Parametric insurance limits to account for

Parametric insurance works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative.

After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

The simplest way to use this section is to write down the real constraint first, compare each option against it, and choose the path that still works outside ideal conditions.

Parametric insurance choices that change the plan

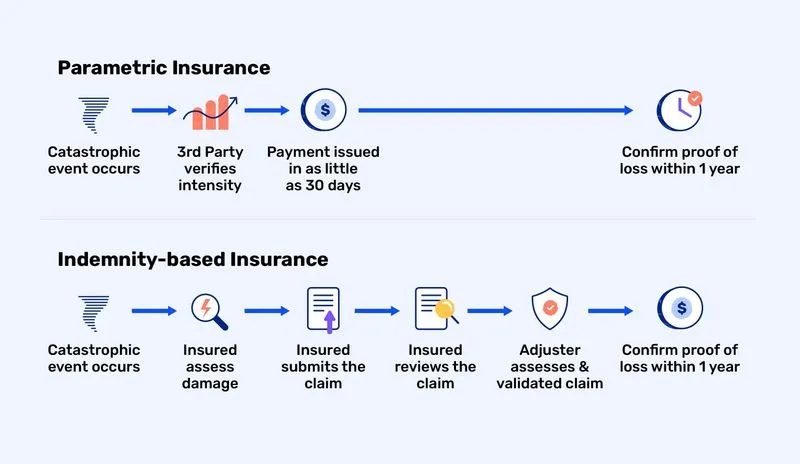

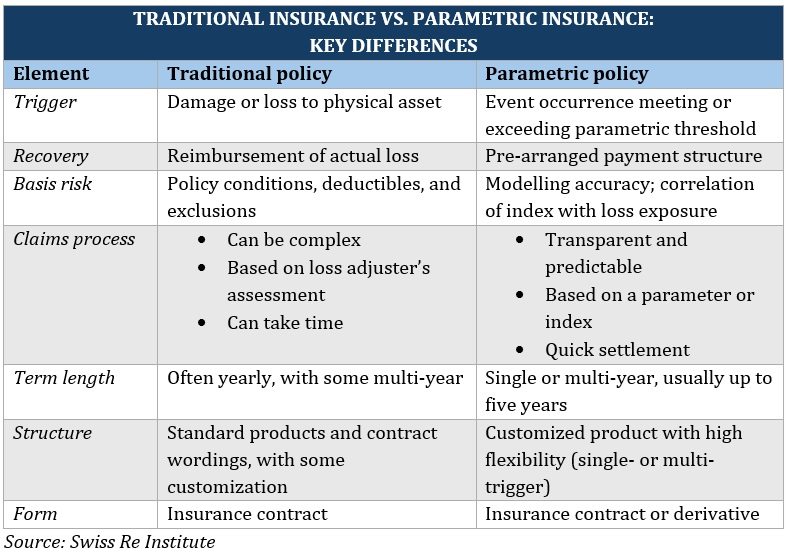

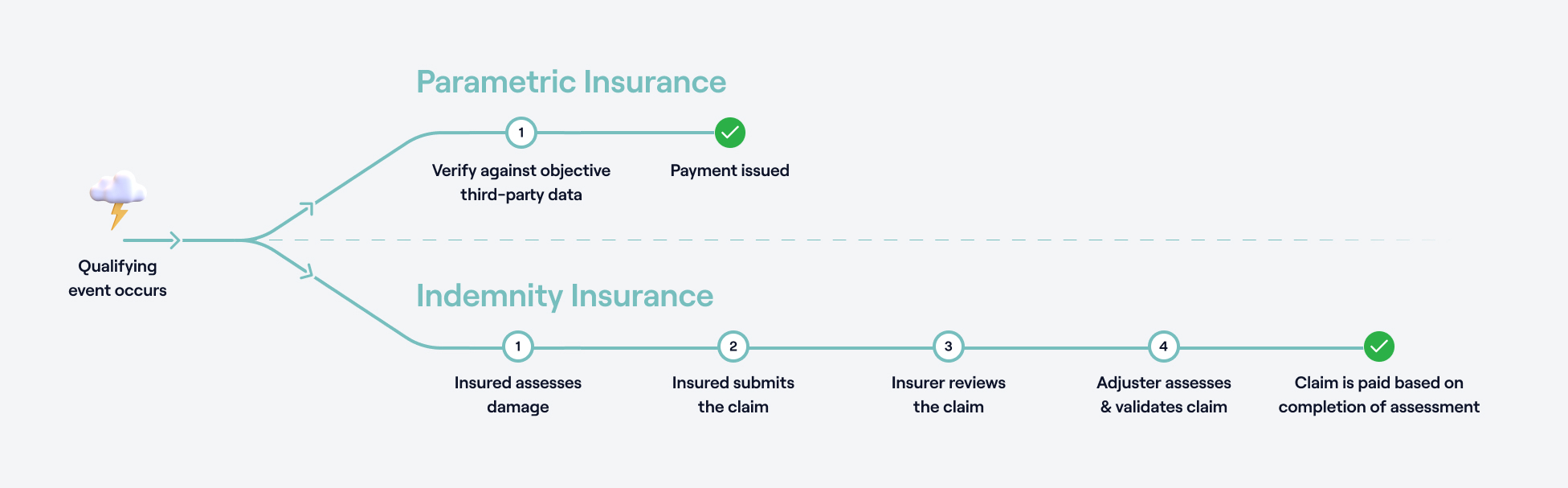

Before integrating parametric insurance into your DeFi risk management stack, you must evaluate the structural tradeoffs. Unlike traditional indemnity policies that reimburse actual verified losses, parametric contracts trigger payouts based on predefined data thresholds. This shift introduces specific advantages and disadvantages that affect capital efficiency, coverage breadth, and operational reliability.

The primary benefit is speed and transparency. Because payouts rely on objective oracles rather than claims adjusters, liquidity is restored instantly after a triggering event. This immediacy is critical for DeFi protocols that face cascading liquidations during market volatility. However, this efficiency comes at the cost of basis risk—the potential mismatch between the payout amount and your actual financial damage. If the oracle data triggers a payout but your specific smart contract did not suffer proportional losses, you may receive capital you do not need, or conversely, insufficient funds to cover your exposure.

In addition, parametric insurance typically covers isolated perils rather than providing comprehensive protection. A policy might cover price crashes or oracle failures but exclude governance attacks or smart contract bugs. This means you often need to layer multiple parametric products to achieve full coverage, increasing complexity and premium costs. The table below breaks down the core factors to compare when selecting a provider.

