Get parametric insurance infrastructure right

Before deploying onchain risk transfer tools, you must align the technical architecture with the insurance logic. Parametric infrastructure is not a simple payment gateway; it is a closed-loop system where data triggers payouts. If the data feed is flawed, the contract fails, regardless of how robust the blockchain layer is. This section outlines the prerequisites for building reliable parametric insurance infrastructure.

Define the trigger and index clearly

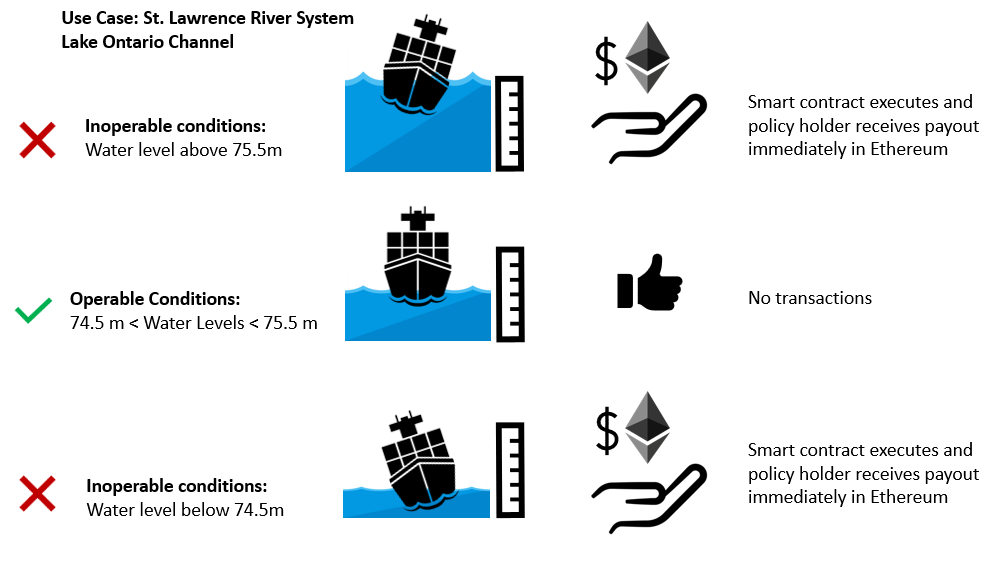

The foundation of any parametric policy is the index—the measurable variable that determines if a loss occurred. For infrastructure projects, this might be wind speed, rainfall volume, or seismic magnitude. You must choose an index that is objective, transparent, and difficult to manipulate. Avoid subjective metrics like "extent of damage" or "operational downtime," as these reintroduce basis risk and delay payouts. The trigger must be binary: did the threshold cross? If yes, payout. If no, no payout. This clarity is what makes parametric insurance fast.

Secure authoritative data feeds

Smart contracts cannot verify real-world events themselves. They rely on data oracles to fetch the index value. For high-stakes infrastructure, you cannot use amateur or aggregated data sources. You need primary, official sources such as government meteorological agencies, certified seismic centers, or recognized industry bodies. These sources must have a proven track record of accuracy and transparency. If the data provider has a history of revision or dispute, your infrastructure is vulnerable. The integrity of your onchain risk transfer tool depends entirely on the trustworthiness of this upstream data.

Structure the payout mechanism

Once the trigger is defined and the data secured, you must structure the payout. Unlike traditional insurance, parametric payouts are not based on actual financial loss but on the severity of the index breach. You need a clear formula that maps index values to payout amounts. This can be linear (e.g., $10,000 per mm of rainfall) or tiered (e.g., 50% payout at threshold, 100% at critical level). The formula must be encoded directly into the smart contract. This eliminates negotiation and ensures immediate liquidity when the event occurs, which is critical for infrastructure recovery.

Test the end-to-end flow

Before mainnet deployment, you must simulate the entire lifecycle. Create a test environment where you can inject fake data and verify that the contract responds correctly. Check edge cases: what if data is delayed? What if the source reports an anomaly? Your infrastructure should have fallback mechanisms, such as secondary data sources or a governance committee for dispute resolution. This testing phase is not optional; it is the only way to ensure that the tool works when the real disaster strikes.

Work through the steps

Parametric Insurance Infrastructure works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

Fix common mistakes in parametric insurance infrastructure

Building onchain risk transfer tools requires precision. A single misalignment between your smart contract logic and the real-world data source can leave a project exposed when it needs coverage most. Below are the most frequent errors and how to correct them.

Basing triggers on unverified oracles

The most critical failure point is trusting a data source that hasn't been rigorously vetted. If your parametric insurance payout depends on a weather index or seismic reading, that data must come from an authoritative, immutable source. Relying on a generic oracle without a clear audit trail introduces counterparty risk.

The Fix: Use only official meteorological agencies or government seismic monitors as your data source. Do not aggregate data from multiple competing sources unless your contract explicitly defines a medianization or consensus mechanism. Verify the oracle's history of uptime and accuracy before deployment.

Ignoring basis risk in trigger design

Basis risk occurs when the parametric trigger moves, but the actual loss does not. For example, a flood insurance policy might trigger because rainfall exceeded 100mm at a nearby weather station, even though the insured property remained dry. This disconnect destroys trust in the product.

The Fix: Calibrate triggers to the specific geographic footprint of the insured asset. Use high-resolution data layers that match the property's coordinates. Include a "dry run" period where you backtest the contract against historical events to ensure payouts align with actual losses in similar scenarios.

Overlooking settlement latency

Onchain insurance is valuable because of speed. If your smart contract waits for a manual confirmation step or a slow offchain verification process, you lose the primary advantage of parametric insurance. Delays in settlement can cripple liquidity for the insured party.

The Fix: Automate the entire settlement path. Once the oracle confirms the trigger event, the smart contract should execute the payout immediately without human intervention. Test the gas costs and execution time of your payout function to ensure it remains viable even during network congestion.

Parametric insurance infrastructure: what to check next

Before deploying onchain risk transfer tools, it helps to separate the technology from the contract mechanics. The infrastructure is simply the settlement layer; the insurance logic lives in the parameters. Below are the most common practical objections regarding implementation, accuracy, and liquidity.

Helpful gear

Use these product recommendations as a starting point, then choose the size, material, and price point that fit how you actually use the gear.

As an Amazon Associate, we may earn from qualifying purchases.

No comments yet. Be the first to share your thoughts!