Why parametric insurance fits DeFi

Traditional indemnity insurance was built for a world where proving loss takes months. You file a claim, an adjuster inspects the damage, and you wait for a settlement. In DeFi, where a protocol can be drained or a bridge compromised in seconds, that timeline is fatal. By the time the paperwork clears, the assets are gone, and the community has moved on. This structural lag makes traditional coverage ineffective for high-stakes digital assets.

Parametric insurance offers a different mechanism. Instead of assessing the actual loss, it pays out automatically when a specific, pre-defined trigger occurs. As noted by Swiss Re, this approach expands coverage beyond physical assets to fill protection gaps left by indemnity models, such as excluded perils or scarce adjusters. Aon describes it as a "simple, straightforward and fast-paying risk transfer solution" triggered by objective data. For a crypto treasury manager, this means liquidity is restored instantly upon validation, regardless of the final extent of the damage.

The fit is structural. DeFi operates on code and public ledgers, making it possible to define triggers that are verifiable by anyone. Whether it is a specific price drop, a block height, or a smart contract interaction, the data is already there. You do not need to prove you lost money; you only need to prove the event happened. This removes the ambiguity and administrative overhead that often stalls traditional insurance claims.

This model also allows for broader coverage. Because payouts are not tied to the precise calculation of individual losses, parametric insurance can cover scenarios that traditional insurers often exclude, such as deductibles or certain types of cyberterrorism. It shifts the focus from how much was lost to what happened. For a protocol building a risk management strategy, this clarity is invaluable. It transforms insurance from a reactive administrative task into a proactive, automated component of your treasury stack.

Designing onchain trigger logic

Use this section to make the Building a Parametric Insurance Strategy for DeFi Risk Transfer decision easier to compare in real life, not just on paper. Start with the reader's actual constraint, then separate must-have requirements from details that are merely nice to have. A practical choice should survive normal use, maintenance, timing, and budget. If a recommendation only works in an ideal situation, call that out plainly and give the reader a fallback path.

The simplest way to use this section is to write down the must-have criteria first, then compare each option against those criteria before weighing nice-to-have features.

Integrating coverage with DeFi protocols

Layering a parametric insurance strategy over active DeFi positions transforms speculative exposure into a managed risk portfolio. Instead of relying on traditional indemnity models that require lengthy loss assessments, these smart contracts execute payouts automatically when predefined triggers are met. This structural integration allows liquidity providers and yield farmers to hedge against specific market events, such as sudden volatility spikes or protocol exploits, without withdrawing their capital.

The core advantage lies in the removal of basis risk associated with traditional insurance. In a standard DeFi yield farming scenario, a parametric policy can be triggered by an oracle reporting a specific drop in the underlying asset's price or a deviation in the protocol's total value locked (TVL). This ensures that the payout aligns precisely with the financial impact on the user's position, offering a clean hedge that traditional insurers cannot replicate. As noted by the World Economic Forum, parametric insurance bolsters transparency and resilience by decoupling the payout from the complex assessment of actual losses.

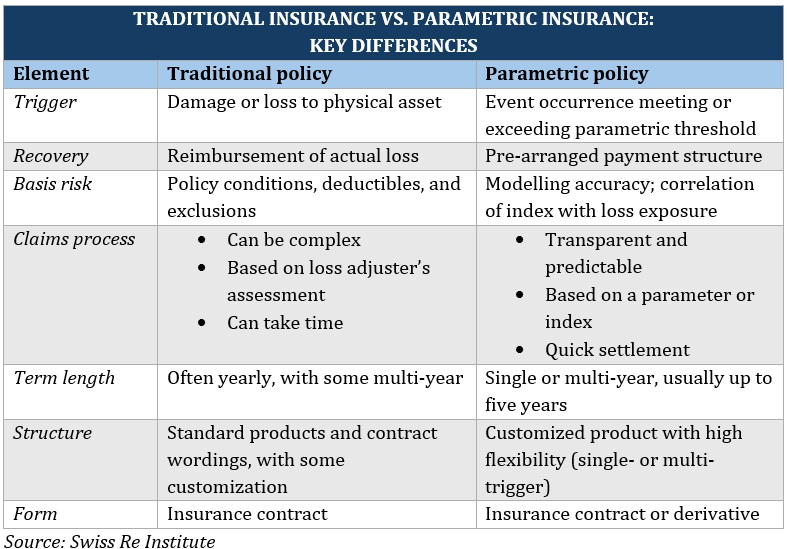

To visualize the difference, consider how parametric coverage compares to traditional insurance in a DeFi context:

| Feature | Traditional Insurance | Parametric DeFi Coverage |

|---|---|---|

| Payout Speed | Weeks to Months | Seconds to Minutes |

| Basis Risk | High (Disputed Valuations) | Low (Oracle-Defined Triggers) |

| Transparency | Opaque Underwriting | Open-Source Smart Contracts |

| Claim Process | Manual Documentation | Automated Execution |

Implementing this strategy requires selecting the right oracle sources and defining clear trigger parameters. Whether protecting against a "rug pull" via TVL drops or hedging against market crashes through price oracles, the goal is to create a seamless safety net that operates in the same time zone as your DeFi activities. This approach ensures that your parametric insurance strategy remains a proactive tool for risk transfer rather than a reactive afterthought.

