What parametric insurance actually is

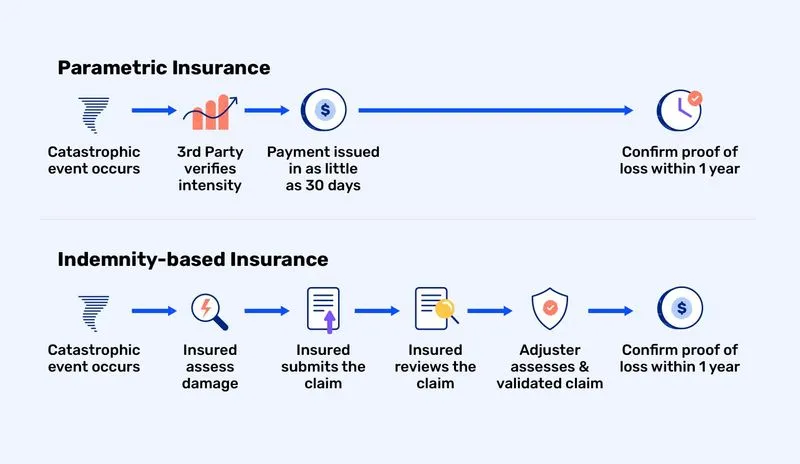

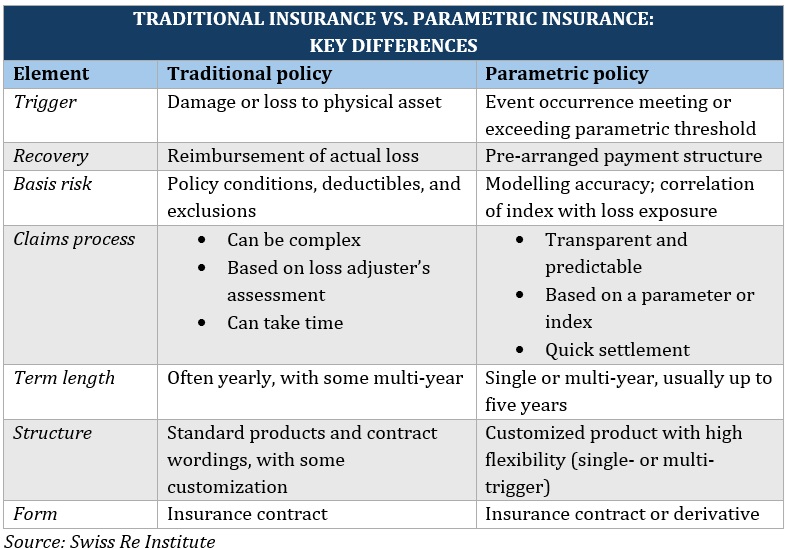

Parametric insurance is a distinct asset class that separates payout from loss assessment. Unlike traditional indemnity insurance, which compensates you for the actual damage suffered, parametric insurance pays out a predetermined amount when a specific, measurable event occurs. This shift transforms risk transfer from a claims-based process into an index-based contract.

The core mechanism relies on a trigger. This trigger is an objective data point, such as wind speed, earthquake magnitude, or rainfall levels. When the data confirms the threshold has been breached, the contract activates automatically. There is no need to adjust for inflation, negotiate repair costs, or wait for an adjuster to visit the site. The payout is binary: either the index hits the mark, or it does not.

This structure is particularly valuable for filling protection gaps left by traditional policies. Swiss Re notes that parametric solutions expand coverage beyond physical assets, addressing deductibles and excluded perils that often leave individuals or businesses exposed. For instance, a farmer might not be compensated for a crop failure under a standard policy if the cause is ambiguous, but a parametric contract tied to local rainfall data will pay out if rain falls below a set threshold.

In the context of DeFi infrastructure, this mechanism offers real-time risk transfer. Smart contracts can verify on-chain or oracle-fed data instantly, removing the administrative lag inherent in traditional insurance. This makes parametric insurance a powerful tool for rapid liquidity injection during crises, whether for natural disasters, supply chain disruptions, or market volatility.

DeFi infrastructure as the settlement layer

Traditional parametric insurance relies on a central authority to verify data and trigger payouts. If that authority is slow, biased, or compromised, the promise of instant relief vanishes. DeFi infrastructure replaces this human bottleneck with code. By moving the settlement layer onto a blockchain, parametric insurance becomes trustless, transparent, and automated.

