What parametric insurance actually covers

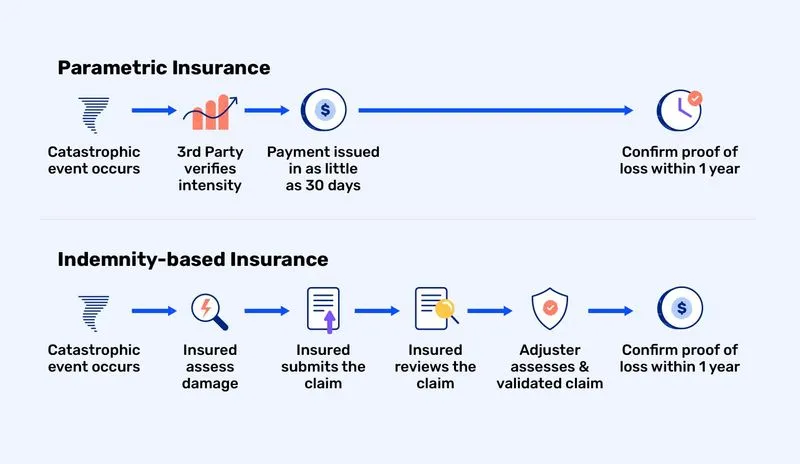

Parametric insurance is a risk transfer mechanism that pays out based on the occurrence of a specific, measurable event rather than an assessment of actual financial loss. Unlike traditional indemnity policies, which require insurers to investigate claims and calculate damages after a disaster, parametric contracts trigger payments when predefined parameters are met. This shift from loss assessment to event triggering creates a system where speed and certainty replace lengthy claims processes.

To understand the difference, consider how a standard property policy works. If a hurricane damages a warehouse, the insurer sends an adjuster to inspect the site, verify the damage, and determine the payout amount. This process can take weeks or months, leaving the insured without liquidity when it is needed most. Parametric insurance removes the adjuster entirely. The contract specifies an index—such as wind speed, earthquake magnitude, or rainfall levels—and the payout is determined solely by whether that index crosses a threshold.

This model relies on objective data sources, often from government agencies or satellite providers, to verify the event. Because the payout is not tied to the insured’s actual financial loss, there is no basis for subrogation or disputes over damage valuation. The Swiss Re Corporate Solutions describes these solutions as covering the probability of a loss-causing event, such as an earthquake, rather than the event’s consequences to a specific asset. This distinction is critical for organizations that need immediate capital to maintain operations after a disaster, regardless of whether their specific physical assets were directly hit.

The coverage is therefore defined by the event’s intensity, not the victim’s suffering. A flood parametric policy might pay out if river levels exceed ten feet for more than 24 hours, even if the insured’s building remained dry. Conversely, if a storm causes severe damage but does not reach the wind-speed threshold, no payment is made. This structure prioritizes financial resilience and rapid response over traditional compensation for physical damage.

How onchain infrastructure automates payouts

Traditional insurance relies on adjusters, paperwork, and weeks of verification to confirm a loss. Parametric insurance removes that middleman by using smart contracts as the payout engine. When a predefined trigger event occurs, the contract executes automatically. This shift from subjective assessment to objective data execution is what makes onchain risk transfer so distinct from legacy models.

The backbone of this system is the oracle network. Oracles act as the bridge between the physical world and the blockchain. They fetch real-world data—such as earthquake magnitude, wind speed, or rainfall levels—and feed it into the smart contract. Because these oracles aggregate data from multiple independent sources, they prevent a single point of failure from manipulating the trigger. This ensures that the payout condition is met based on verified, tamper-resistant data rather than human interpretation.

Once the oracle confirms the trigger has been met, the smart contract releases funds instantly. There is no claims filing process, no waiting for an adjuster’s visit, and no risk of administrative delay. For policyholders, this means liquidity arrives exactly when it is needed most, often within minutes of the event. This immediacy is critical for disaster recovery, allowing businesses and individuals to begin rebuilding or stabilizing operations without cash flow interruptions.

The reliability of this system depends on the quality of the data sources. Official meteorological agencies, seismic monitoring stations, and other primary data providers are typically the feeders for these oracles. By tethering payouts to authoritative, public data, the system eliminates ambiguity. If the wind speed exceeds 120 mph at a specific station, the payout happens. No debate, no denial, just execution.

To understand the market context of these onchain insurance protocols, it helps to look at the assets that power them. Many parametric insurance projects issue governance tokens that reflect the health and adoption of their respective platforms.

Where onchain risk transfer actually works

Parametric insurance in DeFi moves beyond theoretical models to address specific, high-velocity risks that traditional indemnity insurance simply cannot handle. The core advantage is speed: when a smart contract fails or a market moves violently, liquidity providers and users need capital immediately, not after months of claims adjustment. This section outlines the primary scenarios where onchain risk transfer models are deployed.

