How parametric insurance works onchain

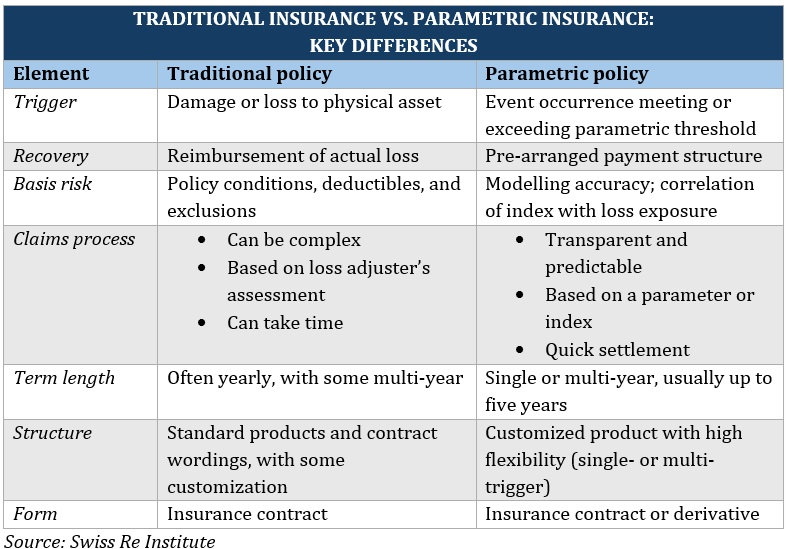

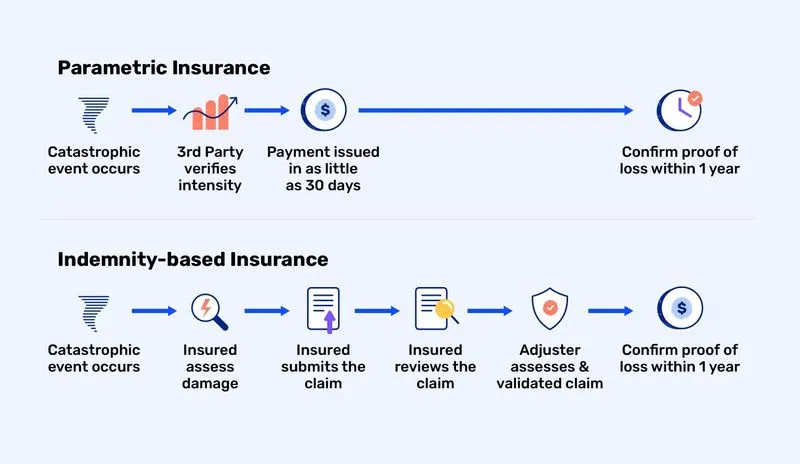

Traditional insurance relies on indemnity: you file a claim, an adjuster investigates, and if verified, you get paid. This process is slow and prone to disputes. Parametric insurance flips this model by paying out automatically when a predefined external index hits a specific threshold.

Onchain, smart contracts handle this mechanism. The "parametric" part refers to pre-agreed variables—like price, volatility, or oracle data—that act as the trigger. When the data source confirms the condition is met, the contract executes the payout instantly. There is no claims adjuster, no paperwork, and no waiting period. The code is the arbiter.

This shift is critical for DeFi risk management. Protocols can hedge against smart contract failures, oracle manipulation, or extreme market volatility by linking coverage to onchain metrics. For example, a liquidity pool might buy parametric coverage that triggers if a specific asset’s price drops below a certain level relative to a trusted oracle feed within a 10-minute window.

The reliability of this system depends entirely on the accuracy of the data source. If the oracle is manipulated or the data feed is delayed, the trigger may fail or activate incorrectly. Therefore, choosing a robust, decentralized oracle network is as critical as selecting the coverage terms. Swiss Re and other traditional reinsurers have long championed this model for its speed and transparency, and onchain insurance brings those same benefits to digital assets.

The chart above illustrates how volatility indices behave. In a parametric setup, a sudden spike in this index could serve as the trigger for a volatility hedge, demonstrating how external data points directly translate into financial outcomes without human intervention.

Key DeFi risk transfer strategies

Onchain parametric insurance moves beyond covering physical assets to address the specific liquidity and operational risks inherent in decentralized finance. As noted by Swiss Re, these products are designed to fill protection gaps left by traditional indemnity insurance, such as deductibles, excluded perils, or the scarcity of coverage during systemic shocks [1]. In DeFi, this translates to automated payouts triggered by onchain data, allowing protocols to maintain solvency without waiting for lengthy claims adjudication.

Hedging protocol treasury volatility

Treasury management is often the most critical function for a DAO or protocol. Parametric strategies can hedge against sharp drops in the value of native tokens or stablecoin depegs. By linking payouts to oracle prices, a protocol can automatically receive funds when its treasury assets fall below a certain threshold, allowing it to rebalance or buy back tokens to stabilize the ecosystem.

