, and liquidity pools to function. Unlike traditional insurance, which requires lengthy claims assessments, these protocols automate payouts based on verified external data. The infrastructure ensures that coverage is transparent, immediate, and resistant to manipulation.

Nexus Mutual

Nexus Mutual operates as a decentralized mutual, allowing users to pool funds to cover smart contract failures. It uses a combination of on-chain data and community consensus to determine payouts, making it one of the most established players in DeFi risk transfer. Users buy coverage directly against specific protocols, with premiums determined by supply and demand dynamics.

Etherisc

Etherisc focuses on real-world assets, offering parametric coverage for flight delays, crop insurance, and solar energy production. By integrating with oracles that verify real-world events, Etherisc extends the utility of blockchain insurance beyond pure DeFi risks. Its infrastructure supports a wide range of industries, demonstrating how parametric models can apply to tangible global events.

InsurAce

InsurAce provides a multi-chain platform that aggregates coverage options across various blockchains. It emphasizes ease of access and a broad selection of underwriting options, allowing users to customize their risk exposure. The platform’s infrastructure supports rapid policy issuance and automated claims, reducing the friction typically associated with buying crypto insurance.

Bridge Mutual

Bridge Mutual functions as a peer-to-peer insurance protocol where participants act as both insurers and insured. It relies on a voting mechanism to validate claims, adding a layer of decentralized governance to the payout process. This model aligns incentives among participants, as the community directly benefits from prudent risk management and accurate claim validation.

| Protocol | Coverage Focus | Trigger Mechanism | Payout Speed |

|---|---|---|---|

| Nexus Mutual | Smart Contract Failure | Consensus + On-Chain | Days |

| Etherisc | Real-World Assets | Oracle Data | Hours |

| InsurAce | Multi-Chain Protocols | Automated Oracles | Minutes |

| Bridge Mutual | DeFi Protocols | Community Vote | Days |

Managing basis risk in coverage

Basis risk is the fundamental tension in parametric insurance. It occurs when the index trigger activates, but the policyholder does not experience a proportional loss, or conversely, when a significant loss occurs but the trigger fails to fire. In DeFi, this disconnect can manifest as an oracle reporting a price crash that didn't impact a specific user's hedged position, or a liquidity pool drain that falls just short of the protocol's predefined threshold. This mismatch undermines the core value proposition of parametric products: replacing complex loss assessment with instant, objective payout.

To mitigate basis risk, designers can employ layered coverage models. Instead of relying on a single binary trigger, protocols can stack multiple indices with varying sensitivities. For example, a DeFi risk transfer protocol might combine a global market cap drop trigger with a specific token pair liquidity pool depth trigger. This ensures that payouts occur across a broader spectrum of adverse scenarios, reducing the likelihood of a "false negative" where the user suffers damage but receives no compensation. Layering acts as a net, catching losses that a single, rigid trigger might miss.

Hybrid models offer another avenue for reducing basis risk by blending parametric speed with traditional assessment elements. A hybrid structure might use a parametric trigger for immediate, partial payouts to cover urgent liquidity needs, while a secondary, more granular assessment process handles the remaining claim value. This approach retains the speed benefits of parametric insurance for minor to moderate events while providing a safety net for complex, high-severity scenarios where basis risk is most pronounced. By acknowledging that no single index can perfectly capture every user's exposure, hybrid designs create a more robust risk transfer mechanism.

Steps to activate your coverage

Activating a DeFi parametric insurance policy requires precision. Unlike traditional indemnity claims that rely on loss assessment, these smart contracts execute payouts the moment a verified oracle confirms a trigger event. Follow this workflow to secure your position.

Navigate to a reputable DeFi insurance protocol. Connect your Web3 wallet to the platform’s interface. Ensure you are on the official domain to avoid phishing sites. Verify the network compatibility matches the asset you intend to protect.

Choose the specific cryptocurrency or liquidity pool you wish to hedge. Review the available coverage options, noting the maximum limit and the premium cost relative to the asset’s current value. The goal is to align the coverage amount with your actual exposure to volatility.

Set the specific conditions that will activate the policy. This involves selecting the oracle source and defining the threshold—for example, a price drop below a certain dollar amount or a specific volatility index spike. These parameters must be objective and immutable once the contract is deployed.

Review the smart contract terms and the calculated premium fee. Approve the transaction in your wallet. Once the blockchain confirms the payment, the coverage is active immediately. You will receive a digital receipt or NFT representing your policy position.

The accuracy of your payout depends entirely on the oracle used. Always verify which data provider the protocol trusts for price feeds or event triggers.

Frequently asked: what to check next

Understanding how parametric insurance works helps clarify its role in DeFi risk transfer. These answers address common questions about triggers, payouts, and market dynamics.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!