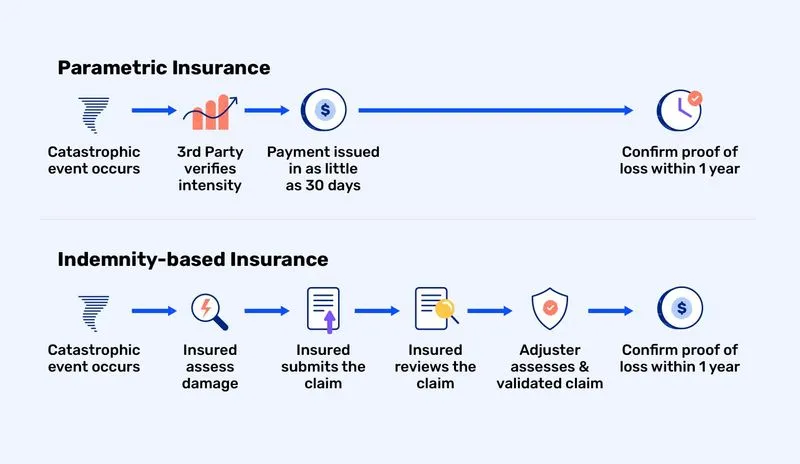

How parametric insurance differs from indemnity

Traditional indemnity insurance operates on a reactive principle: you prove you suffered a loss, and an insurer compensates you for the damage. This process relies heavily on claims adjusters, lengthy investigations, and subjective assessments of liability. For DeFi protocols, where smart contract failures or oracle manipulations can drain liquidity in minutes, this slow, human-centric model is incompatible with the need for immediate capital preservation.

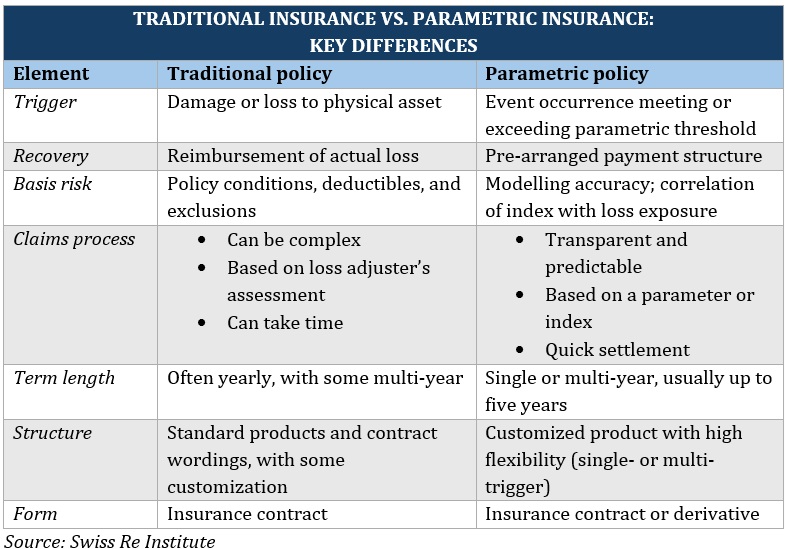

Parametric insurance removes the claims assessment entirely. Instead of evaluating actual financial damage, it pays out when a predefined, objective metric crosses a specific threshold. As Swiss Re notes, these index-based solutions cover the probability of a loss-causing event rather than the event's actual financial impact on a specific entity [src-serp-7]. If the data trigger is met, the payout happens automatically, regardless of whether the protocol actually lost funds or if the loss was caused by a different factor.

This distinction is critical for on-chain risk transfer. Consider a protocol insured against a "flash loan attack." In an indemnity model, an adjuster would need to verify if the attack caused permanent harm. In a parametric model, the contract monitors the blockchain for a specific transaction pattern or price deviation. Once that pattern is detected on-chain, the smart contract executes the payout instantly.

The result is a system built for speed and transparency. There is no ambiguity about what constitutes a "loss" because the definition is code, not opinion. This eliminates the friction of negotiations and allows capital to be restored to the protocol while the incident is still unfolding, rather than weeks after the damage is assessed.

