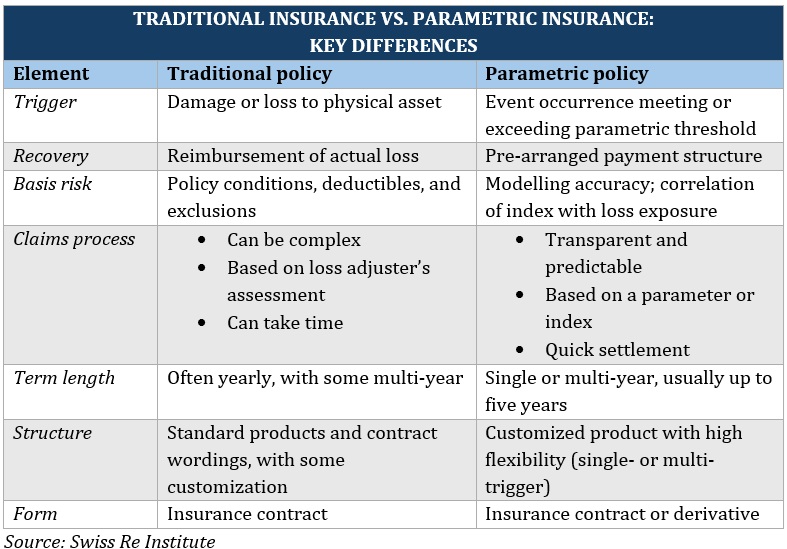

What parametric insurance actually pays

Parametric insurance works differently than the coverage you likely already hold. Traditional indemnity insurance pays out based on the actual financial loss you suffer after a claim is assessed. Parametric insurance, by contrast, pays out when a specific, objective trigger event occurs, regardless of the actual damage incurred. It shifts the focus from assessing loss to verifying data.

Think of it like a flight delay insurance policy. If your flight is delayed by more than two hours, you get a fixed payout. The insurer doesn’t care if you missed a connection or lost luggage; the trigger was met, so the money moves. In parametric insurance, the "trigger" is a measurable data point, such as wind speed, earthquake magnitude, or temperature thresholds.

This model fills critical protection gaps left by traditional indemnity insurance. As noted in Swiss Re’s comprehensive guide, parametric products are particularly useful for covering deductibles, excluded perils, or situations where loss assessment is slow or scarce. For DeFi protocols, this means risk transfer can happen instantly based on on-chain data or oracle feeds, without the need for lengthy claims processing.

The primary advantage is speed and certainty. Once the on-chain data confirms the trigger event, the smart contract executes the payment automatically. This removes the administrative friction and potential disputes inherent in traditional insurance claims. However, it requires careful design to ensure the trigger accurately reflects the risk you are trying to hedge, minimizing the basis risk mentioned above.

Why DeFi needs faster capital access

DeFi protocols operate on thin margins where seconds matter. When a liquidity crunch hits or a macro shock ripples through the market, traditional insurance models are too slow to save a protocol. The underwriting process—assessing damage, verifying losses, and approving claims—can take weeks or months. In crypto, that delay is often fatal. By the time a traditional insurer pays out, the protocol may have already collapsed, or the capital may have drained irretrievably.

Parametric insurance solves this latency problem by removing the claims assessment entirely. Payouts are triggered automatically when on-chain data confirms a specific event, such as a price drop below a threshold or a successful exploit on a known contract. This mechanism ensures immediate liquidity injection exactly when it is needed most, allowing protocols to maintain solvency during critical windows.

The Swiss Re Institute highlights that parametric structures offer faster payouts after disasters by paying set amounts based on event parameters rather than actual losses. This distinction is vital for DeFi. While traditional insurance requires proof of how much was lost, parametric insurance only needs proof that the event occurred. This shift from loss-based to event-based triggers aligns perfectly with the transparent, data-rich nature of blockchain networks.

However, this speed comes with a trade-off known as basis risk. As noted in a Wharton Risk Center primer, the payout may not fully cover actual losses because it is tied to a predefined trigger, not the economic damage sustained. If the trigger is hit but the protocol’s specific losses are higher, the gap must be covered by the protocol’s own reserves. For this reason, parametric insurance is best used as a rapid-response liquidity buffer rather than a complete replacement for comprehensive coverage.

Oracles as the trigger mechanism

The reliability of parametric insurance hinges entirely on the quality of the oracle data feeding the smart contract. Oracles serve as the bridge between off-chain real-world events and on-chain execution. If the oracle data is manipulated, delayed, or inaccurate, the parametric trigger may fire incorrectly, leading to unjustified payouts or missed coverage.