Protocol exploits and smart contract failures

When a DeFi protocol is hacked, the damage is often immediate and total. Traditional insurance would require forensic accounting to determine exact losses, a process that takes weeks or months. Parametric models trigger payouts based on verified onchain events, such as a specific wallet draining funds or a transaction hash confirming a breach. This allows liquidity pools to remain solvent and users to withdraw their funds before panic selling drives the protocol’s token to zero. The trigger is binary: the exploit happened, or it didn’t. No ambiguity, no delay.

Stablecoin depegs and oracle failures

Stablecoins are the backbone of DeFi liquidity, but they are vulnerable to sudden depegs caused by market crashes or oracle manipulation. A parametric policy can be structured to pay out if a stablecoin’s price drops below a certain threshold (e.g., $0.95) for a set duration. This acts as a circuit breaker, providing immediate capital to liquidity providers or allowing users to hedge their positions. By relying on price oracles rather than individual loss assessments, these models protect the broader ecosystem from cascading failures caused by a single asset’s instability.

Flash loan attacks and MEV extraction

Flash loan attacks and maximum extractable value (MEV) exploits can drain protocols in seconds. While these are often prevented by code, parametric insurance can cover the residual risk when exploits slip through. Payouts are triggered by specific onchain patterns, such as a large, uncollateralized loan being repaid within the same block. This provides a safety net for protocols that rely on complex, untested mechanisms, ensuring that users are compensated even if the code itself is perfect but the economic assumptions are flawed.

Cross-chain bridge failures

Bridges are the most common attack vector in cross-chain DeFi. When a bridge is compromised, assets are stuck or stolen across multiple chains. Parametric insurance can be tied to bridge-specific metrics, such as a sudden drop in total value locked (TVL) on a bridge contract or a confirmed exploit on a specific bridge’s governance contract. This allows for rapid compensation without requiring users to prove their individual losses across different blockchain explorers, which can be technically complex and time-consuming.

Market crashes and liquidation cascades

While not an "accident" in the traditional sense, sudden market crashes can trigger mass liquidations that wipe out user positions. Parametric insurance can be designed to pay out if the price of a major asset (like ETH or BTC) drops below a certain level within a specific time window. This provides a hedge for leveraged positions, allowing traders to recover some of their losses without waiting for the market to stabilize. It transforms extreme market volatility from a catastrophic risk into a manageable, insurable event.

Comparison: Indemnity vs. Parametric

The difference between traditional insurance and onchain parametric models is stark. Traditional indemnity insurance relies on proof of loss, which is slow and expensive. Parametric insurance relies on data triggers, which are fast and transparent. The table below compares the two across key dimensions relevant to DeFi.

| Feature | Traditional Indemnity | Onchain Parametric |

|---|---|---|

| Payout Speed | Months | Minutes/Hours |

| Proof of Loss | Required | None (Trigger-based) |

| Transparency | Low (Private claims) | High (Onchain data) |

| Cost | High (Admin fees) | Lower (Automated) |

Designing a parametric insurance strategy

Building a robust onchain risk transfer strategy requires moving beyond generic coverage models. Unlike traditional indemnity insurance, which relies on assessing individual losses after a disaster, parametric insurance pays out based on a pre-agreed trigger. As the UNDP notes, this approach is designed to build financial resilience by ensuring rapid liquidity when specific conditions are met, such as a hurricane's wind speed or a crypto protocol's hack threshold [src-serp-3].

To design an effective strategy, you must carefully select your triggers and ensure sufficient liquidity. This process involves three critical steps: defining the oracle source, calibrating the trigger parameters, and verifying the liquidity pool depth. Each element must align to prevent basis risk—the danger that the payout does not match your actual loss.

The reliability of your payout depends entirely on the oracle feeding data to the smart contract. Choose oracles with proven track records and decentralized data sources to minimize the risk of manipulation. For onchain risks, this might mean using Chainlink or similar providers that aggregate data from multiple exchanges. For physical risks, ensure the oracle pulls from authoritative bodies like NOAA for weather data or official incident reports. If the data source is compromised, the entire strategy fails.

Basis risk occurs when the trigger event happens, but your specific asset suffers little or no damage, or vice versa. To mitigate this, calibrate your trigger parameters closely to your actual exposure. For example, if you are hedging against a stablecoin depeg, set the trigger slightly below the depeg threshold to ensure coverage. If you are covering crop yield, use local weather station data rather than regional averages. Tighter calibration reduces basis risk but may increase premiums or reduce the frequency of payouts.

A parametric policy is only as good as its ability to pay out immediately. Verify that the liquidity pool backing the smart contract has sufficient depth to cover maximum probable losses. In onchain insurance, this often means checking the total value locked (TVL) in the specific risk pool. If the pool is undercapitalized, payouts may be delayed or pro-rated, defeating the purpose of rapid financial resilience. Regularly monitor pool health and consider diversifying across multiple providers for large exposures.

By following these steps, you create a strategy that is both efficient and reliable. The goal is to minimize the gap between the trigger event and your actual financial impact, ensuring that capital is available when you need it most.

No comments yet. Be the first to share your thoughts!