Parametric insurance limits to account for

Parametric Insurance works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

The simplest way to use this section is to write down the real constraint first, compare each option against it, and choose the path that still works outside ideal conditions.

Parametric insurance choices that change the plan

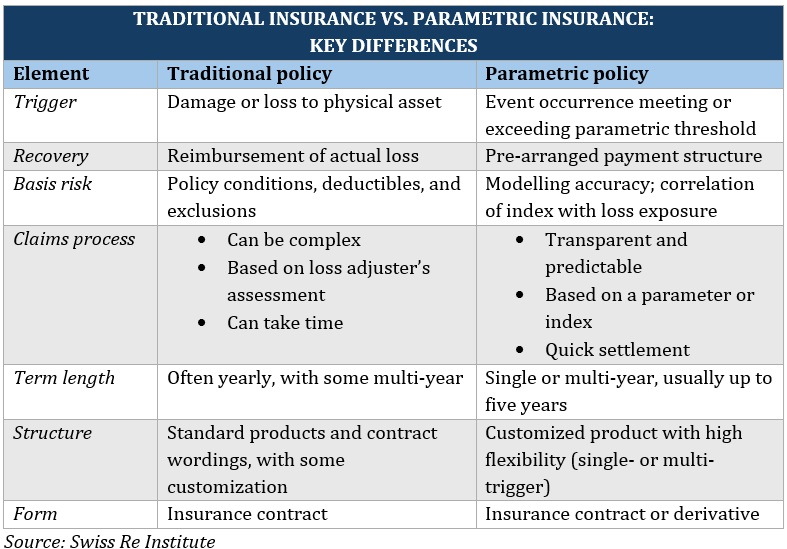

Choosing parametric insurance for DeFi risk transfer means accepting a specific set of structural tradeoffs. Unlike traditional indemnity policies that pay out based on actual proven losses, parametric contracts trigger payments when a predefined external index crosses a threshold. This shift offers speed and transparency but introduces basis risk and potential for misalignment between the index and your actual exposure.

When evaluating these tradeoffs, consider how the index choice impacts your capital efficiency. A mismatch between the oracle data and your specific portfolio performance can leave you underinsured during a real crisis, or overpaying for coverage that doesn't reflect your unique risk profile. The following table breaks down the concrete factors you must weigh before deploying capital.

| Tradeoff Factor | Benefit | Risk / Drawback |

|---|---|---|

| Payout Speed | Automated execution via smart contracts removes administrative delays, ensuring immediate liquidity during market shocks. | No negotiation period; funds are released regardless of whether your specific assets were directly impacted. |

| Basis Risk | Clear, objective triggers eliminate disputes over claim validity, reducing legal and operational overhead. | The index may not perfectly correlate with your portfolio. A market crash might not trigger the specific oracle threshold you selected. |

| Transparency | Smart contract code and oracle data sources are publicly verifiable, allowing for real-time audit of coverage status. | Complex oracle setups can introduce centralization points or latency issues if the data feed is manipulated or delayed. |

| Cost Efficiency | Lower overhead costs due to automated claims processing often result in more competitive premiums for standard perils. | Premiums can spike during high-volatility periods. Custom triggers for niche risks may require expensive, bespoke oracle solutions. |

The choice of oracle provider is critical in mitigating these tradeoffs. Relying on a single data source for your parametric trigger introduces a single point of failure. Diversifying oracle inputs or using decentralized networks can reduce the risk of data manipulation, though it may add complexity to your smart contract architecture.

Choose the next step

Parametric Insurance works best as a clear sequence: define the constraint, compare the realistic options, test the tradeoff, and choose the path with the fewest hidden costs. That order keeps the advice usable instead of decorative. After each step, pause long enough to check whether the recommendation still fits the reader's actual situation. If it depends on perfect timing, unusual access, or a best-case budget, include a simpler fallback.

Watch out for weak parametric options

Not every tokenized risk transfer product deserves capital. The barrier to entry for launching parametric pools is low, which has flooded the market with structures that look sophisticated on paper but fail under actual stress. Before allocating funds, audit the underlying mechanics to separate robust risk transfer from marketing fluff.

Missing oracle diversity

Many protocols rely on a single data source for trigger events. If that oracle experiences latency, a feed error, or a temporary outage, the insurance payout stalls or fails entirely. This single point of failure defeats the purpose of parametric insurance, which is meant to provide immediate liquidity when traditional claims processes break down. Look for protocols that aggregate data from multiple independent oracles to ensure the trigger fires accurately and promptly.

Vague trigger definitions

Some whitepapers use ambiguous language for payout conditions, such as "severe weather" or "market volatility." In a smart contract environment, ambiguity creates legal and technical risk. A trigger must be binary and mathematically precise. If the condition for a payout can be interpreted in two ways, the protocol is likely to face disputes or smart contract exploits. Ensure the contract specifies exact thresholds, time windows, and data sources without room for interpretation.

Inadequate reserve sizing

A common mistake is underestimating the correlation between the parametric trigger and actual systemic losses. If a hurricane triggers a payout, it likely causes widespread damage that correlates with broader market downturns. If the reserve is sized based only on historical frequency without accounting for this correlation, the pool will be insolvent during the very event it is designed to cover. Check the stress-testing methodology used to size the reserve.

Parametric insurance: what to check next

Parametric insurance uses AI-driven oracles to trigger payouts based on predefined data thresholds, such as wind speed or earthquake magnitude. While this removes the need for traditional loss adjusters, it introduces new questions about reliability and coverage gaps.

Does parametric insurance cover all my losses?

No. It only covers the specific parameter defined in the contract. If a hurricane hits your area but the wind speed sensor reads just below the trigger threshold, you receive nothing, even if you suffered damage. This is known as basis risk. Traditional indemnity insurance pays for actual repair costs, whereas parametric insurance pays a fixed amount when data confirms an event occurred. You must accept that the payout may not fully match your actual financial loss.

How fast are payouts compared to traditional insurance?

Payouts are significantly faster. Traditional claims can take weeks or months for adjusters to assess damage. Parametric policies can settle in hours or days once the oracle confirms the data threshold has been breached. For DeFi protocols or businesses needing immediate liquidity after a disaster, this speed is the primary advantage. The money transfers automatically without manual claim filing.

What happens if the oracle data is wrong?

Accuracy depends on the oracle’s source. If the data feed is compromised or delayed, the payout may be incorrect or withheld. This is why using reputable, decentralized oracle networks is critical. Smart contracts often include dispute mechanisms or multiple data sources to validate the trigger. Always verify the oracle’s reputation and redundancy before purchasing coverage.

Is parametric insurance cheaper than traditional policies?

It can be, but not always. Premiums are based on the probability of the trigger event, not historical loss patterns. For high-risk, low-frequency events, parametric policies can be more affordable. However, you are paying for speed and certainty, not for comprehensive loss replacement. Compare the total cost of coverage, including the basis risk gap, to determine if it offers better value for your specific risk profile.

No comments yet. Be the first to share your thoughts!