For DeFi protocols, selecting the right oracle is a critical risk management decision. Protocols often use decentralized oracle networks to aggregate data from multiple sources, reducing the risk of single-point failure. The trigger mechanism must be robust enough to withstand market volatility and potential attack vectors while remaining simple enough to execute automatically.

Basis risk and payout gaps

Parametric insurance is fast, but it is not perfect. The primary drawback is basis risk, a gap between the trigger event and your actual financial loss. In traditional indemnity insurance, payouts are based on verified damages. In parametric insurance, payouts are based on data. If the data triggers a payout, you get paid, regardless of whether you suffered a loss.

This disconnect can work in your favor or against you. You might receive a payout despite having no damage, or suffer significant damage without receiving a cent because the trigger threshold was not met. As noted by the Wharton School, the payout is not related to actual losses or costs incurred, meaning it could be more or less than the economic damage sustained by the insured.

For DeFi protocols, this risk is particularly acute. A liquidity pool might be drained by a smart contract exploit, but if the parametric trigger relies on an oracle reporting a price drop rather than the exploit itself, the insurance may not pay out. Conversely, a minor price dip might trigger a payout even if the protocol’s core assets remain secure. Understanding this misalignment is critical when designing risk transfer mechanisms.

To manage basis risk, insurers and protocols must carefully select triggers that closely correlate with actual loss events. This often requires complex data modeling and multiple layers of verification. While it adds complexity, it is the only way to ensure the insurance provides meaningful protection rather than just speculative payouts.

| Feature | Indemnity Insurance | Parametric Insurance |

|---|---|---|

| Payout Speed | Weeks to months | Days or hours |

| Cost | Higher premiums | Lower premiums |

| Basis Risk | None | High |

| Complexity | High claims process | Simple data trigger |

Real-world DeFi insurance examples

Parametric insurance is no longer a theoretical concept; it is actively protecting DeFi protocols from specific, measurable risks. By replacing traditional loss verification with on-chain data oracles, these structures offer instant liquidity when markets move against positions. This speed is critical in crypto, where seconds can mean the difference between a liquidation and a solvency event.

Yield protection and liquidation buffers

One of the most common applications is protecting yield-bearing positions. Protocols like Euler Finance (now in liquidation) and various lending markets use parametric triggers to cover short-term liquidity crunches. If a token’s price drops below a specific threshold on-chain, the insurance pool automatically releases funds to cover the shortfall, preventing a cascade of liquidations. This acts as a circuit breaker, stabilizing the protocol without requiring manual intervention or lengthy claims processes.

Stablecoin de-pegging coverage

Stablecoins face existential risk during de-pegging events. Parametric insurance contracts can be written to pay out if a stablecoin’s price falls below a certain percentage of its $1.00 peg for a sustained period. This protects holders and the protocol’s stability by providing immediate capital to buy back tokens and restore the peg. The trigger is binary and objective: if the oracle reports the price is below the threshold, the payout executes. This removes ambiguity and ensures that capital is available exactly when market confidence is lowest.

Basis risk and transparency

While these examples show the power of on-chain data, they also highlight the inherent basis risk of parametric models. As noted by Wharton’s Impact Institute, the payout may not perfectly match the actual economic damage sustained. If the oracle data is slightly off or the trigger threshold is set too narrowly, the payout might be insufficient. However, the transparency of on-chain execution means these risks are visible and calculable, allowing sophisticated users to price them into their strategies.

As an Amazon Associate, we may earn from qualifying purchases.

Is parametric insurance worth the basis risk?

The speed of parametric insurance is its primary selling point, but it comes with a specific trade-off known as basis risk. Unlike traditional insurance, payouts are triggered by objective data points—such as a specific earthquake magnitude or rainfall level—rather than an assessment of your actual financial loss. This means the payout might not perfectly align with your real-world damages.

According to the Wharton Risk Center, this disconnect is the main drawback of the model. The payout could be higher or lower than the economic damage sustained. For example, if a parametric policy triggers because wind speeds hit 100 mph, but your roof only sustains minor damage, you might receive a large payout for little loss. Conversely, if the wind hits 99 mph and destroys your home, you receive nothing.

In the context of DeFi risk transfer, this basis risk is managed through smart contract logic. The "worth" of the insurance depends on how closely the chosen onchain data oracle matches the actual risk exposure of the protocol. If the data feed is accurate, the speed and transparency outweigh the imperfection of the payout.

No comments yet. Be the first to share your thoughts!