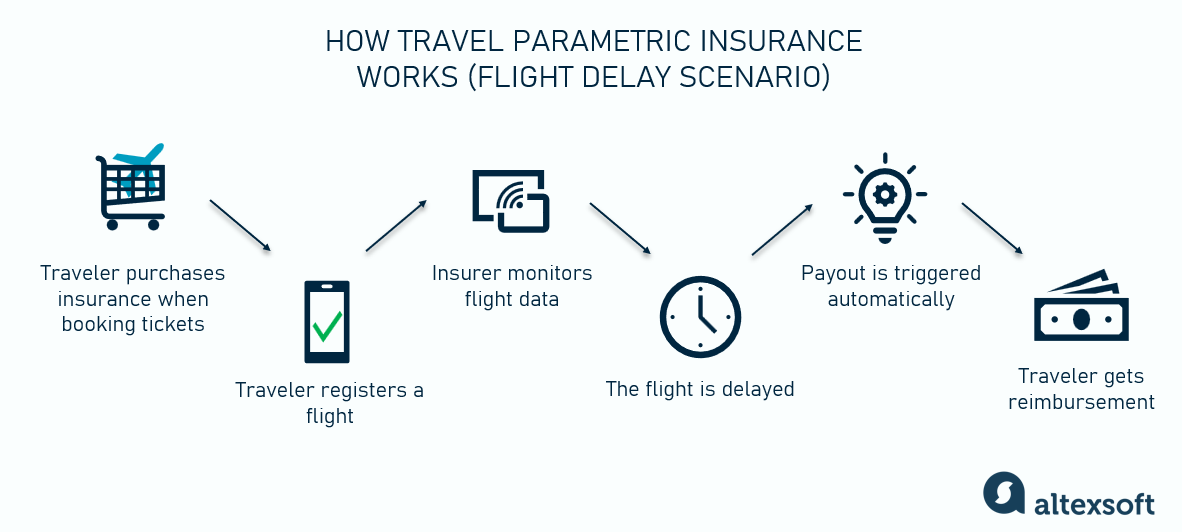

Why parametric insurance fits DeFi risk transfer

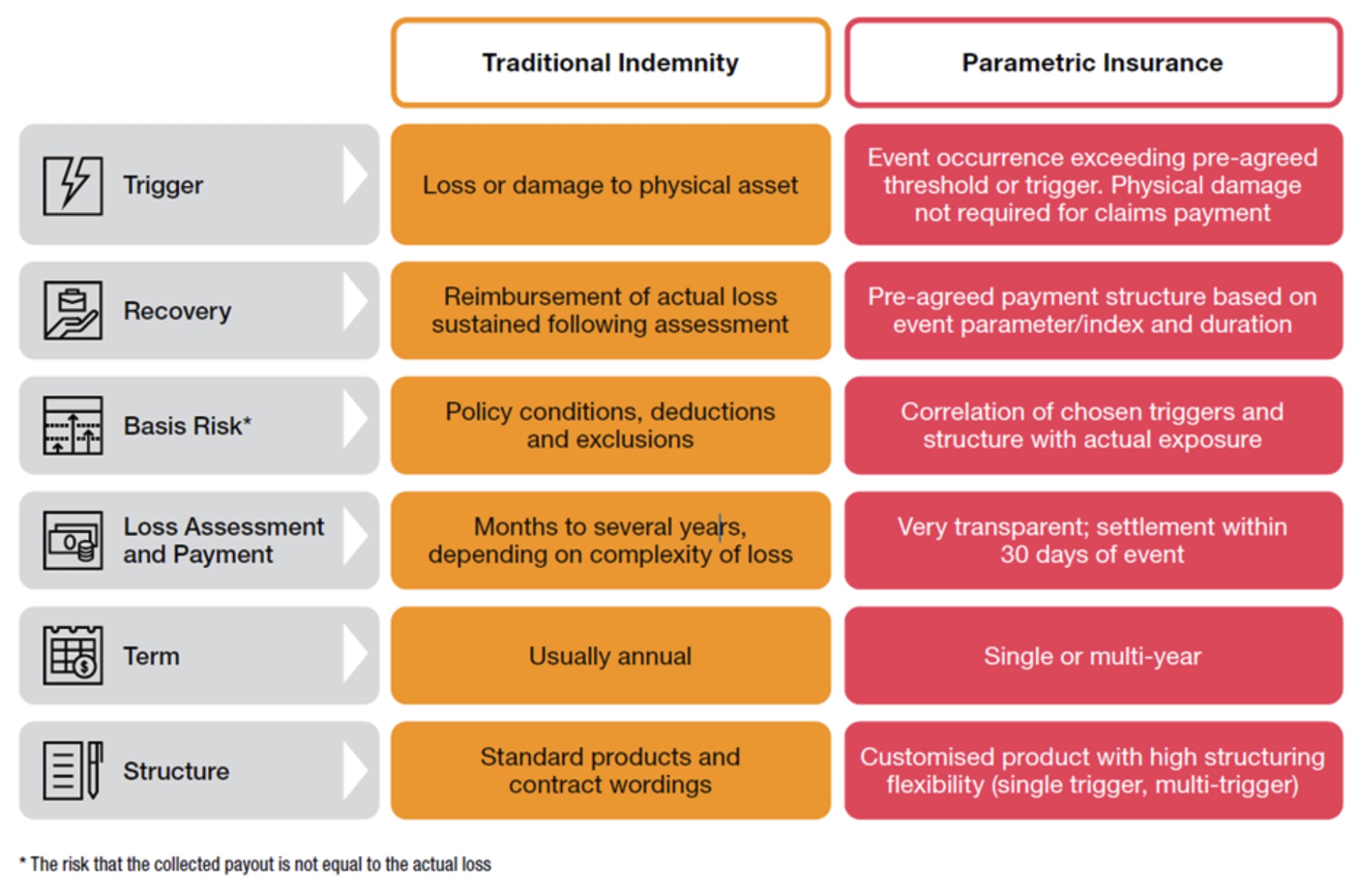

Traditional indemnity insurance relies on a slow, opaque claims process that is fundamentally mismatched with the speed of digital asset markets. When a smart contract fails or a bridge is drained, the window to mitigate damage often closes within minutes. By contrast, a parametric insurance strategy removes subjective loss assessment. Payouts are triggered automatically when an objective, pre-defined data point crosses a specific threshold.

This mechanism shifts the focus from how much was lost to whether a specific event occurred. According to Swiss Re, parametric insurance expands coverage beyond physical assets to fill protection gaps left by traditional models, such as deductibles and excluded perils. In DeFi, the "peril" is often a verifiable on-chain event, such as a price drop below a certain level or a confirmed exploit. This certainty allows protocol treasuries to react immediately, rather than waiting months for a settlement.

The transparency of this model is critical for decentralized finance. Because trigger conditions are encoded into smart contracts, the logic is public and auditable before purchase. There is no hidden underwriting discretion. This alignment of code and capital ensures that risk transfer is as fluid as the assets being protected.

