How parametric insurance works

Parametric insurance flips the traditional insurance model on its head. Instead of waiting for an adjuster to assess damage after a loss occurs, these policies pay out automatically when a specific, predefined event hits a certain threshold. Think of it as an insurance policy that pays out based on the weather report rather than the wreckage.

In a standard indemnity policy, the insurer verifies the actual financial loss before paying. This process can take weeks or months, leaving businesses vulnerable during critical recovery periods. Parametric insurance removes the claims adjustment phase entirely. The payout is triggered by objective data—such as wind speed, earthquake magnitude, or rainfall levels—verified by trusted third-party sources.

This mechanism is particularly valuable for filling protection gaps left by traditional coverage, such as deductibles or excluded perils. By relying on transparent, immutable indices, parametric products reduce administrative costs and eliminate disputes over claim validity. The result is a risk transfer tool that prioritizes speed and certainty over post-loss investigation.

DeFi protocols offering coverage

The onchain insurance landscape has matured beyond simple yield farming hacks into structured risk transfer markets. These protocols allow users to hedge specific smart contract risks or broader market volatility using parametric models. Instead of waiting for a human adjuster to approve a claim, payouts trigger automatically when predefined onchain conditions are met, such as a price drop below a certain threshold or a successful exploit detection.

Nexus Mutual

Nexus Mutual is the most prominent decentralized insurance protocol for Ethereum and EVM-compatible chains. It operates on a peer-to-peer model where capital providers (underwriters) pool funds to cover smart contract risks. Users purchase coverage by paying premiums in ETH or stablecoins. If a covered smart contract is exploited, the payout is determined by the severity of the loss, verified by a decentralized claims committee. This model aligns incentives closely with the community, as underwriters are financially responsible for the claims they underwrite. It is particularly effective for DeFi protocols looking to secure their treasury against known vulnerabilities.

Etherisc

Etherisc focuses on parametric insurance for real-world assets, bridging the gap between blockchain and traditional insurance products. Their flagship product, Flight Delay Insurance, pays out automatically when a flight is delayed by more than two hours, using data from aviation APIs. They also offer crop insurance and photo insurance. Etherisc uses oracles to fetch external data, ensuring that the parametric triggers are based on verifiable real-world events rather than onchain price movements. This makes it a practical tool for businesses and individuals seeking protection against operational disruptions.

Arkham Insurance

Arkham provides insurance solutions tailored to the crypto-native audience, focusing on smart contract risk and exchange solvency. Their parametric models are designed to respond quickly to market events, offering coverage for events like exchange hacks or stablecoin depegs. Arkham leverages its data analytics capabilities to assess risk more accurately than traditional models, allowing for more dynamic pricing. This approach appeals to traders and institutions who need immediate liquidity in the event of a market shock, without the delays associated with traditional insurance claims processes.

Comparison of Coverage Models

| Protocol | Primary Risk Type | Payout Trigger | Capital Source |

|---|---|---|---|

| Nexus Mutual | Smart Contract Exploits | Claims Committee Vote | Underwriter Pool |

| Etherisc | Real-World Events | Oracle Data (Flight/Crop) | Insurance Pool |

| Arkham Insurance | Market Volatility & Hacks | Onchain Price/Event Data | Token Staking |

Recommended Reading

For those looking to deepen their understanding of these mechanisms, the following resources provide a solid foundation in DeFi risk management.

As an Amazon Associate, we may earn from qualifying purchases.

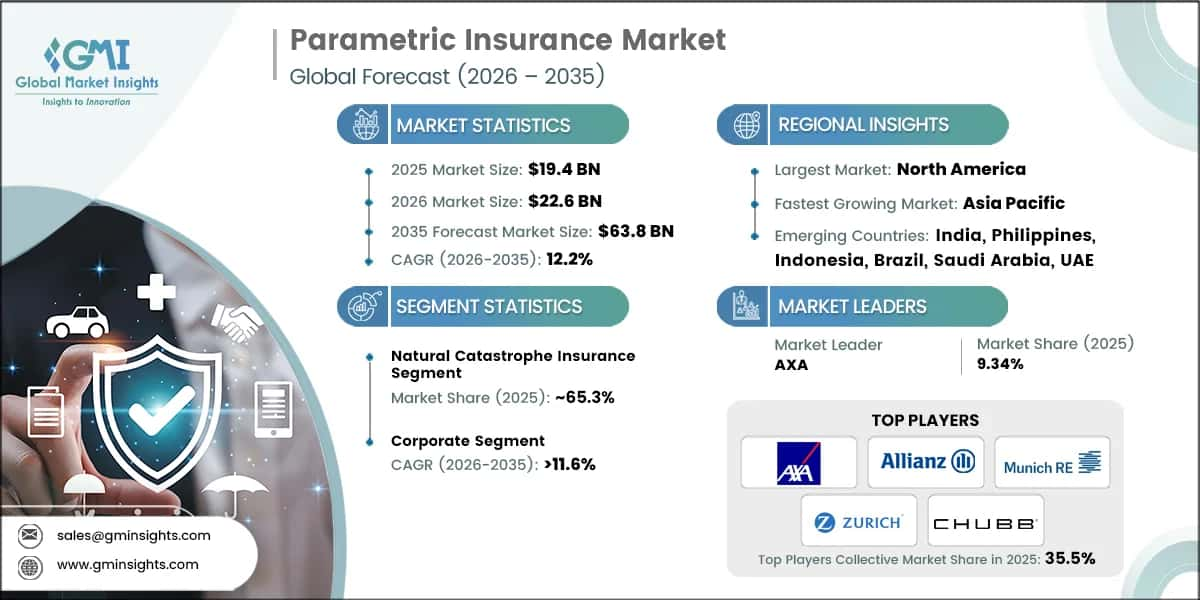

Market trends and adoption data

The parametric insurance market is moving from niche experimentation to a core component of global risk transfer strategies. Driven by the increasing frequency of climate-related events and the need for faster liquidity, adoption is accelerating across both traditional insurance carriers and decentralized finance (DeFi) protocols.

