Why parametric insurance matters for DeFi

Use this section to make the Building a Parametric Insurance Strategy for DeFi Risk Transfer decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

Choosing reliable onchain data

A parametric insurance strategy depends entirely on the accuracy of its data sources. If the oracle feeding your smart contract is compromised, the payout logic fails, leaving policyholders exposed. Unlike traditional insurance, where adjusters assess damage manually, onchain triggers rely on automated, transparent data feeds that must be resistant to manipulation.

Selecting the right oracle requires balancing decentralization with latency. Decentralized networks like Chainlink aggregate data from multiple independent node operators, making it significantly harder for a single attacker to distort the price or event data. For volatile DeFi assets, this redundancy is essential. A centralized feed might be cheaper, but it introduces a single point of failure that sophisticated actors can target during periods of high market stress.

The volatility of underlying assets further complicates data reliability. Rapid price swings can trigger false positives if the oracle does not filter out temporary market noise or flash crashes. Therefore, your design must account for the specific behavior of the asset being insured. For instance, a stablecoin depeg event requires a different data verification threshold than a major cryptocurrency like Ethereum, which naturally experiences wider intraday fluctuations.

Defining binary and threshold triggers

Once data is secured, the next step is defining the trigger conditions that initiate a payout. These conditions act as the contract’s logic core, translating real-world events into onchain actions. The most common structures are binary triggers, which pay out if a condition is met (e.g., "ETH price < $1,500"), and threshold triggers, which pay out based on the magnitude of an event (e.g., "ETH price drops more than 10% in one hour").

Binary triggers are simpler to implement and audit, making them ideal for straightforward coverage. However, they can be vulnerable to "oracle manipulation" attacks if the trigger price is set too close to the current market price. A sophisticated attacker might temporarily depress the oracle price to trigger a payout and then reverse the trade. To mitigate this, many protocols use time-weighted average prices (TWAP) over a specific window, ensuring the trigger reflects sustained market conditions rather than a fleeting anomaly.

Threshold triggers offer more nuanced protection, particularly for assets with high beta or those exposed to specific systemic risks. By setting a deviation threshold, you can exclude minor fluctuations that do not constitute a genuine loss event. This reduces unnecessary payouts and keeps the insurance pool solvent for larger, more significant events. The key is to calibrate these thresholds based on historical volatility data, ensuring they are strict enough to prevent abuse but loose enough to capture genuine risks.

Leverage existing parametric insurance infrastructure

Building a parametric insurance strategy from scratch requires significant engineering overhead, particularly in oracle reliability and smart contract security. Most developers can avoid this friction by integrating with established DeFi protocols that already handle the data feed and payout logic. This approach shifts the focus from infrastructure maintenance to product design and risk modeling.

The current landscape offers several robust options for integrating parametric coverage. These protocols differ primarily in their data sources, coverage flexibility, and liquidity depth. Choosing the right partner depends on whether you need weather-specific triggers, crypto market volatility protection, or broader disaster coverage.

The following comparison highlights the key differences between leading providers to help you select the best fit for your specific risk transfer needs.

| Protocol | Data Source | Coverage Type | Liquidity Model |

|---|---|---|---|

| Nexus Mutual | Oracle networks & community voting | Smart contract exploit & failure | Mutualized capital pool |

| Etherisc | Verified oracle feeds (e.g., weather) | Commodity & weather events | Pool-based with reinsurance |

| Index Coop (DIAX) | Index rebalancing mechanics | Index token de-pegging | Managed vault liquidity |

| Hedgey | On-chain yield data | Impermanent loss protection | Premium-based pool |

Managing basis risk and model gaps

A parametric insurance strategy solves for speed, but it introduces a different kind of exposure: basis risk. This occurs when the trigger fires without a corresponding financial loss for the holder, or worse, when a loss occurs but the parameter threshold remains unmet. In DeFi, where smart contracts execute automatically, this mismatch is not merely an inconvenience—it is a structural flaw that can drain protocol treasuries or leave users underinsured.

Basis risk in DeFi usually stems from data latency or index mismatch. If a protocol uses a central exchange’s price feed as its oracle, a flash crash on a low-liquidity DEX might not trigger a payout, leaving the user exposed to the actual market impact. Conversely, a temporary spike on a major exchange might trigger a payout even if the user’s specific portfolio remained stable. The gap between the "index" and the "actual" loss is the basis.

Model gaps compound this issue. Most parametric models rely on historical data to define "normal" volatility. When a novel attack vector or a black-swan liquidity event occurs, the model may fail to recognize the severity until it is too late. To mitigate this, a robust parametric insurance strategy must diversify data sources, using aggregated oracles rather than single-point feeds, and incorporate circuit breakers that pause payouts during anomalous data patterns.

