Defining the parametric insurance strategy

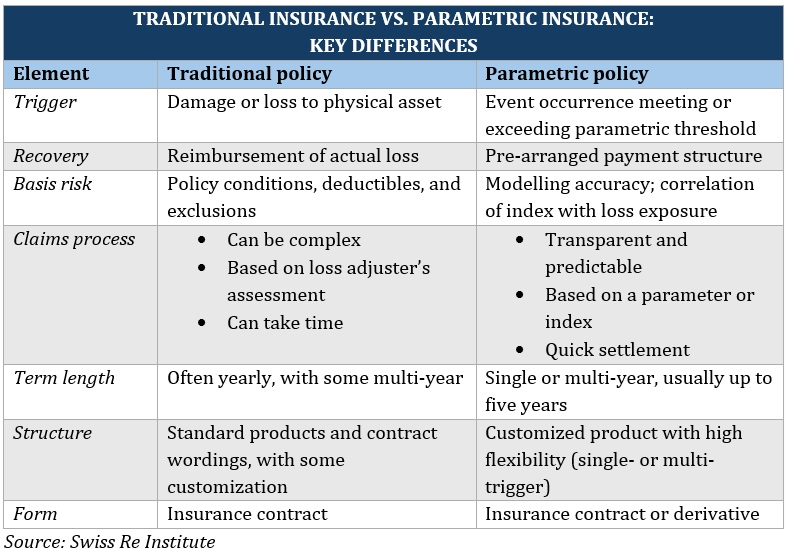

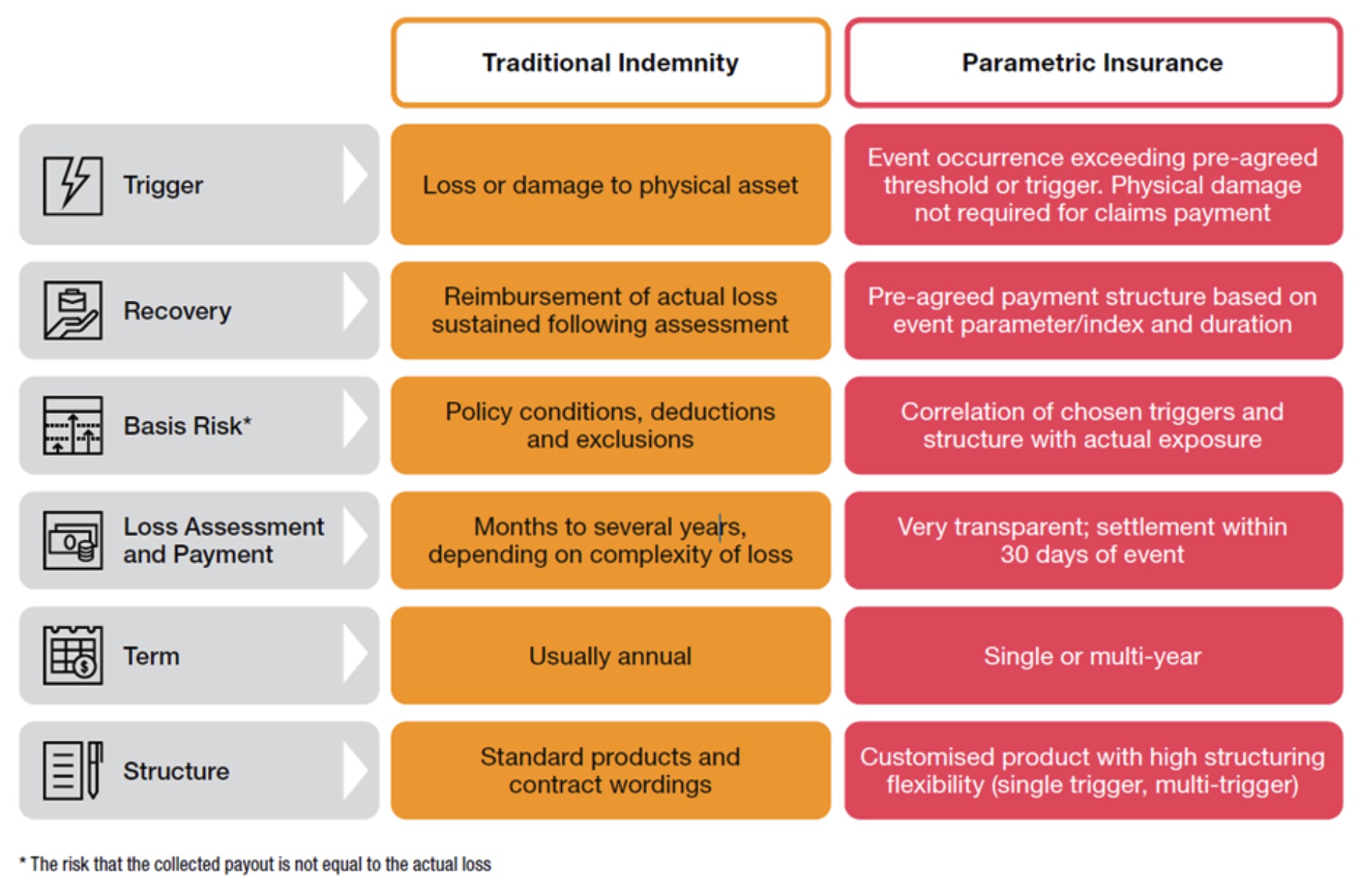

Parametric insurance is a risk transfer mechanism that pays out based on a predefined, objective trigger rather than an assessment of actual losses. In traditional indemnity models, claims are settled after a detailed investigation into the extent of damage—a process that can take months. Parametric insurance eliminates the subjective loss-adjustment phase entirely. Instead, it relies on verified data points, such as oracle price feeds or protocol exploit signatures, to determine if a payout should occur.

This distinction is critical for high-stakes digital asset management. When a DeFi protocol suffers a flash loan attack or a stablecoin depegs, the window for effective mitigation is measured in minutes, not months. Traditional insurance cannot operate at this speed. Parametric structures, however, can execute smart contract payouts automatically the moment the trigger condition is met, providing immediate liquidity to cover losses or stabilize the ecosystem.

The National Association of Insurance Commissioners (NAIC) notes that this model offers faster payouts after disasters by paying set amounts based on event parameters rather than losses. In the context of DeFi, this means capital preservation is not left to the discretion of an adjuster but is enforced by code. This transparency and speed make parametric insurance a foundational component of modern DeFi risk strategies, particularly for protocols handling significant value where downtime or insolvency poses systemic risk.

Onchain infrastructure for coverage

Parametric insurance removes the need for traditional loss adjustment by relying on code and data rather than human judgment. In DeFi, this means the entire lifecycle—from premium collection to automatic payout—is governed by smart contracts. The system works only if the underlying data is trustworthy; if the input is flawed, the output is useless. This "garbage in, garbage out" reality makes the technical backbone the most critical component of any coverage strategy.

The core of this infrastructure is the oracle. Oracles act as the bridge between off-chain reality and on-chain execution. They fetch external data, such as weather reports or price feeds, and deliver it to the smart contract. Because smart contracts cannot initiate requests themselves, they rely on decentralized oracle networks to provide this data. If an oracle is compromised or provides delayed information, the payout logic fails. Therefore, selecting a robust oracle network is not just a technical choice; it is a risk management decision.

Data feeds must be deterministic and tamper-resistant. For financial triggers, this often involves aggregating prices from multiple exchanges to prevent single-point failures. For non-financial triggers, such as earthquake magnitude, the data must come from a verified scientific source. The contract then compares this incoming data against the predefined parameters. If the threshold is met, the contract automatically executes the payout to the policyholder's wallet, eliminating administrative delays and reducing counterparty risk.

