Defining the parametric insurance strategy

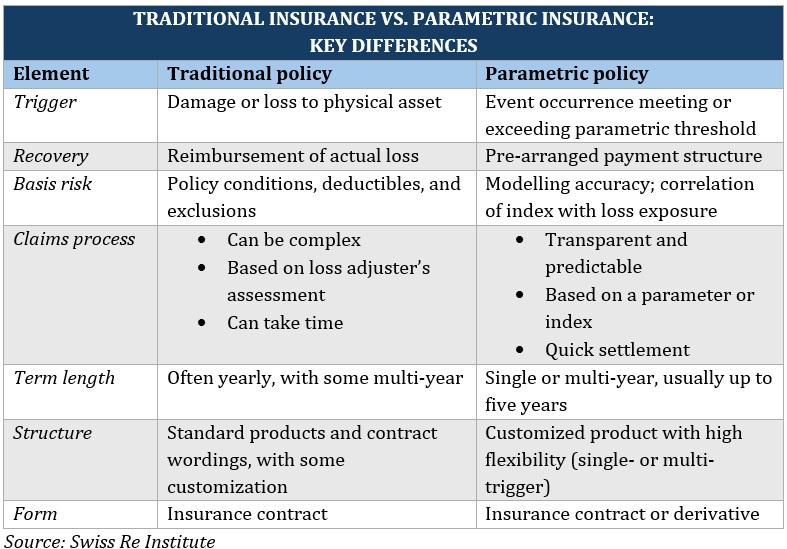

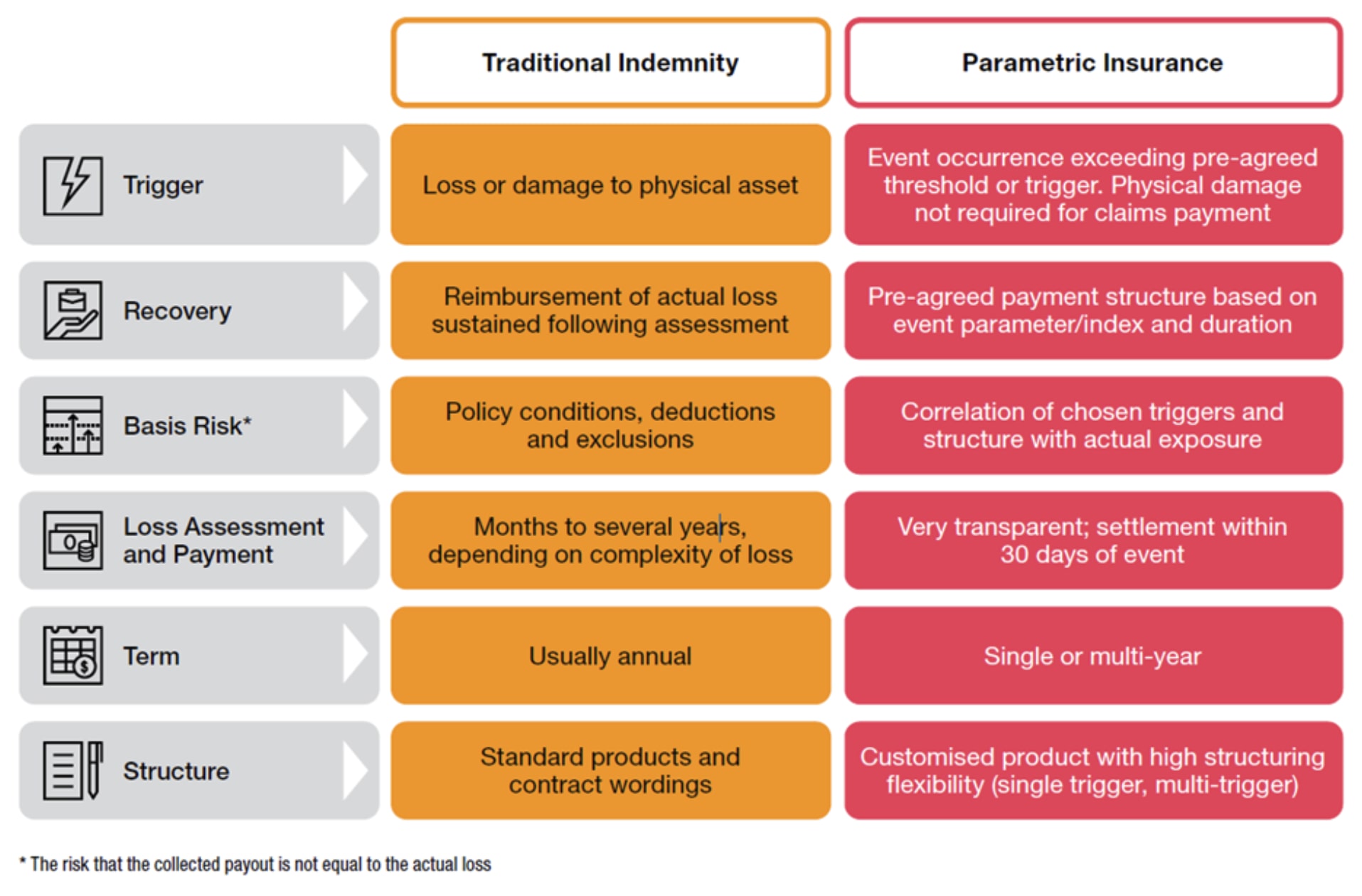

Building a parametric insurance strategy in DeFi requires shifting away from traditional loss assessment toward automated, data-driven triggers. Unlike indemnity models, which rely on lengthy claims processes to verify actual damage, parametric insurance relies on objective, pre-defined parameters to execute payouts. As Swiss Re notes, this approach expands coverage beyond physical assets to fill protection gaps, offering a straightforward and fast-paying risk transfer solution [1].

In the context of decentralized finance, this distinction is critical for managing smart contract risk and market volatility. A parametric strategy does not wait to confirm that a protocol was hacked or that funds were stolen; it triggers when an external oracle reports that a price has dropped below a specific threshold or that a transaction volume anomaly has occurred. This mechanism removes the ambiguity of "how much was lost" and replaces it with the certainty of "when the event happened."

This model transforms insurance from a reactive administrative burden into a proactive liquidity tool. By aligning payouts with verifiable on-chain data, DeFi protocols can maintain solvency and user trust even during rapid market downturns, ensuring that capital is available exactly when the system is most vulnerable.

Onchain infrastructure for risk transfer

Use this section to make the Building a Parametric Insurance Strategy for DeFi decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

Select reliable parametric triggers

Choosing the right trigger is the most critical decision in your parametric insurance strategy. Unlike traditional insurance, which pays out based on verified actual loss, parametric insurance activates when a specific, objective parameter hits a pre-set threshold. This distinction eliminates the need for lengthy claims assessments but introduces a new challenge: basis risk.