Smart contracts replace actuarial processing

In conventional insurance, actuaries spend weeks modeling risk and adjusting premiums based on historical data. Parametric models simplify this by tying payouts to objective, measurable events—such as wind speed exceeding 100 mph or rainfall dropping below a specific threshold. The smart contract encodes these thresholds directly. When the predefined condition is met, the payout executes automatically. There is no claims adjuster, no paperwork, and no delay. The code acts as the sole arbiter of truth.

Oracle networks provide the data

Smart contracts cannot interact with the outside world on their own. They require oracles—bridges that fetch real-world data and feed it into the blockchain. For parametric insurance, these oracles pull data from trusted sources like meteorological agencies or seismic monitors. The integrity of the payout depends entirely on the accuracy of these oracles. If the oracle reports false data, the contract executes incorrectly. This is why reputable parametric platforms use decentralized oracle networks to prevent single points of failure and manipulation.

Transparency and immutability

Once deployed, the terms of a parametric insurance policy are immutable. Neither the insurer nor the insured can alter the conditions or the payout structure. This transparency builds trust. Buyers can audit the smart contract code to verify exactly what triggers a payout and how much they will receive. Sellers can demonstrate their solvency by holding collateral in the contract. This open-book approach reduces the information asymmetry that often plagues traditional insurance markets.

Real-time settlement

The most significant advantage of DeFi infrastructure is speed. In a traditional system, a disaster claim can take months to settle. In a parametric system, settlement can occur in minutes or even seconds after the data oracle confirms the event. This immediacy is critical for businesses and individuals trying to recover from catastrophic losses. Liquidity is available exactly when it is needed most, without waiting for administrative processing.

How oracles feed the trigger

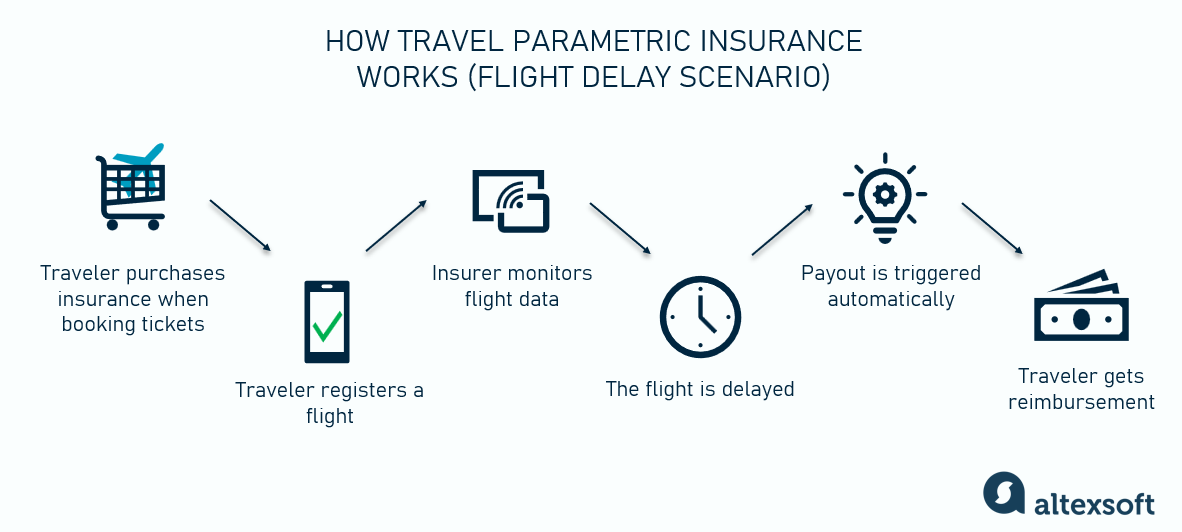

Parametric insurance removes the need for claims adjusters, but it introduces a new dependency: data. Smart contracts cannot observe the physical world on their own. They require a reliable feed of external information to determine whether a payout is due. This is where oracle networks come in. They act as the bridge between off-chain reality and on-chain execution, ensuring the contract reacts only to verified events.

The mechanism is straightforward but critical. An oracle monitors a specific metric—such as wind speed, earthquake magnitude, or flight delay duration—and pushes that data to the blockchain. When the metric crosses a predetermined threshold, the smart contract automatically executes the payout. This eliminates the ambiguity of traditional insurance, where coverage depends on interpreting policy language after a loss occurs. Instead, the trigger is binary: the data either meets the condition, or it does not.