Managing basis risk and oracle dependency

A parametric insurance strategy relies on the precision of its data inputs. The primary structural risk is basis risk: the gap between the triggering event and the actual financial loss. If your DeFi protocol hedges against a specific volatility spike, but the underlying asset suffers losses from a correlated liquidity crunch that the trigger didn't catch, your strategy fails. Swiss Re notes that parametric insurance expands coverage to fill gaps left by traditional indemnity models, but this expansion only works if the parameter accurately reflects the financial reality of the insured party [src-serp-1].

This disconnect is often exacerbated by oracle dependency. In DeFi, oracles bridge the off-chain world to on-chain execution, but they introduce latency and potential manipulation vectors. A delayed price feed can trigger a payout when no loss has occurred, or worse, fail to trigger when a catastrophic event has already drained a treasury. This isn't just a technical glitch; it's a fundamental flaw in the risk transfer mechanism.

To mitigate these risks, your strategy must prioritize oracle diversity and fallback mechanisms. Relying on a single data source is a single point of failure. Instead, aggregate data from multiple reputable providers to smooth out anomalies and reduce the impact of any single manipulated feed. The goal is to create a robust data layer that makes the parametric trigger as close to the actual financial impact as possible, ensuring that the insurance pays out exactly when it is needed most.

Build your implementation checklist

Turning a theoretical parametric insurance strategy into a live DeFi position requires moving from abstract risk models to executable smart contracts. The workflow below outlines the audit process for identifying eligible positions and selecting appropriate triggers.

Identify which assets are vulnerable to specific market events. Map your positions against potential risks like liquidation cascades, oracle failures, or liquidity pool drains. This audit establishes the baseline exposure that your parametric insurance strategy needs to cover.

Define the exact parameter that will activate the payout. In DeFi, this is often a price threshold on a specific oracle or a time-based block height. As noted by Aon, parametric insurance is triggered by a specific, pre-defined event, ensuring the mechanism is automatic and objective.

Since the payout depends entirely on the trigger data, the oracle’s integrity is paramount. Choose a decentralized oracle network with a proven track record of accuracy and resistance to manipulation. If the oracle is compromised, the parametric insurance strategy fails regardless of how well the contract is coded.

Run simulations using historical data to see if your trigger would have paid out during past market crashes. This backtesting ensures the parametric trigger aligns with your actual risk profile and doesn’t result in false positives or missed payouts during critical moments.

Technical analysis of trigger mechanics

To fully understand the structural advantages of parametric insurance in DeFi, we must examine the underlying mechanics of how triggers are validated and executed. The following chart illustrates the latency and data flow differences between traditional indemnity claims and parametric smart contract executions.

Frequently asked: what to check next

What does parametric mean in insurance?

Parametric insurance, sometimes called index-based insurance, offers policyholders pre-specified financial protection when a particular parameter is met. Unlike traditional policies that indemnify pure loss after an assessment, this approach agrees ex ante to make a payment upon the occurrence of a triggering event. This trigger is often a catastrophic natural event that ordinarily precipitates a loss, ensuring immediate liquidity for DeFi protocols facing structural risks.

What is a parametric insurance example?

Consider a DeFi lending protocol using a parametric strategy to hedge against oracle failures or extreme market volatility. If the price of an underlying asset drops below a specific threshold within a defined time window, the insurance payout is triggered automatically. This mirrors agricultural models where rainfall dropping below a set millimeter amount triggers an automatic payout, removing the need for lengthy claims adjustments and allowing the protocol to rebalance positions instantly.

What is the future of parametric insurance?

The future of parametric insurance extends far beyond weather or natural perils. As noted by industry experts, it has the potential to move into other markets, such as management liability, specialty lines, cyberterrorism, and other risks that don't trigger physical damage but have a significant financial impact. For DeFi, this means broader coverage for smart contract vulnerabilities and governance attacks, integrating parametric triggers directly into protocol safety modules.

No comments yet. Be the first to share your thoughts!