To visualize how these triggers work, consider an ETH price drop protocol. If the price of ETH falls below a certain threshold within a specific time window, the contract pays out. A technical chart helps illustrate the volatility that might trigger such a clause, showing how rapid market movements can activate coverage without human intervention.

This infrastructure shifts the focus from claims processing to data integrity. By automating the verification process, parametric insurance offers speed and transparency that traditional models struggle to match. However, it requires a deep understanding of the technical components involved. Users must ensure that the smart contracts are audited and that the data sources are reliable, as there is no manual override in case of error.

Key use cases in DeFi risk transfer

Parametric insurance addresses the most painful friction in decentralized finance: the gap between a loss event and actual compensation. In traditional insurance, adjusting claims for smart contract exploits or protocol failures can take months, during which capital remains frozen and users abandon the platform. Parametric policies replace subjective loss assessment with objective, on-chain triggers, turning risk transfer from a bureaucratic hurdle into an automated settlement.

Smart Contract Failure and Exploit Coverage

The most immediate application of parametric insurance is protecting against code vulnerabilities. Rather than waiting for legal consensus on negligence, these policies activate when a verified exploit occurs. Triggers are typically tied to on-chain events, such as a specific amount of ETH drained from a protocol within a defined time window, or a confirmed incident report from a reputable security auditor like CertiK or OpenZeppelin.

This approach ensures that liquidity is restored almost immediately after a breach, preserving user confidence. For example, if a lending protocol suffers a flash loan attack that drains $5 million, the parametric payout can be executed automatically via a multisig wallet once the oracle confirms the event. This speed is critical in DeFi, where reputation damage spreads faster than any traditional claims process.

Liquidity Pool and Impermanent Loss Protection

Liquidity providers face unique risks, including impermanent loss and pool-specific exploits. Parametric products can be structured to cover scenarios where the value of a token pair deviates beyond a predetermined threshold relative to an external oracle price. If the price of ETH/USDC in a specific pool diverges from the Chainlink oracle by more than 5% due to a manipulation attack, the liquidity provider receives a payout proportional to their share.

This mechanism separates market volatility from protocol-specific failures. By indexing triggers to oracle data rather than subjective pool performance metrics, insurers can accurately price the risk of manipulation without needing to audit every transaction in real-time. It provides a safety net for high-yield strategies that are inherently more vulnerable to market stress.

Extreme Market Volatility and De-pegging Events

DeFi is highly sensitive to systemic shocks, such as stablecoin de-pegging or cascading liquidations during sharp market downturns. Parametric insurance can act as a circuit breaker, providing capital injections when the broader market experiences extreme stress. Triggers might be based on the price of Bitcoin or Ethereum falling below specific levels on major exchanges, or a stablecoin’s price dropping below $0.95 for more than 24 hours.

These policies help stabilize protocols during black swan events. For instance, if a major stablecoin de-pegs, a parametric payout to a lending platform can prevent a cascade of forced liquidations that would otherwise wipe out user collateral. This type of coverage transforms volatility from an existential threat into a manageable, priced risk, allowing protocols to operate with higher leverage and deeper liquidity.

Comparison: Traditional vs. Parametric in DeFi

The shift from traditional indemnity models to parametric triggers changes the fundamental economics of risk in DeFi. Traditional insurance relies on post-event investigation, which is often impossible in anonymous, irreversible blockchain environments. Parametric insurance relies on pre-defined data points, making it the only viable model for many high-frequency, high-volume DeFi interactions.

| Feature | Traditional Insurance | Parametric Insurance |

|---|---|---|

| Trigger Mechanism | Subjective loss assessment | Objective on-chain data |

| Payout Speed | Months to years | Hours to days |

| Basis Risk | Low (covers actual loss) | Higher (payout may not match exact loss) |

| Cost | High (underwriting & legal) | Lower (automated settlement) |

Managing basis risk in parametric models

Basis risk remains the single most significant vulnerability in parametric insurance. It occurs when the index or trigger activates a payout despite the user suffering no actual loss, or conversely, fails to pay out when the user has genuinely lost capital. In traditional insurance, indemnity is calculated based on the specific damage to an asset. In DeFi, however, coverage is tied to external data points—such as a price drop on a major exchange or a volatility spike—that may not perfectly mirror the conditions of the insured portfolio.