| Factor | Advantage | Disadvantage |

|---|---|---|

| Payout Speed | Instant settlement via smart contract | No negotiation for partial or exceptional cases |

| Basis Risk | Transparent trigger conditions | Payout may not match actual loss severity |

| Coverage Scope | Fills gaps left by traditional insurance | Usually limited to single peril or event type |

| Data Dependency | Reduces administrative overhead | Relies on oracle accuracy and availability |

| Cost | Lower premiums for specific risks | Higher costs for comprehensive multi-peril coverage |

When evaluating these tradeoffs, consider the volatility of the underlying asset. Rapid market movements can trigger false positives or negatives depending on the oracle's reporting frequency. Always verify that the data source is robust and that the contract logic accounts for edge cases, such as oracle delays during network congestion.

How to choose the next step for onchain parametric insurance

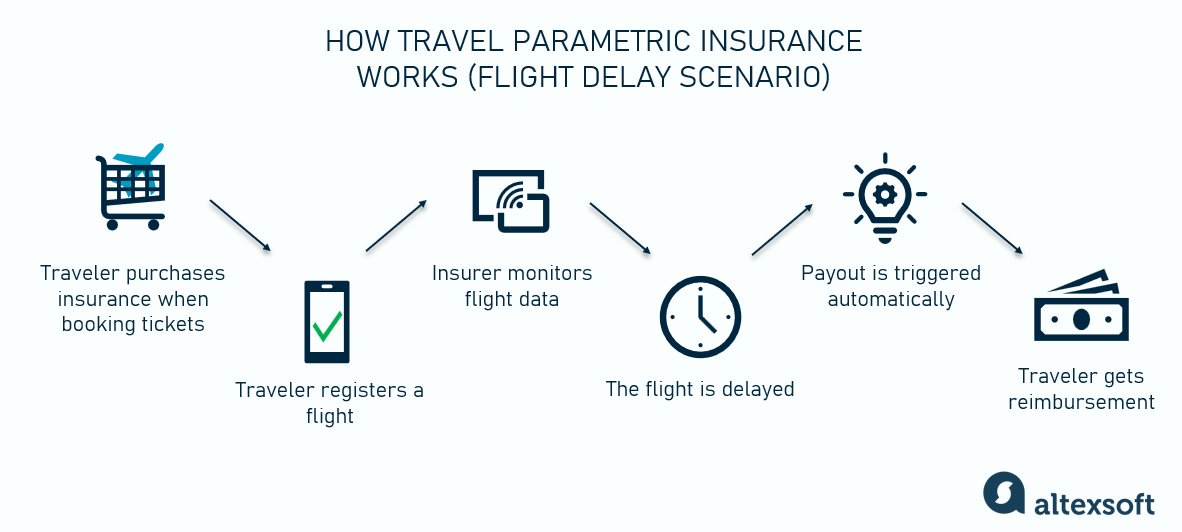

Traditional indemnity insurance often falls short for digital assets and DeFi protocols. It relies on slow claims processing and subjective loss verification, which creates liquidity gaps when speed matters most. Parametric insurance solves this by tying payouts to objective, verifiable data points rather than actual financial damage. This shift enables real-time risk transfer, but it requires a different evaluation framework.

To determine if a parametric solution fits your portfolio or protocol, follow these steps to assess basis risk, data reliability, and smart contract integration.

