Why parametric insurance fits DeFi

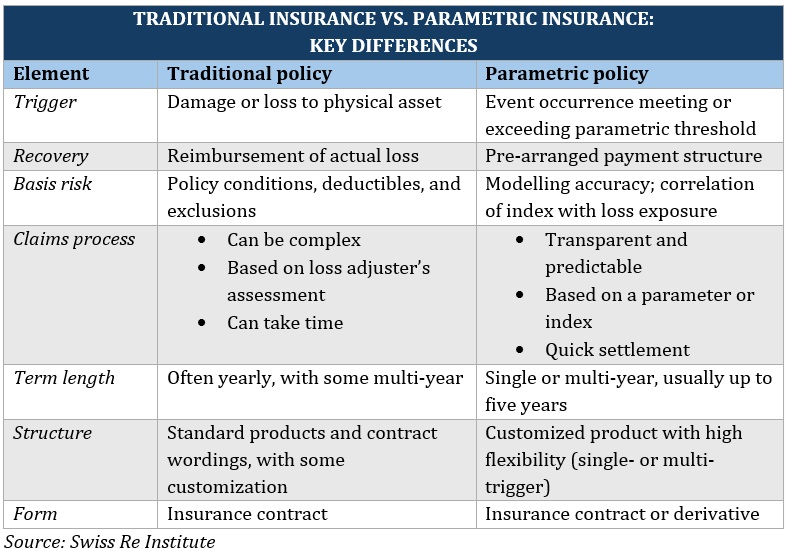

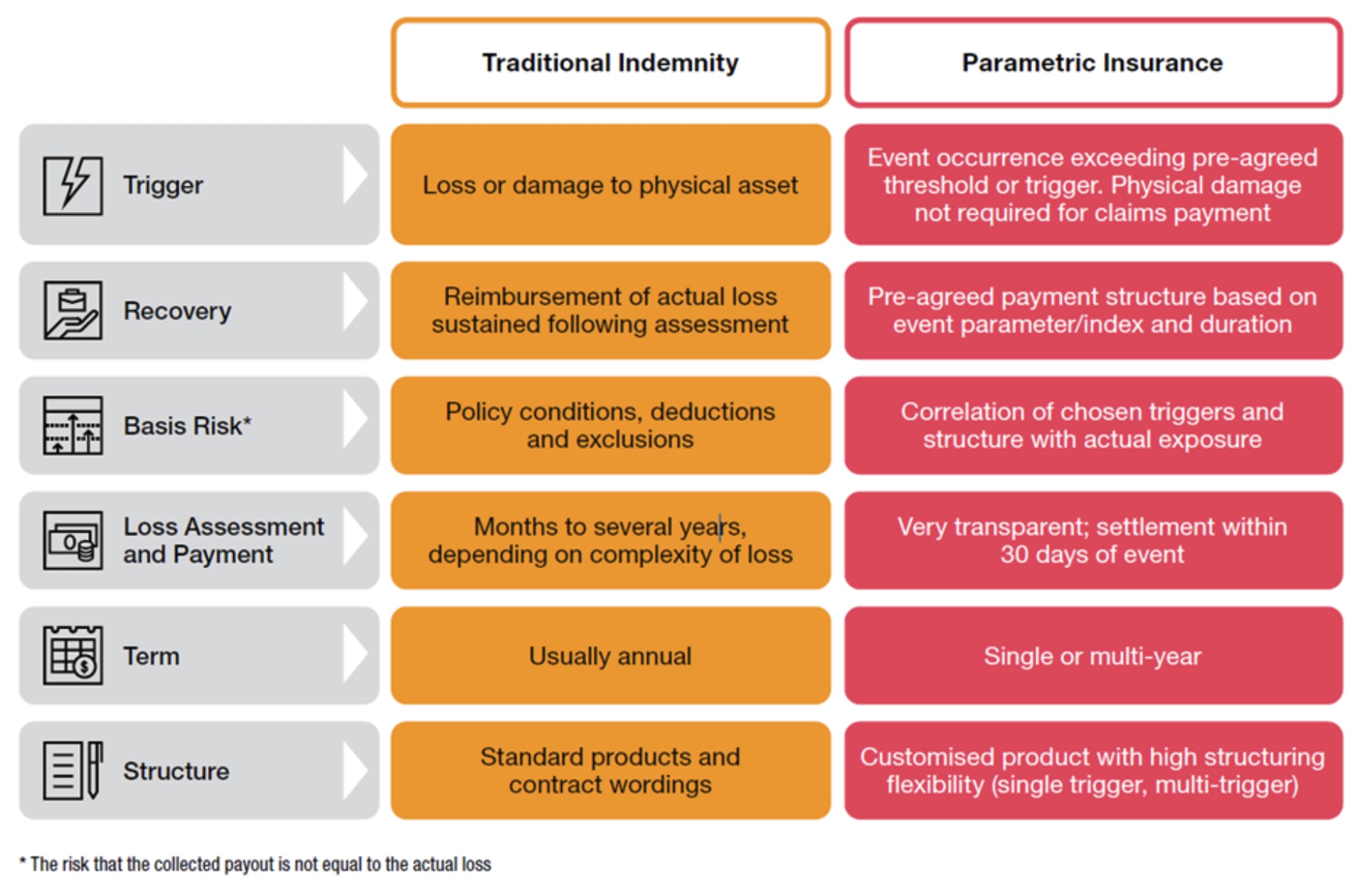

Traditional indemnity insurance relies on post-loss assessments to determine payout amounts. In the DeFi space, this model is too slow and opaque. When a smart contract exploit or oracle failure occurs, the window for liquidity recovery is measured in minutes, not weeks. By the time an adjuster verifies the damage, the funds are often already drained or the protocol is insolvent.