The National Association of Insurance Commissioners (NAIC) notes that while parametric insurance offers faster payouts, it does not offer broad coverage and may require additional traditional policies to fully cover all exposures. This principle holds true in DeFi: parametric layers should be viewed as a specific risk-transfer tool, not a blanket solution. Users must understand that the trigger is a proxy for loss, not the loss itself, and design their positions accordingly.

The trajectory of onchain coverage

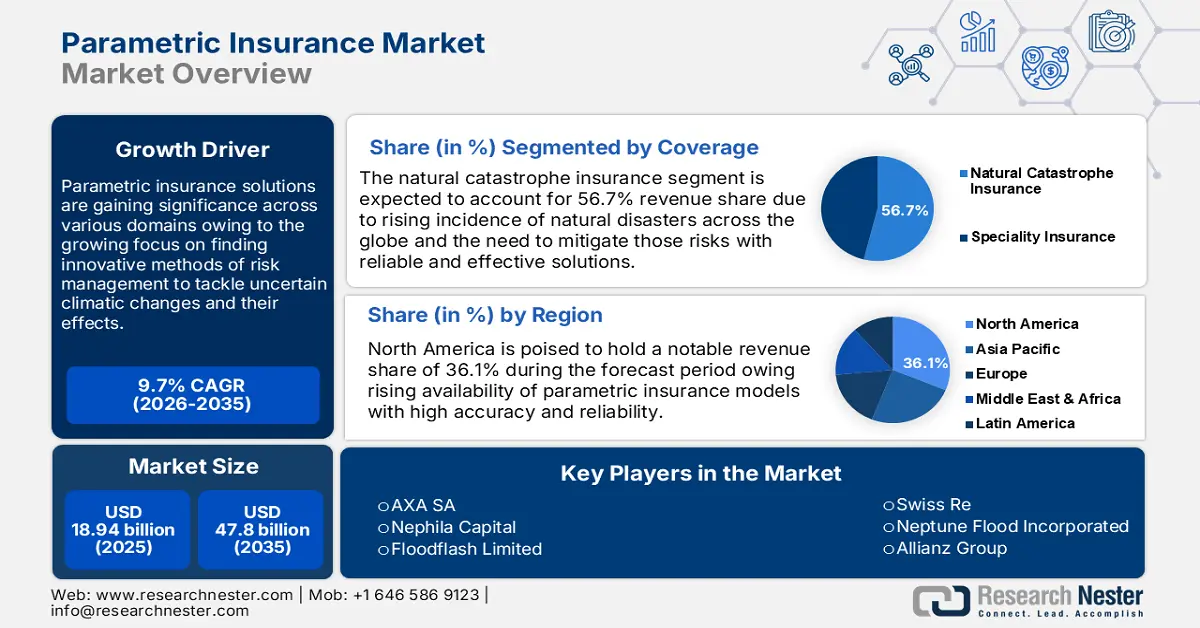

The parametric insurance strategy is shifting from experimental pilots to structured market integration. Market research projects a 7.8% CAGR for the sector through 2035, driven by the need for rapid payouts and climate adaptation. This growth relies on bridging traditional reinsurance capital with decentralized liquidity, creating a more resilient risk transfer layer.

AI-driven risk assessment is central to this evolution. By processing real-time data feeds, AI models reduce the basis risk that often plagues static triggers. This precision allows for broader coverage of complex perils, making parametric products viable for a wider range of DeFi protocols and real-world assets.

Common questions about parametric insurance

What does parametric mean in insurance?

Parametric insurance shifts the focus from assessing actual financial loss to measuring specific, pre-defined triggers. Instead of waiting for a claims adjuster to evaluate damage, the policy pays out automatically when a measurable parameter—such as wind speed, rainfall levels, or earthquake magnitude—reaches a set threshold. This mechanism allows for rapid liquidity, making it a powerful tool for a parametric insurance strategy in DeFi where speed is essential.

What are the downsides of parametric insurance?

The primary limitation is basis risk, which occurs when the trigger event does not perfectly align with your actual financial exposure. For example, a flood sensor might register high water levels at a specific gauge, but your property remains dry, or vice versa. Additionally, these policies typically cover only one specific peril rather than offering broad protection, meaning you may still need conventional coverage for other risks.

What is the future outlook for parametric coverage?

The sector is expanding rapidly, with market projections indicating a 7.8% compound annual growth rate from 2025 to 2035. This growth is driven by the integration of AI-driven risk assessment tools and the increasing need for climate resilience. As data sources become more granular, parametric solutions are becoming more precise, offering better alignment between triggers and real-world impacts for risk managers.

No comments yet. Be the first to share your thoughts!