While traditional insurers struggle with crypto volatility, parametric models offer a standardized approach. By defining clear triggers—such as oracle price feeds or on-chain transaction hashes—protocols can secure coverage that pays out instantly. This transforms insurance from a reactive administrative burden into a proactive risk management tool.

Designing the trigger mechanism

The foundation of any parametric insurance strategy is the trigger—the specific condition that initiates a payout. Unlike traditional insurance, which relies on claims adjusters, a parametric trigger is binary and objective. It is either met or it is not. This distinction eliminates ambiguity and speeds up settlement, but it means the trigger design must be flawless. As Aon notes, parametric insurance is a "simple, straightforward and fast-paying risk transfer solution that is triggered by a specific, pre-defined event" Aon. In DeFi, that "pre-defined event" must be coded with mathematical precision.

1. Selecting reliable data oracles

Your trigger depends entirely on data. If the data feed is manipulated or delayed, the payout is either wrong or never happens. In DeFi, this data comes from oracles—decentralized networks that fetch off-chain information and bring it on-chain. You cannot rely on a single source. A robust strategy uses a multi-source oracle network (like Chainlink) that aggregates data from multiple providers to prevent single-point failures. The oracle must be configured to provide the exact metric you need, whether that is the spot price of ETH, a volatility index, or the status of a specific protocol. Trust is transferred from the counterparty to the oracle infrastructure.