Institutional interest has shifted from theoretical models to tangible deployment. Organizations like the United Nations Development Programme (UNDP) and the International Association of Insurance Supervisors (IAIS) are actively publishing frameworks that standardize parametric triggers. This regulatory clarity is reducing the barrier to entry for institutional capital, allowing pension funds and sovereign wealth funds to allocate capital to parametric risk pools with greater confidence.

The growth trajectory is supported by a dual engine of demand: developing nations seeking financial resilience against natural catastrophes and institutional investors looking for non-correlated assets. As data infrastructure improves, the precision of parametric triggers increases, making these products more attractive to a broader range of risk managers.

To understand the broader market context, it is helpful to look at the performance of related financial instruments. The following chart illustrates the movement of a relevant market index, reflecting investor sentiment toward risk management and alternative insurance assets.

While parametric insurance operates in a specialized niche, its financial mechanics are increasingly integrated with broader crypto and traditional finance markets. The live price data for key assets in this ecosystem often serves as a proxy for market confidence in decentralized risk solutions.

Evaluating Parametric Tools and Indices

Assessing a parametric product requires looking past the marketing and into the mechanics of the index itself. Unlike traditional insurance, which pays based on actual verified losses, parametric insurance triggers payouts when a predefined threshold is met. This shift moves the risk from loss assessment to index reliability. If the index doesn't accurately reflect your exposure, you face basis risk—the gap between the trigger event and your actual financial impact.

The National Association of Insurance Commissioners (NAIC) notes that parametric insurance offers faster payouts by paying set amounts based on event parameters rather than losses. This speed is the primary value proposition, but it comes with a trade-off: precision. You must evaluate whether the chosen metric—whether it be wind speed, earthquake magnitude, or rainfall levels—closely correlates with your specific vulnerability.

To compare the landscape, we look at key parameters across leading DeFi and traditional parametric structures. The table below highlights differences in basis risk, payout speed, and capital efficiency.

| Product Type | Basis Risk Profile | Payout Speed | Capital Efficiency |

|---|---|---|---|

| Traditional Parametric | Low (Customized) | Days to Weeks | Low |

| DeFi Weather Swap | Medium (Standardized) | Hours | High |

| Catastrophe Bond | Low (Broad) | Weeks | Medium |

| On-Chain Index Token | High (Generic) | Minutes | Very High |

When selecting a tool, prioritize indices with transparent data sources. The Climate Policy Initiative emphasizes that parametric insurance pays out if a specific event occurs, rather than based on indemnity. This distinction means your due diligence must focus on the data provider's integrity. A poorly sourced index can lead to false negatives (no payout when you need one) or false positives (payout when you don't). Always verify the oracle or data feed before committing capital.

Building a parametric risk strategy

Integrating parametric insurance into your broader risk management plan requires shifting from reactive claims to proactive trigger design. Unlike traditional indemnity policies that pay out based on actual loss verification, parametric contracts settle automatically when a predefined index—such as wind speed or earthquake magnitude—crosses a specific threshold. This approach fills critical protection gaps left by conventional coverage, particularly for deductibles and excluded perils [[src-serp-1]].

To build a robust strategy, you must align these instruments with your existing financial infrastructure. Start by mapping your exposure to specific physical or market risks that are difficult to insure traditionally. Then, select a provider with transparent index methodologies and reliable data sources. The goal is not to replace all insurance but to create a layered defense that pays out quickly when liquidity is most needed.

Identify risks where traditional insurance falls short. Look for high-deductible scenarios, excluded perils, or situations where claim verification takes too long. Parametric insurance excels here because it removes the need for loss adjustment surveys, providing immediate capital when a trigger event occurs.

Establish clear, measurable indices for your policy. Be aware of "basis risk"—the mismatch between the trigger event and your actual financial loss. For example, if a hurricane passes 50 miles from your facility, a wind-speed trigger might not cover your specific damage. Choose indices that correlate tightly with your asset vulnerability.

Due diligence is critical. Verify that your provider uses authoritative data sources, such as national weather bureaus or seismic networks. Review their claims history and financial stability to ensure they can meet obligations during widespread catastrophe events. Brokers can help navigate this landscape by comparing multiple underwriters [[src-serp-2]].

Finally, integrate the parametric layer into your treasury management. Since payouts are automatic, treat these contracts as liquid assets that can be drawn upon instantly. This allows your organization to maintain operational continuity without waiting for lengthy insurance claims processes. By combining traditional coverage with targeted parametric solutions, you create a resilient strategy that adapts to modern risk landscapes.

No comments yet. Be the first to share your thoughts!