Designing the oracle and trigger mechanism

Building a parametric insurance guide for DeFi requires a rigid technical backbone. Unlike traditional policies that wait for loss assessments, onchain parametric insurance relies entirely on data accuracy and deterministic logic. The system functions like a vending machine: if the input matches the criteria, the payout executes automatically. This eliminates subjectivity but places immense pressure on the oracle infrastructure and the precision of the trigger conditions.

Selecting reliable data sources

The oracle acts as the bridge between offchain reality and onchain execution. In DeFi, this is often the most vulnerable point. If the data source is compromised or delayed, the smart contract pays out incorrectly or fails to pay at all. For high-stakes financial decisions, you cannot rely on a single data feed. The architecture must aggregate data from multiple independent providers to ensure redundancy and accuracy.

Official sources provide the gold standard for this data. For example, the National Association of Insurance Commissioners (NAIC) and Swiss Re Institute define parametric insurance as paying out based on predefined event parameters rather than actual losses. In a DeFi context, this means the oracle must pull verified data—such as weather indices, earthquake magnitudes, or price feeds—from authoritative sources like Descartes Labs or major exchanges. The goal is to minimize latency while maximizing trust.

Defining the trigger conditions

Once the data source is established, the next step is defining the exact mathematical conditions that execute the smart contract. This is the "parametric" part of the equation. The trigger must be binary: either the condition is met, or it is not. There is no room for interpretation.

For instance, a crop insurance contract might trigger if rainfall drops below 2 inches for three consecutive days. A DeFi protocol might trigger a payout if the price of ETH falls below $1,500 for more than one hour. These conditions are coded directly into the smart contract. The oracle feeds the data, and the contract compares it against the threshold. If the threshold is breached, the funds are released instantly.

Visualizing the execution

Understanding the trigger mechanism is easier when visualized. Imagine a price chart where a horizontal line represents the trigger threshold. As long as the price stays above the line, no action occurs. The moment the price crosses below that line, the smart contract executes. This simplicity is what makes parametric insurance scalable across DeFi.

Structuring smart contracts for automated payouts

Building a parametric insurance guide for DeFi requires shifting focus from legal indemnity to code execution. Unlike traditional policies that rely on adjusters and paperwork, this infrastructure uses smart contracts to manage the escrow and trigger verification automatically. The goal is to remove human discretion entirely, ensuring that payouts happen only when specific, verifiable data points are met.

The Escrow and Trigger Mechanism

The core of the system is a smart contract that holds the premiums in a stablecoin escrow. This contract acts as a neutral third party, holding funds until the trigger event is confirmed. The trigger itself is an oracle-fed data point—such as a specific ETH price level or a weather station reading—that must be immutable and publicly verifiable.

When the oracle reports that the condition has been breached, the contract’s logic executes immediately. There is no claims process, no waiting for approval, and no ambiguity. The code checks the data against the predefined threshold. If the data matches the criteria, the contract initiates the transfer of funds.

Automatic Transfer of Funds

Once the trigger is verified, the smart contract automatically transfers the agreed-upon stablecoin amount to the policyholder’s wallet. This happens in a single transaction block, often within seconds of the data confirmation. This speed is the primary value proposition for DeFi users facing immediate liquidity risks.

To illustrate the efficiency gain, compare this to traditional insurance workflows:

| Process | Traditional Claims | Parametric Smart Contract |

|---|---|---|

| Verification | Manual review (days to weeks) | Oracle data check (seconds) |

| Payout | Bank transfer (days) | On-chain transfer (instant) |

| Dispute | Common | Near zero (code is law) |

This automation reduces counterparty risk significantly. The policyholder does not need to trust the insurer’s willingness to pay; they only need to trust the code and the data source. As Swiss Re notes, this model fills protection gaps left by indemnity insurance by expanding coverage to measurable events rather than physical asset damage. The result is a risk transfer mechanism that is fast, transparent, and programmable.

Pricing models and basis risk management

Pricing parametric insurance in DeFi is less about calculating the exact cost of a potential loss and more about pricing the probability of a trigger event. Unlike traditional indemnity insurance, where premiums reflect individual risk profiles and historical claims, parametric models rely on statistical probabilities of predefined events. This shift allows for faster underwriting but introduces unique challenges when dealing with volatile crypto assets and opaque oracle data.

