How to build a parametric insurance strategy

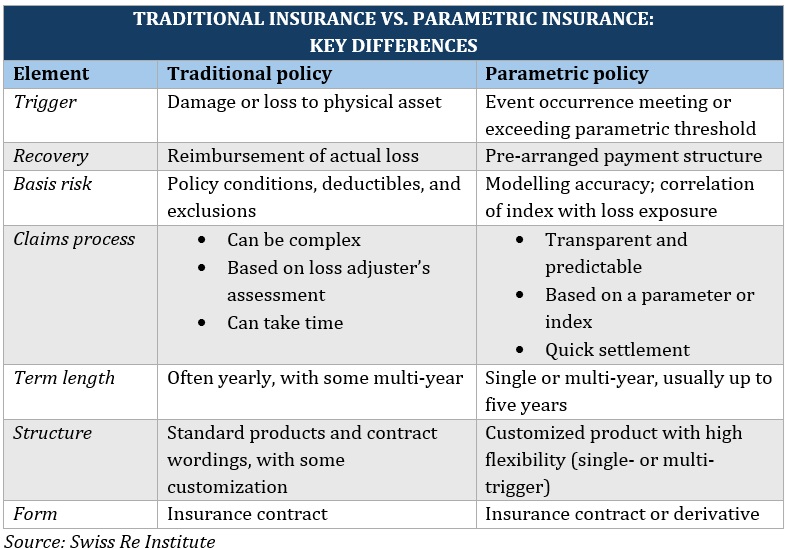

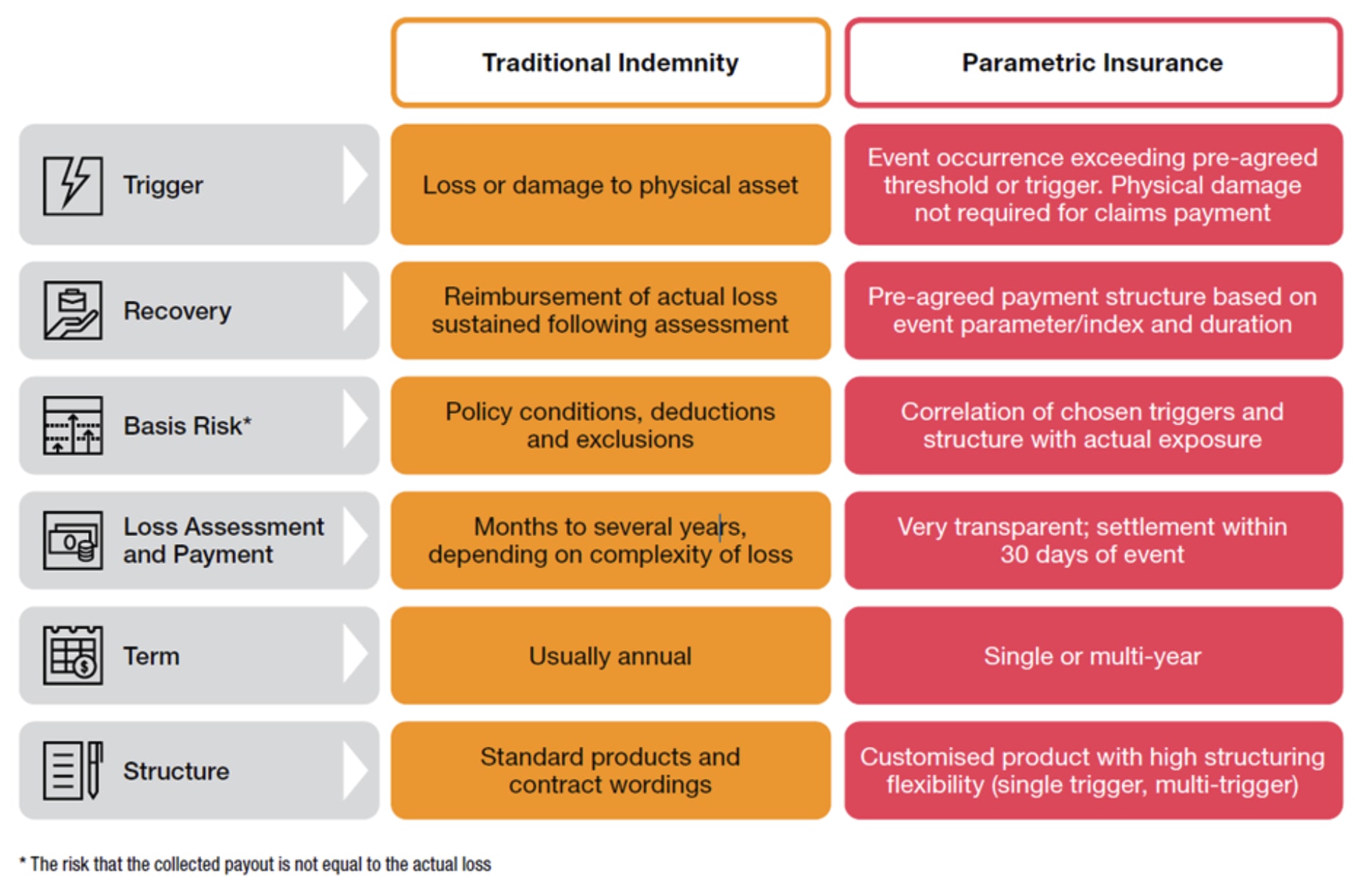

Parametric insurance replaces traditional claims assessments with pre-defined triggers. Instead of waiting for adjusters to verify losses, payouts execute automatically when specific data points—like rainfall levels or wind speeds—cross a set threshold. This model offers rapid liquidity and transparency, making it ideal for DeFi risk transfer where speed and verifiability are paramount.

For DeFi protocols, this means shifting from indemnity-based coverage to index-based protection. The strategy hinges on selecting reliable oracles and clear trigger conditions. If the data source fails or the trigger is ambiguous, the payout logic breaks. Therefore, your first step is auditing the oracle infrastructure to ensure it cannot be manipulated or stalled during critical market events.

Next, define the trigger metrics with precision. Vague conditions lead to disputes or failed payouts. For example, a protocol might trigger a payout if the price of ETH drops below $2,000 for more than 10 minutes on a specific oracle chain. This clarity allows for instant settlement, preserving capital during flash crashes or liquidity crises. The goal is to remove human judgment from the payout equation entirely.

Finally, backtest your strategy against historical market events. Analyze how your triggers would have performed during past volatility spikes. Did they protect the protocol? Did they trigger unnecessarily? This proof check ensures your coverage aligns with actual risk exposure, not just theoretical models. Without rigorous backtesting, parametric insurance becomes a gamble rather than a hedge.

Parametric insurance strategy choices that change the plan

