Parametric insurance market research limits to account for

Parametric insurance market research requires a sharp focus on data reliability rather than just market size. While global estimates suggest the sector could reach $63.8 billion by 2035, the real challenge lies in verifying the underlying data oracles that trigger payouts. Unlike traditional indemnity insurance, which relies on loss assessments, parametric contracts depend entirely on the accuracy and integrity of external data sources.

When evaluating providers, prioritize those with transparent oracle networks. A gap between the trigger event and the actual payout often stems from poor data latency or manipulation risks. Look for firms that use multiple redundant data feeds and clearly define the index parameters in their policy wording. This due diligence ensures that the contract functions as a true risk transfer mechanism rather than a speculative instrument.

Evaluating parametric insurance choices that change the plan

Building a parametric insurance strategy requires balancing speed and certainty against basis risk and data integrity. Unlike traditional indemnity policies, these contracts pay out based on predefined triggers—such as wind speed, rainfall levels, or earthquake magnitude—rather than actual loss assessment. This structure eliminates lengthy claims processing but introduces specific vulnerabilities that risk managers must evaluate before deployment.

Speed vs. Basis Risk

The primary advantage of parametric coverage is liquidity. Payouts typically occur within days of trigger verification, providing immediate capital for disaster recovery when traditional insurance might take months. However, this speed comes with basis risk: the potential mismatch between the trigger event and your actual financial loss. For example, a hurricane might trigger a payout in a specific coastal zone while causing minimal damage to your inland facility, or vice versa. Evaluating the correlation between the index and your specific exposure is essential to ensure the product actually hedges your risk rather than creating a speculative position.

Data Source Reliability

The integrity of the payout depends entirely on the oracle or data source feeding the smart contract. If the trigger relies on weather station data, satellite imagery, or seismic readings, the choice of provider becomes critical. Errors in data collection, sensor malfunctions, or tampering can lead to incorrect payouts or failed claims. Risk managers should prioritize data sources with proven track records, transparent methodologies, and established legal standing. In the DeFi context, this often means selecting decentralized oracle networks with robust consensus mechanisms to prevent single points of failure.

Cost vs. Coverage Precision

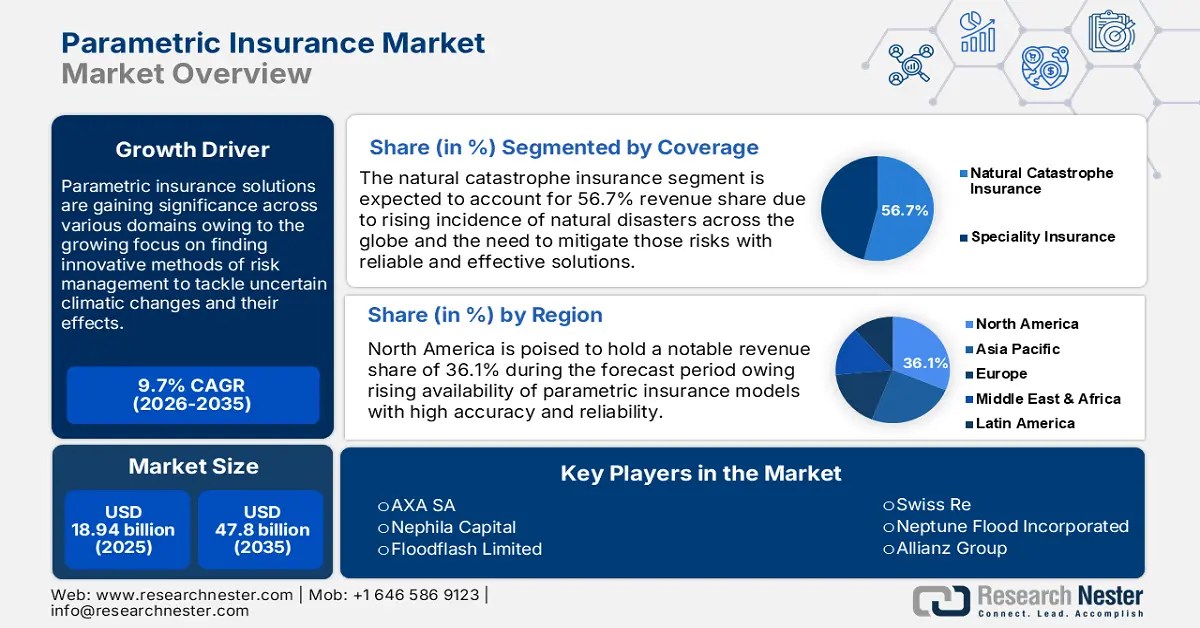

Parametric policies often carry lower premiums than traditional indemnity insurance due to reduced administrative costs and moral hazard. However, the coverage is binary or stepped, lacking the granular tail coverage that indemnity policies provide. You must determine if the fixed payout structure aligns with your financial modeling. Over-insuring triggers can lead to wasted premiums, while under-insuring leaves gaps in your balance sheet. The market is expanding rapidly, with global estimates suggesting growth from $19.4 billion in 2025 to over $63 billion by 2035, indicating increasing competition and product sophistication.