The core financial risk in any parametric contract is basis risk. This occurs when the index used to trigger a payout does not perfectly correlate with the actual financial loss suffered by the policyholder. For example, a DeFi protocol might insure against a specific stablecoin depegging below $0.95. If the depeg happens but the user’s funds were secured in a cold wallet and suffered no actual loss, the payout still triggers. Conversely, if the user loses funds due to a smart contract exploit that doesn’t match the defined index criteria, they receive nothing. This mismatch is the fundamental tension in parametric design.

To mitigate basis risk, protocols must carefully select oracles and indices. Swiss Re notes that parametric solutions cover the probability of a loss-causing event, emphasizing that the index must be a robust proxy for actual damage. In DeFi, this often means using multiple data sources or choosing indices that closely mirror the specific revenue streams or collateral values at risk. The tighter the correlation between the trigger and the real-world impact, the lower the basis risk and the more trustworthy the insurance product becomes.

Pricing premiums in this environment requires dynamic models that account for both the frequency of trigger events and the severity of potential payouts. Since DeFi markets can move violently in short periods, static pricing models often fail. Protocols may use real-time volatility metrics to adjust premiums, ensuring that coverage remains affordable during calm periods while providing adequate capital reserves during market stress. This dynamic approach helps maintain the solvency of the insurance pool while keeping the cost of protection aligned with current market conditions.

Implementing a DeFi risk transfer strategy

Building a parametric insurance strategy on-chain requires moving beyond theory into rigorous engineering. Unlike traditional indemnity claims, smart contracts execute payouts automatically when external data confirms a loss. This eliminates human adjudication but introduces new dependencies: the reliability of oracles and the security of the underlying code.

To integrate this coverage effectively, follow this operational workflow.

Start by identifying the exact event that triggers a payout. For DeFi, this is often a price crash or a protocol exploit. You must select a reputable oracle, such as Chainlink, to provide this data. The trigger must be binary and indisputable to prevent disputes. As noted in foundational guides by Descartes Underwriting, clarity in trigger definition is the bedrock of parametric models.

Since the contract executes automatically, any bug in the logic can lead to catastrophic losses or failed payouts. Engage a reputable audit firm to review the oracle integration and payout logic. This step is non-negotiable for high-stakes financial applications. The audit should specifically test edge cases where oracle data might be delayed or manipulated.

Before launching, deposit the required liquidity into the insurance escrow contract. This capital backs the policies issued. Conduct extensive testing on a testnet to simulate trigger events and verify that payouts occur as expected. This ensures that the protocol can handle the load and that the oracle data is correctly interpreted by the contract.

Implementing this strategy reduces counterparty risk but shifts the burden to technical precision. By focusing on clear triggers, rigorous audits, and thorough testing, protocols can offer reliable protection to their users.

Common questions about onchain coverage

Parametric insurance in DeFi operates differently than traditional policies. Instead of assessing individual losses after an event, these smart contracts trigger payouts automatically when a specific data point—like a price drop or weather metric—crosses a predefined threshold. This distinction is central to understanding how the technology functions and where it fits in a risk management strategy.

How do oracles prevent manipulation?

Oracles serve as the bridge between off-chain reality and on-chain execution. To prevent manipulation, reputable protocols use decentralized oracle networks that aggregate data from multiple independent sources. This diversity makes it significantly harder for a single actor to skew the data feed. If an oracle fails or becomes unresponsive, most contracts include a fallback mechanism or a governance pause to halt payouts until the issue is resolved.

What is basis risk in parametric insurance?

Basis risk is the gap between the index used to trigger a payout and the actual financial loss incurred by the policyholder. For example, if a parametric policy is triggered by a drop in the ETH/USD price, but your loss stems from a smart contract exploit rather than market volatility, you may receive a payout that doesn't fully cover your damages. As noted by the NAIC, these products pay based on event parameters rather than actual losses, meaning the coverage is precise but not necessarily comprehensive for all risk types.

Is parametric insurance regulated?

Regulatory status varies by jurisdiction. While traditional parametric disaster insurance is gaining traction with bodies like the NAIC, DeFi implementations often operate in a gray area. Most current protocols function as decentralized autonomous organizations (DAOs) rather than licensed insurance companies. Users should verify the legal standing of any protocol in their region, as regulatory frameworks for on-chain financial instruments are still evolving.

No comments yet. Be the first to share your thoughts!