For this system to work, the oracle must be accurate and tamper-resistant. If the data feed is compromised or delayed, the contract may pay out incorrectly or fail to pay when it should. Reputable oracle networks use multiple data sources and consensus mechanisms to minimize the risk of a single point of failure. This reliability is what allows parametric insurance to function as a legitimate risk transfer tool in high-stakes environments, providing immediate liquidity when it is needed most.

How DeFi Capital Moves Faster Than Traditional Reinsurance

Traditional reinsurance relies on slow-moving capital markets. A reinsurer must underwrite risk, set premiums, and wait for claims verification before disbursing funds. This process can take months, leaving policyholders exposed during the critical recovery window.

DeFi liquidity pools offer a different model. Capital is pre-funded and locked in smart contracts, ready to execute automatically when parametric triggers are met. This shifts the bottleneck from claims processing to capital availability.

The contrast is stark. Traditional reinsurance provides deep capital reserves but suffers from liquidity friction. DeFi pools offer instant access but depend on the depth of the specific liquidity pool. Understanding this trade-off is essential for evaluating parametric insurance as a risk transfer tool.

| Feature | Traditional Reinsurance | DeFi Liquidity Pools |

|---|---|---|

| Capital Access | Slow (months) | Instant (seconds) |

| Verification | Claims assessment | Oracle trigger |

| Cost Structure | High overhead | Low overhead |

| Accessibility | Limited to large entities | Open to global participants |

This structural difference allows DeFi to address gaps in traditional markets, particularly for smaller, frequent risks where administrative costs outweigh potential payouts. However, it also introduces new risks related to smart contract security and oracle reliability.

Regulatory hurdles and compliance

Parametric insurance sits at the intersection of two distinct worlds: traditional insurance and decentralized finance. This dual nature creates a complex regulatory environment where jurisdiction matters more than technology. Insurers must navigate a patchwork of rules that were not designed for onchain settlement or algorithmic triggers.

The International Actuarial Association (IAA) outlines the core requirement for any product to be recognized as insurance: an insurable interest and a clear link between the index and the loss. Without this foundational connection, regulators may classify parametric products as financial derivatives rather than insurance, triggering entirely different compliance frameworks. This distinction is critical for capital reserves and consumer protection.

Consult CounselThe Financial Stability Institute (FSI) of the Bank for International Settlements (BIS) has highlighted that while parametric insurance offers speed and transparency, it also introduces new systemic risks. Regulators are currently debating how to apply existing solvency standards to smart contracts that execute automatically. The lack of unified global standards means a product compliant in one jurisdiction may face legal challenges in another.

For DeFi infrastructure providers, this means building compliance into the protocol layer. This includes KYC/AML checks for policyholders, transparent oracle verification processes, and clear dispute resolution mechanisms. As the market matures, we expect more jurisdictions to create specific sandboxes for parametric products, allowing for innovation while maintaining consumer safeguards.

Evaluating Parametric Risk Transfer Options

Before deploying capital into a DeFi protocol, risk managers must verify that the solution aligns with their specific exposure. Parametric insurance removes basis risk—the gap between the index payout and actual loss—but only if the underlying mechanics are sound. Use this checklist to determine if a protocol fits your risk profile.

Ensure the trigger directly correlates to your business loss. For a logistics firm, a wind speed index may not capture port closure delays. The index must be granular enough to avoid basis risk while remaining objective and verifiable.

Smart contracts rely on oracles to fetch external data. Choose protocols that aggregate data from multiple reputable sources (e.g., NOAA, major exchanges) to prevent a single point of failure or manipulation. Check if the oracle has a proven track record of uptime.

DeFi protocols are immutable once deployed. Verify that the code has been audited by reputable firms like OpenZeppelin or Trail of Bits. Look for a bug bounty program and a history of transparent vulnerability disclosures.

Determine if the protocol operates within your jurisdiction’s legal framework. Some regions classify parametric tokens as securities or require specific licensing for risk transfer mechanisms. Consult legal counsel to ensure the structure doesn’t violate local insurance laws.

| Feature | Traditional | Parametric |

|---|---|---|

| Payout Speed | Months | Minutes |

| Basis Risk | Low | High |

| Underwriting Cost | High | Low |

Parametric solutions offer speed and lower overhead, but they demand rigorous due diligence. If your risk profile is highly specific and traditional insurers are unavailable, DeFi parametric insurance may be the right fit—provided the infrastructure is robust.

No comments yet. Be the first to share your thoughts!