2. Defining precise payout parameters

Once the data source is set, you must define the exact threshold for the trigger. For a DeFi protocol, common triggers include:

- Price Drops: A specific asset (e.g., ETH) falling below a certain USD value for a sustained period (e.g., 10-minute average below $1,800).

- Volatility Spikes: A rapid increase in price variance over a short window, indicating market stress.

- Smart Contract Exploits: Confirmation of a specific function call or fund drain event on a monitored protocol.

The NAIC highlights that parametric insurance pays "set amounts based on event parameters rather than losses" NAIC. In DeFi, this means the payout is fixed or formulaic, not based on the actual financial harm suffered by a user. This requires careful calibration: too loose a trigger, and the insurance becomes too expensive; too tight, and it never pays out when users need it most.

3. Implementing time-weighted averages

Raw price data is noisy. A single flash crash can trigger a false positive if you use the immediate spot price. To mitigate this, most sophisticated parametric strategies use a Time-Weighted Average Price (TWAP) or a similar rolling average. Instead of triggering on the price at second T, the trigger looks at the average price over the last N minutes. This smooths out volatility and ensures the trigger reflects a genuine market shift rather than a temporary glitch. It adds a small delay to the payout, but it significantly reduces the risk of frivolous claims or accidental payouts due to market manipulation.

4. Testing and stress-testing the trigger

Before deploying capital, you must simulate the trigger under various market conditions. This includes backtesting against historical data to see how the trigger would have performed during past crashes, as well as forward-testing in a sandbox environment. You should also consider "tail risks"—events that are rare but severe. Does the trigger hold up if the oracle network experiences a temporary outage? What happens if the price feed is delayed? Rigorous testing ensures that the mechanism works not just in normal conditions, but when it matters most.

Choose a decentralized oracle network that aggregates data from multiple providers to ensure reliability and prevent single-point failures.

Set precise, objective parameters for the trigger, such as a specific price drop or volatility spike, ensuring they are binary and unambiguous.

Implement a rolling average (TWAP) for price data to smooth out noise and prevent false triggers from short-term market spikes.

Simulate the trigger under historical crash scenarios and potential oracle failures to ensure robustness before deployment.

The chart above shows ETH price action. In a real parametric strategy, you would overlay horizontal lines to mark your specific trigger thresholds (e.g., the TWAP average price). This visualizes exactly where the "if" condition in your smart contract would activate. The goal is to make the trigger visible and understandable to all stakeholders, ensuring transparency in how the insurance mechanism works.

By focusing on these technical core components—oracle selection, precise parameters, time-weighting, and rigorous testing—you build a parametric insurance strategy that is not just a theoretical concept, but a functional, reliable risk transfer tool for the DeFi ecosystem.

Choosing the right onchain coverage provider

Selecting a parametric insurance protocol requires matching your specific DeFi risk profile to the provider's mechanics. Unlike traditional insurance, which relies on claims adjusters, parametric insurance offers rapid, transparent, and predetermined payouts based on predefined triggers. This mechanism significantly reduces administrative friction and payout delays, which is critical when capital is at risk.

When evaluating providers, focus on three core metrics: liquidity depth, capital efficiency, and trigger accuracy. Liquidity ensures that payouts can be executed immediately upon trigger validation without slippage. Capital efficiency determines how much coverage you can secure relative to the premium cost. Trigger accuracy measures how closely the protocol's oracle data aligns with your actual exposure, minimizing basis risk.

The table below compares leading DeFi parametric insurance protocols. Use this data to identify which provider best supports your strategy, whether you are hedging against smart contract failure, oracle manipulation, or market volatility.

| Protocol | Max Coverage Limit | Premium Structure | Trigger Type |

|---|---|---|---|

| Nexus Mutual | $10M+ | Fixed & Dynamic | Community Vote |

| InsurAce | Varies by Vault | Fixed | Oracle + Smart Contract |

| Hedgy | $100k+ | Fixed | Oracle + Smart Contract |

| Unslashed | Custom | Fixed | Oracle + Smart Contract |

Avoid these trigger design mistakes

Designing a parametric insurance strategy for DeFi risk transfer requires precision. The core appeal of parametric products is their ability to pay out automatically when a predefined event occurs, removing the need for lengthy claims assessments. However, this efficiency is only as good as the parameters you set. If those parameters are flawed, the insurance becomes either useless or dangerously expensive.