Basis risk occurs when the trigger activates, but the payout does not perfectly match your actual financial exposure, or vice versa. As noted in PwC’s analysis of parametric insurance, this mismatch can undermine the utility of the coverage if the trigger is too loosely correlated with the underlying DeFi protocol’s vulnerability. To mitigate this, you must select triggers that are both measurable and directly tied to the specific risk you are hedging.

In DeFi, triggers generally fall into three categories: price-based, time-based, or oracle-dependent. Price triggers are the most common, activating when an asset’s value drops below a certain level. However, they are susceptible to short-term volatility spikes that may not reflect a fundamental failure. Time-based triggers, often used for liquidity locks, are simpler but less sensitive to market conditions. Oracle-dependent triggers rely on external data feeds, offering precision but introducing counterparty risk if the oracle itself is compromised.

The following comparison outlines the trade-offs between these trigger types to help you balance sensitivity against false positives.

| Trigger Type | Reliability | Complexity | Common Use Case |

|---|---|---|---|

| Price-Based | High for market crashes | Low | Lending protocol liquidations |

| Time-Based | Certain if event occurs | Very Low | Vesting schedule delays |

| Oracle-Dependent | Depends on data source | High | Cross-chain bridge failures |

Managing basis risk in coverage

The primary challenge in building a parametric insurance strategy is basis risk—the gap between the trigger and your actual loss. In traditional insurance, payouts are based on proven damage. In parametric models, they are based on an objective index, like wind speed or rainfall data. Basis risk occurs when that index moves, but your portfolio does not suffer the corresponding financial impact, or vice versa.

This disconnect can create a false sense of security. If a parametric trigger fires but your specific DeFi protocol remains functional due to redundancy, you receive a payout for a loss you didn't experience. Conversely, a severe market event might slip past a poorly calibrated trigger, leaving you exposed. Swiss Re and other industry leaders note that basis risk is the most significant barrier to wider adoption because it undermines the very reliability parametric insurance promises to deliver.