Covering smart contract exploit gaps

Traditional cyber insurance often excludes coverage for exploits due to the difficulty of verifying causality and intent. Parametric insurance bypasses this by triggering payouts based on verified onchain events, such as a specific amount of ETH drained from a contract within a set timeframe. This speed is vital for maintaining user confidence and ensuring the protocol can continue operating immediately after an incident.

Comparing traditional vs. parametric coverage

The following table highlights the structural differences between traditional indemnity insurance and parametric coverage in a DeFi context.

| Feature | Traditional Indemnity | Parametric Coverage |

|---|---|---|

| Trigger | Proof of actual loss | Predefined data threshold |

| Payout speed | Weeks to months | Minutes to hours |

| Basis risk | Low | Higher |

| Verification | Manual claims process | Automated oracle data |

While parametric insurance offers speed and certainty, it introduces basis risk—the potential for a mismatch between the trigger event and the actual financial loss. For example, a payout might trigger due to a price drop, but if the protocol’s treasury is diversified, the actual impact might be less severe. Conversely, a protocol might suffer a significant exploit that doesn’t meet the parametric trigger threshold, leaving it underinsured. Therefore, these strategies work best as part of a broader risk management framework, complementing, rather than replacing, traditional security audits and multi-sig controls.

[1] Swiss Re, "Comprehensive Guide to Parametric Insurance," 2024.

Building the parametric infrastructure

Onchain parametric insurance relies on a three-part stack: oracles for data verification, smart contracts for execution, and liquidity pools for payout funding. This architecture replaces the traditional claims adjuster with code and verified data, creating a system that is transparent and automated.

Oracles: The Data Verification Layer

Oracles serve as the bridge between real-world events and the blockchain. In traditional insurance, an adjuster visits a site to assess damage. In parametric insurance, an oracle feeds specific data points—such as wind speed, earthquake magnitude, or flight delay duration—into the smart contract.

Reliability is critical here. If the oracle feeds incorrect data, the contract executes incorrectly, leading to false payouts or denied claims. The Swiss Re Institute has noted that data integrity is the primary technical hurdle in scaling parametric models. For onchain systems, this means using decentralized oracle networks that aggregate data from multiple sources to prevent manipulation. A single point of failure in the data feed can undermine the entire trust model of the policy.

Smart Contracts: The Execution Engine

Once the oracle provides the data, the smart contract evaluates it against the pre-set trigger conditions. If the data meets or exceeds the threshold, the contract automatically executes the payout. There is no human intervention, no paperwork, and no delay for approval.

This automation reduces operational costs significantly. Traditional insurance involves heavy administrative overhead for claims processing. Onchain parametric contracts execute instantly, transferring stablecoins or native tokens to the policyholder’s wallet. The logic is immutable and transparent, visible to anyone on the blockchain, which builds trust in the payout mechanism.

Liquidity Pools: Funding the Payouts

The final component is the source of funds. In traditional insurance, premiums are held in reserves managed by the insurer. In DeFi parametric insurance, liquidity pools often back the coverage. These pools are funded by liquidity providers who earn yield in exchange for bearing the risk of parametric triggers.

When a trigger is met, the smart contract draws the required payout from the pool. This model ensures that funds are always available for immediate distribution, provided the pool has sufficient depth. It also allows for more flexible pricing models, as the cost of coverage can adjust dynamically based on the pool’s risk exposure and available liquidity.

Understanding basis risk and coverage gaps

Parametric insurance promises speed, but it introduces a specific vulnerability: basis risk. This occurs when the trigger event recorded by the index does not perfectly align with the actual financial loss experienced by the policyholder. In traditional indemnity insurance, payouts are based on verified damage. In parametric models, they are based on data points. If the data is accurate but the correlation is weak, you may face a coverage gap where the index shows a severe event, yet your specific asset remains unscathed—or worse, you suffer significant loss while the index reports nothing.

The Insurance Association of America and Swiss Re both highlight that this disconnect is the primary barrier to wider adoption in natural catastrophe (NatCat) markets. For example, a hurricane might pass 50 miles offshore, triggering a wind-speed parametric payout, while a coastal property suffers negligible damage. Conversely, a localized flood might devastate a farm without reaching the threshold of a regional rainfall index. In DeFi, this manifests when a protocol’s collateral is liquidated due to a broad index drop, even if the specific token held remains solvent.

Mitigating basis risk requires rigorous stress testing of the oracle and index selection. It is not enough to choose a popular data source; you must validate that the data granularity matches your exposure. Narrower indices reduce basis risk but increase the likelihood of false negatives (no payout when needed). Wider indices increase the likelihood of false positives (payouts when no loss occurred). The goal is to find the "sweet spot" where the correlation is strong enough to provide reliable protection without creating excessive moral hazard or basis mismatch.