Integrating onchain coverage into a DeFi risk transfer strategy requires balancing speed against precision. Traditional indemnity models rely on loss adjustment, which introduces delays and subjective claims processing. Parametric insurance replaces this with pre-defined triggers—such as price drops or volatility spikes—that automate payouts once specific conditions are met.

This shift offers immediate liquidity during market stress, a critical feature for protocols requiring rapid capital preservation. However, the reliance on external data introduces basis risk. If the trigger does not perfectly correlate with your actual portfolio loss, you may face underinsurance or overinsurance. Evaluating these tradeoffs is essential for designing a robust hedge.

The following comparison breaks down the key variables to consider when selecting a parametric structure.

| Factor | Parametric Structure | Traditional Indemnity |

|---|---|---|

| Payout Speed | Automated; often within days or hours | Manual review; weeks to months |

| Basis Risk | High; trigger may not match actual loss | Low; payout reflects verified loss |

| Transparency | High; smart contract logic is public | Low; claims process is opaque |

| Cost Structure | Lower administrative overhead | Higher adjuster and legal fees |

| Complexity | Moderate; requires precise trigger design | Low; standard policy language |

When designing your strategy, prioritize triggers that align with your specific exposure. For example, a protocol holding stablecoins might use a de-pegging event as a trigger, while an LP position might use an impermanent loss threshold. Always backtest your triggers against historical market data to ensure they would have paid out during past volatility events. This due diligence minimizes the gap between the index movement and your actual financial impact.