To mitigate this, you must treat trigger selection as a dynamic process rather than a static setting. Avoid overly broad indices that don't correlate tightly with your specific asset class. For example, if you are insulating a stablecoin peg against de-pegging events, using a general Bitcoin volatility index as a trigger creates massive basis risk. Instead, look for direct causal links between the index and your exposure.

Regularly backtest your chosen parameters against historical market stress events. This helps you understand how the index behaves during black swan events that might not fit historical averages. The goal is to minimize the basis risk to an acceptable level where the cost of potential false positives or negatives is outweighed by the speed and certainty of the coverage.

Build a parametric insurance strategy with DeFi tools

Building a parametric insurance strategy for DeFi requires selecting protocols that automate coverage through smart contracts. Unlike traditional policies that rely on lengthy claims assessments, these tools use predefined triggers to release funds instantly. This mechanism is essential for high-stakes DeFi users who cannot afford liquidity gaps during market volatility.

You can categorize available tools into on-chain coverage markets and oracle-driven risk protocols. Coverage markets like Nexus Mutual allow users to buy and sell coverage for specific smart contract risks, while oracle-based protocols can trigger payouts based on external data feeds like price crashes or network outages. Understanding the distinction between these two models helps you align your coverage with your specific exposure.

When evaluating protocols, look for those with transparent parameter definitions and robust oracle sources. The reliability of the trigger data is just as important as the smart contract's security. If the oracle data is flawed, the payout logic fails, leaving your strategy exposed.

To deepen your understanding of risk management frameworks that support these strategies, consider exploring established resources on DeFi security and protocol auditing.

As an Amazon Associate, we may earn from qualifying purchases.

Build your parametric insurance strategy checklist

A parametric insurance strategy works best when it acts as a pre-funded circuit breaker rather than a reactive claim. Because payouts rely on objective triggers rather than loss assessments, your preparation time is the only variable that matters. Use this checklist to audit your DeFi positions and ensure your coverage is live before volatility strikes.

Map every position that faces a specific, measurable risk. In DeFi, this usually means tracking impermanent loss in volatile pairs or liquidation risks in leveraged lending protocols. Define exactly what metric would cause you financial harm, such as a specific ETH price drop or a sudden spike in gas fees.

Choose a data source that is transparent and resistant to manipulation. For crypto positions, on-chain price feeds like Chainlink oracles are standard because they aggregate data across multiple exchanges. Avoid triggers based on a single exchange’s price, which can be easily spoofed during low-liquidity events.

Deploy capital into a parametric insurance protocol that covers your specific trigger. Look for platforms that offer transparent smart contract audits and clear payout logic. Ensure the protocol has sufficient liquidity to pay out claims instantly when the trigger is met, without requiring manual approval.

Pre-fund your coverage position with stablecoins or the underlying asset. Regularly review your position to adjust for changing market conditions. Remember that basis risk—the gap between your trigger and your actual loss—can still occur, so maintain a small buffer of unallocated capital for unexpected scenarios.

Implementing this checklist transforms your DeFi risk management from a passive hope into an active, automated strategy. By focusing on objective triggers and reliable data, you remove the ambiguity that often delays traditional insurance payouts, ensuring your capital remains protected when it matters most.

Common questions on parametric triggers

Understanding how a parametric insurance strategy operates requires shifting focus from damage assessment to event verification. Unlike traditional indemnity policies that reimburse actual losses, parametric products pay out based on objective, pre-defined triggers. This distinction is critical for DeFi participants seeking speed and certainty in coverage.

What is a parametric insurance example?

A parametric policy pays out when a specific measurable event occurs, regardless of the actual financial damage. For instance, if rainfall in a defined region drops below a set threshold during a specific season, the policy triggers automatically. In DeFi, this might mean a stablecoin de-peg triggers a payout from a protocol’s treasury, ensuring liquidity without waiting for manual claims processing.

What does parametric mean in insurance?

The term refers to an ex ante agreement to pay upon the occurrence of a triggering event, rather than indemnifying pure loss. As noted by Aon, this creates a straightforward risk transfer solution. The "parameter" is the objective data point—such as wind speed, earthquake magnitude, or blockchain transaction volume—that dictates the payout, eliminating the ambiguity of loss adjustment.

How are payouts determined?

Payouts are dictated by objective measures of the causal event, not the sustained damage. If a parametric policy is tied to a river’s height, the payout is calculated based on how far the water rose above flood stage, not the cost of repairs. This objectivity allows for rapid settlement, a feature that is particularly valuable in fast-moving crypto markets where liquidity gaps can widen instantly.

No comments yet. Be the first to share your thoughts!