| Factor | Parametric | Traditional Indemnity |

|---|---|---|

| Payout Speed | Days to weeks | Months to years |

| Basis Risk | High | Low |

| Claims Process | Automated/Trigger-based | Loss assessment required |

| Premium Cost | Generally lower | Generally higher |

| Coverage Precision | Fixed/Stepped | Actual cash value |

Building a Parametric Insurance Decision Framework

Turning market research into a working strategy requires moving beyond general market size estimates to specific structural checks. The global parametric insurance market is expanding rapidly, with projections indicating growth from an estimated $19.4 billion in 2025 to $63.8 billion by 2035 [src-serp-2]. However, this growth reflects broad adoption trends, not necessarily suitability for every risk profile. A practical decision framework prioritizes three core components: trigger specificity, data oracle reliability, and DeFi integration mechanics.

1. Define Binary Trigger Conditions

Parametric insurance pays out based on predefined physical metrics rather than actual loss assessment. Your first step is to establish triggers that are indisputable and easily verifiable. Avoid vague conditions like "severe weather" or "market volatility." Instead, specify exact thresholds, such as wind speeds exceeding 120 mph at a designated weather station or a specific index dropping below a set value.

Clarity in triggers reduces basis risk—the danger that the payout does not match your actual financial exposure. If your crop fails due to drought but the trigger is rainfall volume, a payout may not cover your specific loss. Align triggers with the data sources you trust most to ensure the event is measurable and immutable.

2. Vet Data Oracle Integrity

The bridge between the physical world and the blockchain is the data oracle. Since payouts are automated, the oracle providing the input data becomes the single point of failure. Evaluate the oracle's source directly. Does it pull from a recognized meteorological agency, a regulated financial exchange, or a verifiable IoT sensor network?

Prioritize oracles with decentralized verification mechanisms. If a single entity controls the data feed, you reintroduce counterparty risk. Check if the oracle provider has a history of uptime and accuracy. In high-stakes scenarios, the cost of a failed payout due to oracle latency or error often outweighs the premium savings.

3. Structure DeFi Risk Transfer

Integrating parametric insurance with DeFi requires understanding liquidity and smart contract risk. Determine whether you will hold the policy directly on-chain or use a structured product. If using on-chain protocols, audit the smart contract code or rely on established, time-tested platforms. Liquidity is critical; ensure there is sufficient capital in the pool to cover potential payouts during extreme events.

Consider the tax and regulatory implications of holding crypto-assets as collateral for these policies. Unlike traditional insurance, parametric payouts may be classified as property or capital gains depending on your jurisdiction. Consult legal counsel to structure the wrapper or stablecoin holdings in a way that minimizes unexpected tax liabilities while maintaining quick access to funds when triggers are met.

Spotting Weak Parametric Insurance Options

The parametric insurance market is expanding rapidly, with the global sector estimated at USD 19.4 billion in 2025 and projected to reach USD 63.8 billion by 2035 [1]. This growth attracts many DeFi risk transfer strategies, but not all options deliver reliable protection. Buyers often encounter misleading claims about coverage precision or baseless assumptions about oracle reliability. Identifying these weak options requires a clear understanding of how triggers, data, and contracts interact.

The Basis Risk Trap

Basis risk occurs when the trigger index does not perfectly align with your actual financial loss. For example, a parametric policy based on regional rainfall might pay out even if your specific farm did not experience crop failure due to localized soil conditions. This mismatch is the most common mistake in parametric structuring. It creates a false sense of security while leaving the insured exposed to significant gaps. Always stress-test the correlation between the index and your specific exposure before committing capital.

Oracle Vulnerabilities and Data Integrity

DeFi-based parametric products rely heavily on data oracles to fetch real-world information. If the oracle source is compromised or experiences latency, the payout can be incorrect or delayed. Weak options often use single-source oracles without fallback mechanisms. A robust strategy requires oracles that aggregate data from multiple independent sources and include a time-weighted average mechanism to prevent manipulation. Without this, the smart contract becomes a single point of failure.

Illiquidity and Contract Rigidity

Unlike traditional insurance, parametric contracts are often standardized and less flexible. In the DeFi space, this can mean locked liquidity or complex unwinding procedures during a crisis. Some platforms promise instant payouts but impose hidden fees or minimum holding periods that negate the benefit during a rapid onset event. Evaluate the exit strategy and liquidity depth of the pool before buying. Rigid contracts can become liabilities if the market conditions change unexpectedly.

Key Takeaways

- Basis risk remains the primary structural flaw in many parametric products.

- Oracle redundancy is essential for DeFi-integrated policies.

- Liquidity and contract flexibility often get overlooked in favor of high yields.

Parametric insurance market research: what to check next

Integrating parametric insurance with DeFi requires navigating complex data and regulatory layers. Here are the practical answers to common questions about how these systems function and where they face friction.

No comments yet. Be the first to share your thoughts!