How to structure onchain parametric coverage

Integrating parametric insurance into DeFi requires shifting from subjective loss assessment to automated, data-driven triggers. Unlike traditional indemnity policies that rely on adjusters and lengthy claims processes, parametric contracts execute payouts when predefined external metrics hit specific thresholds. This structure aligns well with the speed and transparency requirements of decentralized finance, where liquidity can vanish in seconds during market stress.

To build a robust framework, you must first define the risk parameters with precision. The goal is to eliminate ambiguity in the trigger mechanism so that execution is inevitable and immediate once the condition is met. This section outlines the practical steps to structure this coverage effectively.

Begin by isolating the specific exposure you need to hedge. In DeFi, this is rarely general "market risk" but rather specific events like a stablecoin depeg, a major protocol exploit, or a sharp drop in a correlated asset. Define the exact event that would cause unacceptable losses to your portfolio. For example, if you hold a large position in ETH, a drop below a specific price level against USD or BTC might be the trigger, not general market volatility.

The integrity of your policy depends entirely on the data source. Choose oracles with proven track records and high availability, such as Chainlink or Pyth Network. Avoid single-source data feeds for critical triggers. Verify that the oracle provides the specific data point you need (e.g., a 1-hour TWAP rather than a spot price) to prevent manipulation or flash crash false positives. The oracle must be able to report the trigger condition on-chain or to a trusted off-chain verifier that interacts with the smart contract.

Set clear, binary conditions for the trigger. This could be a price falling below $1.99 for a stablecoin or wind speeds exceeding 100 mph in a real-world asset scenario. Determine the payout curve: is it a fixed lump sum upon trigger, or does it scale linearly with the severity of the event? Ensure the payout amount covers your calculated exposure. Over-insuring ties up capital in premiums, while under-insuring leaves you exposed. The trigger must be objective and verifiable by anyone auditing the blockchain state.

Before deploying mainnet funds, simulate the trigger conditions in a testnet environment. Verify that the oracle reports correctly under stress and that the payout function executes as intended. Check for edge cases, such as what happens if the oracle delays reporting or if the price feed is temporarily unavailable. This step is critical to ensure that the "if-then" logic holds up under real-world network congestion or oracle failure scenarios.

| Feature | Traditional Insurance | Parametric Onchain |

|---|---|---|

| Payout Trigger | Loss assessment & claims | Pre-defined data threshold |

| Payout Speed | Weeks to months | Minutes to hours |

| Dispute Risk | High (subjective) | Low (objective data) |

| Transparency | Low (private contracts) | High (on-chain code) |

By following these steps, you create a coverage layer that operates independently of human intervention. This reduces counterparty risk and ensures that liquidity is available when you need it most, turning your DeFi strategy into a more resilient, automated system.

Spotting Weak Options in Onchain Coverage

Parametric insurance promises speed by paying out when a specific data point hits a threshold, but the onchain version often hides structural flaws. In DeFi risk transfer, the difference between a robust hedge and a misleading claim usually comes down to three things: the quality of the oracle, the liquidity of the payout pool, and the clarity of the trigger.

Oracle Manipulation Risks

Many onchain policies rely on decentralized oracles to verify triggers like price drops or weather events. If the oracle source is thin or easily manipulated, the trigger can fire incorrectly, leaving you with either a worthless policy or an unexpected payout that doesn't match your actual loss. Always check which oracle feeds the policy uses and whether they have a history of stability during high-volatility events.

Liquidity and Payout Delays

A common mistake is assuming that "parametric" means instant cash. While the trigger might be automatic, the actual transfer of funds depends on the liquidity available in the smart contract's reserve. If the pool is underfunded during a systemic crisis, you may face delays or partial payouts. Look for policies with dedicated liquidity pools or reinsurance backing to ensure funds are available when needed.

Vague Trigger Definitions

Some policies use ambiguous trigger conditions that are open to interpretation. For example, a "major storm" might be defined by wind speed, but if the data source only reports gusts rather than sustained winds, the payout might not align with your damage. Read the policy's data source specifications carefully to ensure the trigger matches your actual risk exposure.

Parametric insurance strategy: what to check next

Before integrating onchain coverage, it helps to understand the mechanics and limitations of parametric triggers. Unlike traditional indemnity policies, these contracts rely on predefined data points rather than loss assessments.

No comments yet. Be the first to share your thoughts!