Implementing your coverage checklist

Before deploying capital into on-chain risk transfer, protocols must treat parametric insurance as a structural hedge, not an afterthought. The goal is to map specific smart contract risks to external data sources that can trigger payouts without manual claims adjustment. This process requires aligning your protocol’s technical architecture with the capabilities of oracle networks and underwriting providers.

1. Identify the specific risk vector

Start by isolating the single most critical failure point in your protocol. Is it a liquidity pool exploit, a price oracle manipulation, or a governance attack? Parametric coverage works best when the risk is binary and measurable. Vague "security breach" clauses rarely translate well to on-chain triggers. Define the exact event that constitutes a loss. For example, if your protocol relies on a specific oracle, define the threshold deviation that would destabilize your collateral ratio.

2. Select a reliable data oracle

Your payout depends entirely on the integrity of the data source. If the oracle is compromised, the insurance is useless. Partner with established oracle networks like Chainlink or Pyth Network that have proven track records in delivering tamper-resistant price feeds. Ensure the oracle has sufficient decentralization and fallback mechanisms. This step is non-negotiable; relying on a single, unverified data point is a recipe for total coverage failure.

3. Define the trigger mechanism

The trigger is the bridge between the real-world event and the smart contract payout. It must be automated, transparent, and resistant to manipulation. Common triggers include price drops below a certain percentage, transaction volume spikes, or specific block numbers. Avoid complex conditions that require human interpretation. The trigger should be a simple if/then statement that the smart contract can execute automatically. This ensures speed and reduces the risk of dispute.

4. Vet the underwriting provider

Not all parametric providers are created equal. Look for entities with experience in both traditional reinsurance and decentralized finance. Providers like Swiss Re have been exploring parametric models for years, bringing institutional rigor to the space. Evaluate their capitalization, claims history, and technical infrastructure. Ensure they have a clear process for verifying trigger events and distributing payouts. Avoid providers who cannot provide transparent proof of reserves or clear smart contract audit reports.

5. Test the smart contract integration

Before going live, run extensive simulations of your coverage contract. Deploy a testnet version and simulate various trigger scenarios, including edge cases and oracle failures. Verify that the payout logic executes correctly and that funds are distributed to the right addresses. This step is critical for ensuring that your coverage works when you need it most. A buggy insurance contract is worse than no insurance at all.

Common Questions About Onchain Parametric Insurance

Onchain parametric insurance is still a niche sector, so it’s natural to have questions about how payouts work and who backs them. Unlike traditional insurance, which waits for loss assessment, onchain policies pay out automatically when a verified oracle confirms an event threshold has been hit.

How fast are payouts on parametric DeFi insurance?

Speed is the primary advantage of parametric coverage. Because there is no need to adjust for individual damage assessments, payouts can occur within minutes or hours of the triggering event. The National Association of Insurance Commissioners (NAIC) notes that parametric insurance offers faster payouts after disasters by paying set amounts based on event parameters rather than losses. Onchain, this process is automated via smart contracts, removing the administrative lag common in traditional claims processing.

Can oracles be manipulated to trigger false payouts?

Oracle manipulation is a significant risk in DeFi, but top-tier parametric protocols mitigate this by using decentralized data feeds and multi-source verification. Relying on a single data point is dangerous; instead, reputable projects aggregate data from multiple independent oracles to confirm that a trigger event, such as a specific earthquake magnitude or weather index, has genuinely occurred. This redundancy makes it computationally expensive and practically difficult for bad actors to manipulate the trigger conditions.

Is parametric DeFi insurance regulated?

Regulatory clarity varies by jurisdiction, but the industry is moving toward formal oversight. Organizations like the Insurance Association of Switzerland (IAIS) and the NAIC are actively studying parametric products to integrate them into existing frameworks. While most onchain protocols operate in a decentralized, borderless manner, they often structure their legal wrappers to comply with local insurance laws where possible. Users should always verify if a protocol has obtained any specific regulatory licenses or partnerships in their region.

What is basis risk in onchain insurance?

Basis risk occurs when the trigger event does not perfectly align with your actual financial loss. For example, an earthquake parametric policy might pay out because the epicenter was near a city, even if your specific property was undamaged. This is a known limitation of index-based products. To minimize basis risk, users can choose protocols that offer granular geographic triggers or combine parametric coverage with traditional indemnity policies for comprehensive protection.

Do I need to audit the smart contracts myself?

While you don’t need to be a developer, understanding that smart contract audits are non-negotiable is critical. Reputable onchain insurance providers publish third-party audit reports from firms like CertiK or OpenZeppelin. These audits verify that the logic governing payouts and fund custody is secure. Never deploy capital into a protocol that lacks recent, public audits, as vulnerabilities in the code could lead to total loss of the insurance pool.

No comments yet. Be the first to share your thoughts!