The most common pitfall is overfitting triggers to past events. It is tempting to look at historical data and set thresholds that perfectly match previous losses. This approach fails because market conditions and volatility regimes shift. A trigger that worked during a calm period might trigger false payouts during high volatility, or fail to pay out during a genuine crisis if the event exceeds the modeled range. You need triggers that are robust across different market environments, not just those that fit the last bull or bear market.

Another critical error is relying on low-liquidity oracles. Your payout depends entirely on the data source. If the oracle you choose is backed by thin liquidity or can be manipulated, your insurance is effectively worthless. A manipulated price feed can trigger a false payout, draining your pool, or fail to trigger during a real crash, leaving you exposed. Always choose oracles with deep liquidity and a proven track record of resistance to manipulation.

Finally, watch out for coverage gaps. Parametric policies usually cover one specific peril, such as a drop in ETH price below a certain threshold. They do not cover broad market risks like smart contract failures or governance attacks. If your strategy relies on this insurance to protect your entire portfolio, you will find yourself underinsured when the unexpected happens. Use parametric insurance as a specific hedge, not a blanket solution.

The Hidden Costs: Basis Risk and Coverage Gaps

While a parametric insurance strategy offers speed and transparency, it is not a silver bullet. The primary drawback is basis risk—the disconnect between the index trigger and your actual financial loss. Because these policies pay out based on predefined data points (like a specific DeFi protocol hack or a drop in ETH price) rather than actual damages, you can suffer a significant loss without triggering a payout, or receive a payout when your actual loss is minimal.

This mechanism creates narrow coverage scopes. Most parametric policies are designed for specific, binary events, such as a smart contract exploit or a sudden market crash. They rarely cover broader systemic risks, operational errors, or gradual value erosion. As noted by industry analysts, relying solely on parametric products often leaves policyholders exposed to other vulnerabilities, necessitating additional conventional insurance layers to cover the full spectrum of exposure.

To mitigate these gaps, a robust strategy treats parametric insurance as a complement to, not a replacement for, traditional risk management. It works best for high-impact, low-frequency events where traditional claims processes are too slow to prevent insolvency. For ongoing operational risks, standard liability coverage or internal risk reserves remain essential.

Final checks before deploying coverage

Before you lock capital or purchase a parametric insurance strategy, run through this verification list. Traditional indemnity insurance relies on loss assessment, which can take months, but parametric solutions promise speed by paying out based on pre-defined triggers. This speed is only as reliable as the data feeding it.

Check the data source feeding your smart contract. If the oracle fails or is manipulated, the payout logic breaks. Ensure the oracle has a proven track record of delivering accurate, tamper-proof data for the specific metric you are insuring against.

Ambiguity in trigger definitions is the primary cause of claim disputes. Define your parameters with absolute precision. For example, instead of "heavy rain," use "rainfall exceeding 50mm within 24 hours at Station X." The National Association of Insurance Commissioners notes that these clear parameters are what enable faster payouts after disasters [4].

Even if the trigger is met, you need a counterparty to pay. For traditional parametric layers, check the reinsurer’s credit rating. For DeFi protocols, audit the liquidity pool’s depth and the smart contract’s security history. Aon emphasizes that parametric insurance is a risk transfer solution, meaning the counterparty’s ability to pay is paramount [3].

Calculate the total cost of coverage, including protocol fees and potential basis risk. Parametric policies often have lower administrative costs than traditional ones, but you must ensure the premium doesn’t eat into the value of the payout [5].

Once these checks are complete, you can deploy with confidence. This structured approach ensures your parametric insurance strategy is not just a theoretical hedge, but a functional safety net for your DeFi positions.

No comments yet. Be the first to share your thoughts!