The parametric insurance limits to account for

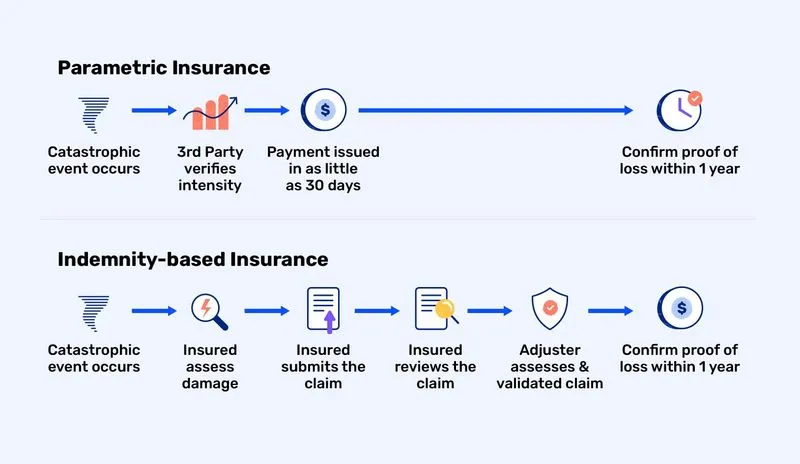

Parametric insurance expands coverage beyond physical assets to fill protection gaps left by indemnity insurance, such as deductibles, excluded perils, and scarce loss data. Unlike traditional policies that require proof of actual damage, parametric contracts trigger payouts based on predefined, objective triggers—like earthquake magnitude or wind speed.

This structural shift creates a specific constraint for DeFi strategies: the risk of basis mismatch. If the onchain oracle data diverges from the real-world event intensity, payouts may not align with actual losses. This disconnect forces builders to prioritize oracle reliability and trigger design over simple coverage breadth.

For resilient DeFi strategies, the focus must shift from maximizing coverage to minimizing basis risk. This means selecting oracles with proven track records and designing triggers that closely correlate with the underlying asset’s exposure, ensuring that the payout mechanism remains robust even when market conditions are volatile.

Parametric insurance choices that change the plan

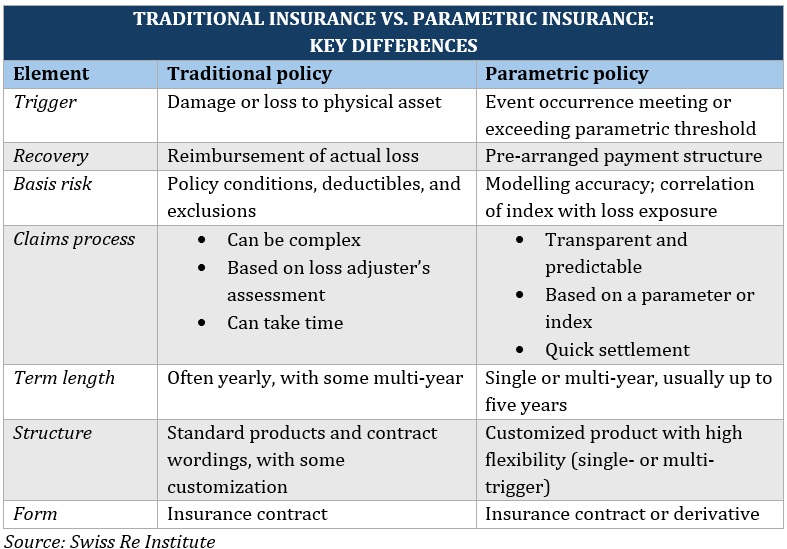

Parametric insurance fills gaps that traditional indemnity policies leave open, such as deductibles or excluded perils [1]. However, this efficiency comes with specific structural tradeoffs that DeFi builders must evaluate before deployment. Unlike traditional claims that assess actual loss, parametric triggers rely on external data oracles, introducing basis risk and model dependency.