This disconnect is particularly acute in decentralized finance, where assets are fragmented across multiple chains and liquidity pools. A trigger based on the price of ETH on Coinbase might activate due to a liquidity crunch on that specific exchange, while the user’s ETH remains safely locked in a cold wallet or a different protocol with stable liquidity. According to PwC, this misalignment creates a fundamental challenge where the insurance product functions more like a speculative derivative than a true hedge against loss.

To mitigate basis risk, modelers must prioritize correlation over simplicity. Instead of relying on a single, broad market index, strategies should incorporate composite indices or multi-source oracle feeds that aggregate data from several reputable exchanges. This approach smooths out idiosyncratic volatility and ensures that the trigger reflects broader market movements rather than isolated exchange anomalies. Additionally, incorporating a minimum loss threshold—where payouts only occur if the user’s portfolio has also dipped below a certain value—can significantly reduce false positives, aligning the parametric payout more closely with actual economic harm.

Steps to implement your strategy

Adopting parametric insurance for DeFi risk transfer requires a structured approach. Unlike traditional indemnity models, this strategy relies on data oracles and predefined triggers to automate payouts. Follow these steps to build a resilient framework.

Begin by isolating the specific smart contract or market risks you need to hedge. In DeFi, this often means targeting price volatility, liquidity pool exploits, or oracle failures. Define the exact exposure limits that threaten your portfolio’s solvency.

Your insurance policy is only as strong as its data source. Choose decentralized oracle networks with proven track records for accuracy and resistance to manipulation. The oracle feeds the trigger; if the data is compromised, the payout logic fails.

Set precise, binary conditions for payout. Avoid subjective metrics. For example, a trigger might activate if ETH drops below $1,800 on a major exchange within a 15-minute window. Clear definitions prevent disputes and ensure immediate liquidity when volatility strikes.

Evaluate parametric insurance protocols based on their capitalization, smart contract audits, and historical claim settlement speed. Prioritize providers with transparent on-chain reserves and robust governance models to ensure they can meet obligations during market stress.

Frequently asked questions about parametric insurance

How does parametric insurance handle basis risk in DeFi?

Basis risk occurs when the parametric trigger activates a payout that does not match the user's actual financial loss, or fails to pay out when a loss occurs. To manage this, strategies often use composite indices or multi-source oracle feeds to smooth out idiosyncratic volatility. Additionally, incorporating a minimum loss threshold ensures payouts only occur if the user’s portfolio has also dipped below a certain value, aligning the trigger more closely with actual economic harm.

What are the primary risks of using parametric insurance in DeFi?

The primary risk is basis risk, where the trigger event does not align with your actual financial loss. For example, a protocol might suffer a hack that doesn't meet the predefined "TVL drop" threshold, leaving you uninsured. Additionally, data oracle failures can lead to incorrect trigger executions. It is essential to choose providers with robust, decentralized oracle networks to minimize the chance of manipulation or technical failure.

How does parametric insurance differ from traditional insurance in DeFi?

Traditional insurance relies on subjective loss assessment, which can take months to resolve. Parametric insurance removes the adjuster from the equation. The policy is binary: either the trigger event occurred, or it did not. This structure offers transparency and speed, making it ideal for the fast-moving DeFi ecosystem where liquidity crises can escalate in minutes. The trade-off is basis risk, where the trigger may not perfectly correlate with every individual user's loss.

No comments yet. Be the first to share your thoughts!