Parametric insurance removes the need for subjective loss assessment. Instead of proving actual damage, payouts are triggered by objective, on-chain data. If a specific price threshold is breached or a transaction hash indicates a known exploit pattern, the smart contract automatically releases the funds. This shifts the focus from "how much was lost?" to "did the event occur?"

This approach aligns with the core values of DeFi: transparency and automation. A well-designed parametric insurance strategy ensures that capital remains liquid even during market stress, turning insurance from a passive safety net into an active risk management tool.

Designing onchain parametric triggers

Building a parametric insurance strategy for DeFi requires replacing subjective claims adjustment with deterministic code. The core challenge is defining a "trigger"—a specific, measurable event—that automatically releases funds without human intervention. This architecture relies on the seamless interaction between oracles, price feeds, and smart contracts to ensure that payouts are both immediate and immutable.

At the heart of this system is the oracle. In traditional insurance, an adjuster visits a site to verify damage. In DeFi, an oracle acts as the bridge between off-chain reality and on-chain logic. It fetches external data, such as weather station readings or market volatility indices, and feeds it into the smart contract. The reliability of the entire system hinges on the oracle's integrity; if the data source is compromised, the payout logic fails. Protocols often use decentralized oracle networks to aggregate data from multiple sources, reducing the risk of a single point of failure.

Once the oracle provides the data, the smart contract evaluates it against predefined thresholds. These thresholds are the "parametric" part of the strategy. For example, a contract might be coded to pay out if the price of ETH drops below a certain level within a 24-hour window, or if wind speeds exceed 100 mph in a specific geographic region. This binary logic—either the condition is met, or it is not—eliminates ambiguity and dispute. The payout is not based on the actual financial loss suffered by the user, but on the severity of the trigger event itself.

To illustrate how these thresholds function in practice, consider a volatility-based coverage product. The contract monitors a specific price feed, and if the asset's value breaches a set limit, the funds are automatically transferred to the insured wallet. This mechanism ensures liquidity when it is needed most, without the delay of traditional claims processing.

The precision of this design allows for complex risk transfer models. By combining multiple data points—such as correlating price drops with volume spikes—protocols can create more nuanced triggers that better reflect real-world risks. However, this also introduces the risk of "basis risk," where the trigger event does not perfectly align with the user's actual loss. Careful parameter selection is therefore critical to maintaining trust in the coverage.

Liquidity pools as insurance capital

Parametric insurance protocols typically fund payouts through liquidity pools rather than traditional reinsurance markets. This structure creates a direct link between capital efficiency and risk pricing. When you purchase coverage, your premium often goes into a pool that earns yield from lending or staking activities, which can offset the cost of insurance.

| Factor | What to check | Why it matters |

|---|---|---|

| Fit | Match the option to the primary use case. | A good deal still fails if it does not fit the job. |

| Condition | Verify age, wear, and service history. | Hidden condition issues erase upfront savings. |

| Cost | Compare purchase price with likely upkeep. | The cheapest option is not always the lowest-cost option. |

Real-world DeFi risk scenarios

A parametric insurance strategy shifts the focus from proving loss to verifying triggers. In traditional insurance, you wait for an adjuster to assess damage. In DeFi, you need immediate liquidity when a protocol fails. This section breaks down how a parametric approach handles the three most common threats: oracle manipulation, stablecoin depegging, and smart contract exploits.

Oracle manipulation

Oracles feed external data to smart contracts. If an oracle is manipulated, the contract acts on false information. A parametric strategy doesn’t wait for a lawsuit. It monitors oracle health metrics. If the price deviation exceeds a set threshold, the insurance payout triggers automatically. This protects users from flash loan attacks that temporarily skew market prices.

Stablecoin depegging

Stablecoins should always trade at $1.00. When they don’t, liquidity dries up. A parametric policy can track the USD Coin (USDC) price. If USDC drops below $0.95 for more than ten minutes, the policy pays out. This allows traders to exit positions or rebalance portfolios before the depeg worsens. The trigger is objective and verifiable on-chain.

Smart contract exploits

Hacks happen fast. Traditional insurance takes months to settle. A parametric strategy uses a hard-coded exploit threshold. If a protocol loses more than 5% of its total value in a single transaction, the payout activates. This provides immediate capital to cover user withdrawals and stabilize the protocol. It turns a potential catastrophe into a manageable event.

Implementing your coverage workflow

Deploying parametric coverage in DeFi requires treating the protocol like a financial instrument rather than a traditional policy. You are buying a contract that executes automatically based on data, not claims adjusters. This workflow breaks down the deployment into three distinct phases: selecting the right protocol, defining the trigger parameters, and funding the position.

1. Select the Protocol

Start by identifying a protocol that offers the specific coverage type you need, such as smart contract risk or stablecoin depegging. Look for platforms with transparent governance and audited oracle integrations. The reliability of the data source is as important as the smart contract itself. Choose a provider with a track record of payouts during actual market stress events.

2. Define the Trigger

The core of your strategy is the trigger—the specific condition that must be met for a payout to occur. This could be a price drop below a certain threshold, a volatility spike, or a specific blockchain event. Be precise: ambiguous triggers can lead to denied payouts. Use historical data to set thresholds that reflect genuine risk rather than minor market noise. Your trigger should align with the actual threat to your portfolio.

3. Fund and Deploy

Once your parameters are set, deposit the required collateral into the protocol. Most systems require over-collateralization to ensure liquidity for payouts. Monitor your position regularly, as market conditions change. Unlike traditional insurance, you can often adjust your coverage limits or exit the position early, but doing so may result in partial refunds or fees. Treat this as an active management task, not a set-and-forget solution.

No comments yet. Be the first to share your thoughts!