When designing resilient strategies, you are balancing speed against precision. The following comparison breaks down the concrete factors that determine whether a parametric product fits your risk profile.

| Factor | Benefit | Risk | Mitigation |

|---|---|---|---|

| Payout Speed | Instant or near-instant settlement | None; automated execution | N/A |

| Basis Risk | Lower administrative overhead | Trigger does not match actual loss | Use multi-index triggers |

| Data Integrity | Transparent and verifiable on-chain | Oracle manipulation or failure | Decentralized oracle networks |

| Complexity | Easy to underwrite and scale | Model error in trigger design | Third-party actuarial validation |

Basis risk remains the most significant tradeoff. If a hurricane causes widespread damage but falls just short of the wind-speed threshold, the policy pays nothing despite real losses. This disconnect is inherent to parametric models but can be mitigated by using correlated multi-index triggers that account for secondary effects like flooding or power outages.

Data integrity is another critical factor. Since payouts depend on external oracles, the security of the data feed is paramount. Relying on a single centralized source creates a single point of failure. Using decentralized oracle networks or aggregating data from multiple reputable sources reduces the risk of manipulation or technical failure.

Finally, consider the complexity of trigger design. While parametric products are easier to underwrite than traditional indemnity policies, designing an accurate trigger requires specialized actuarial expertise. Model error can lead to either excessive payouts or frequent false negatives. Engaging third-party validators helps ensure that the trigger logic aligns with real-world risk scenarios.

Choose the next step

Parametric Insurance works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

Spotting Weak Parametric Options

Not all parametric insurance products are built for the same risk profile. In DeFi, a mismatch between the trigger mechanism and the actual exposure can leave a portfolio underinsured. We identify three common traps that undermine resilience.

Vague Trigger Definitions

A trigger must be binary and objective. If the contract relies on subjective assessments or complex formulas, payouts become disputed. Look for clear thresholds, such as a specific price drop on a major exchange. Avoid products that use "significant loss" or similar ambiguous language. The trigger should be verifiable on-chain or via a single, reputable oracle.

Excessive Basis Risk

Basis risk occurs when the index used for the trigger does not perfectly correlate with your actual holdings. For example, insuring against a general market crash may not protect a concentrated position in a single volatile asset. Always check the correlation between the underlying index and your portfolio. If the correlation is weak, the payout may arrive too late or not at all when you need it most.

Illiquid Payout Structures

Some parametric products delay payouts to verify data integrity, which defeats the purpose of immediate liquidity. In DeFi, speed is critical. Ensure the contract specifies a short, fixed payout window after the trigger is met. Avoid products that require manual claim submission or lengthy verification processes. The goal is automatic, instant compensation to stabilize your position.

Parametric insurance: what to check next

Parametric insurance in DeFi shifts the payout trigger from actual loss verification to predefined onchain data. This structure removes the friction of claims adjusters but introduces new technical risks that buyers must evaluate before deploying capital.

How do onchain oracles affect payout reliability?

Your policy pays only if the oracle reports the threshold has been met. If the oracle is delayed, censored, or manipulated, the payout may not occur when you need it most. Always verify the oracle provider’s reputation and check if the contract includes a fallback mechanism for data outages.

What is basis risk in parametric DeFi products?

Basis risk occurs when the parametric trigger does not perfectly match your actual financial loss. For example, a rainfall trigger might activate, but your specific farm might not suffer crop damage due to microclimates. In DeFi, this often means the index price diverges from your specific pool’s performance, leaving you underinsured despite a trigger event.

Can smart contract bugs void a parametric claim?

Yes. Even if the oracle data meets the trigger, a bug in the payout logic can prevent funds from reaching your wallet. Unlike traditional insurance, there is no claims department to appeal to. Audits are essential, and you should assume that a successful exploit could result in total loss of the coverage pool.

How does liquidity affect my ability to exit?

Parametric insurance pools often have limited liquidity compared to centralized insurers. If you need to exit a position or if a large claim drains the pool, you may face significant slippage or delayed payouts. Check the pool’s depth and historical utilization rates to ensure there is enough capital to cover worst-case scenarios.

No comments yet. Be the first to share your thoughts!