The core of any parametric policy is the trigger. Unlike traditional insurance that assesses individual loss, parametric policies pay out when a predefined external variable reaches a set threshold. For DeFi, this might be a specific price drop on a major exchange or a confirmed smart contract exploit amount. Clearly defining this metric ensures the policy addresses a single, measurable peril rather than offering vague protection.

Basis risk is the potential mismatch between the trigger outcome and your actual financial loss. A price drop might trigger a payout even if your portfolio remained hedged, resulting in a net loss due to premium costs. Conversely, a significant exploit might not meet the trigger threshold if the data source lags. You must calculate whether the certainty of a partial payout outweighs the risk of paying premiums for non-triggered events.

Since payouts are automated, the integrity of the data oracle is paramount. If the oracle fails, is manipulated, or experiences latency, the payout logic becomes unreliable. Choose providers that use decentralized oracle networks or established, audited data feeds. This step is critical for onchain applications where a single data point failure can result in incorrect fund distribution or missed coverage during a crisis.

Onchain parametric insurance requires seamless integration with your existing DeFi infrastructure. The policy must be programmable, allowing for automatic claim verification and fund disbursement via smart contracts. Evaluate the provider’s technical stack for compatibility with your protocol’s architecture, ensuring that the payout mechanism does not introduce new vulnerabilities or gas inefficiencies into your system.

Parametric premiums are often higher than traditional policies due to the specialized nature of the coverage and the cost of maintaining reliable data infrastructure. However, they eliminate the administrative overhead of claims processing. Calculate the total cost of ownership, including the potential financial impact of uncovered losses under traditional policies, to determine if the parametric premium offers a better risk-adjusted return for your specific exposure.

Common Parametric Insurance Pitfalls

Parametric insurance offers speed, but the onchain infrastructure amplifies specific risks if the contract parameters are poorly defined. Buyers often assume coverage is comprehensive, but these policies are designed for specific triggers, not broad protection. Understanding the structural weaknesses helps avoid costly surprises when a claim is filed.

Basis Risk Discrepancies

The most frequent complaint in parametric insurance is basis risk—the mismatch between the trigger event and your actual financial loss. An onchain oracle might register a 10-meter-per-second wind gust as the payout threshold, but your roof damage might only occur at 15 meters. If the event intensity falls just below the smart contract’s threshold, you receive zero payout despite sustaining real damage. This gap is inherent to the model; you are trading indemnity accuracy for speed.

Oracle Reliability and Latency

Smart contracts rely entirely on external data feeds to execute payouts. If the oracle source experiences latency, corruption, or a temporary outage during the critical window of an event, the automated payout can be delayed or halted. Unlike traditional insurers who adjust for manual delays, onchain systems are rigid. A failure in the data provider’s infrastructure effectively voids the coverage during the very moment you need it most. Always verify the redundancy of the data sources feeding your policy.

Illiquid Secondary Markets

While traditional insurance policies are rarely traded, parametric policies are tokenized assets. Theoretically, this creates liquidity. In practice, secondary markets for these specific risk tokens are often thin. If you need to exit a position early, you may find no buyers, or you may have to sell at a steep discount. The promise of immediate liquidity often dissolves when market conditions tighten, leaving you holding an asset you cannot easily convert back to cash.

Parametric Insurance FAQs

Parametric insurance is a coverage model where payouts are triggered by predefined objective parameters—such as wind speed, earthquake magnitude, or rainfall levels—rather than an assessment of actual financial loss. Once the data oracle confirms the threshold has been breached, the smart contract executes the payment automatically. This mechanism removes the traditional claims adjustment process, providing liquidity to DeFi protocols or businesses within days or hours of an event, rather than months.

What are the downsides of parametric insurance?

The primary limitation is basis risk, which occurs when the payout does not align with your actual economic damage. Because the trigger is binary and based on a specific metric, you might suffer significant losses without meeting the threshold, or receive a payout that exceeds your actual costs. Additionally, parametric policies typically cover only one specific peril. You cannot bundle wildfire, flood, and liability into a single contract; you must layer multiple parametric policies alongside traditional indemnity insurance to create a comprehensive risk management strategy.

Is parametric insurance worth it for DeFi and businesses?

It is worth it if your priority is speed and certainty of liquidity. For DeFi protocols facing smart contract risk or liquidation cascades, waiting for a traditional insurer’s investigation can be fatal. Parametric contracts provide immediate capital to stabilize positions. However, it is not a replacement for core coverage. It works best as a supplemental layer that bridges the gap between the event and the arrival of traditional capital, specifically for risks that are difficult or slow to underwrite conventionally.

What does parametric mean in insurance?

"Parametric" refers to the use of predefined parameters or indices to trigger payouts. Instead of assessing the actual monetary loss after an event (indemnity), the insurance contract specifies a measurable variable—such as wind speed, seismic magnitude, or cryptocurrency price drop. If that variable crosses a set threshold, the payout is automatically executed. This removes subjective loss assessment, making the process faster and more transparent, but it introduces basis risk where the trigger may not perfectly match the actual damage.

No comments yet. Be the first to share your thoughts!