Parametric insurance limits to account for

While onchain infrastructure offers speed and transparency, parametric insurance carries inherent structural constraints that can limit its applicability in DeFi risk transfer. The model relies entirely on predefined triggers and oracle data, which creates specific points of failure that indemnity-based policies do not face.

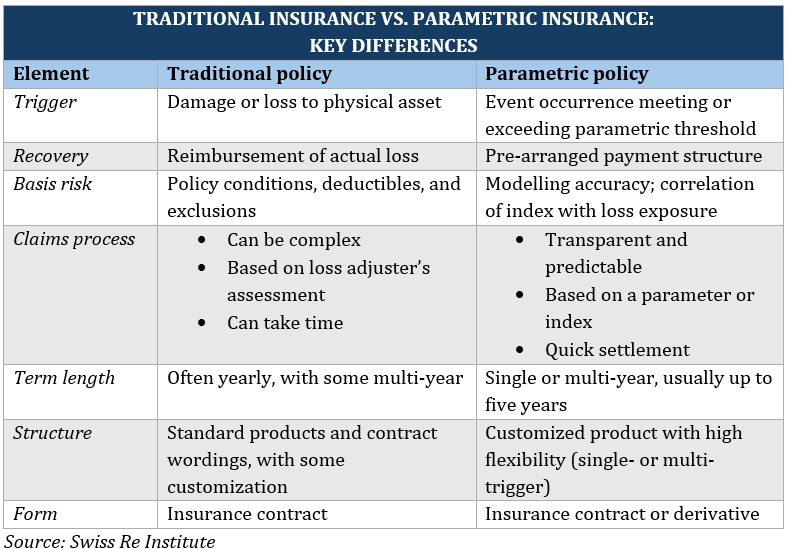

The most significant constraint is basis risk—the potential disconnect between the trigger event and the actual financial loss incurred by the policyholder. In traditional insurance, payouts are based on verified damages. In parametric models, a payout occurs if the oracle data meets the threshold, regardless of whether the user suffered a proportional loss. This can lead to situations where a protocol receives a payout despite minimal impact, or conversely, suffers a major exploit that falls just short of the trigger threshold. This disconnect can distort risk management incentives and lead to moral hazard if participants structure positions to exploit trigger boundaries.

Oracle dependency introduces another layer of vulnerability. Since parametric payouts are automated based on external data feeds, the integrity of the oracle is paramount. If an oracle is manipulated, delayed, or provides inaccurate data, the resulting payout may be incorrect or the contract may fail to execute entirely. This reliance on centralized or semi-centralized data sources contradicts the decentralized ethos of DeFi and introduces a single point of failure. As noted by Swiss Re, parametric insurance expands coverage beyond physical assets, but this expansion is only as reliable as the data infrastructure supporting it [src-serp-1].

Finally, the binary nature of parametric payouts limits flexibility. Unlike traditional insurance, which can offer partial coverage or deductibles tailored to specific risk profiles, parametric contracts typically operate on an all-or-nothing basis. This rigidity can make it difficult to customize coverage for complex DeFi strategies that involve multiple layers of risk. While onchain tools can help mitigate some of these issues through more granular data and smarter contract design, the fundamental constraints remain a critical consideration for any DeFi risk transfer strategy.

Parametric insurance choices that change the plan

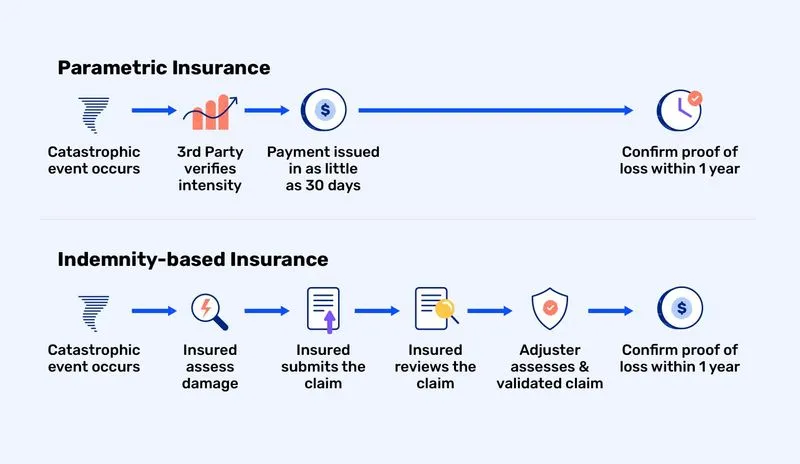

Before deploying capital into onchain risk transfer protocols, you must evaluate the structural differences between parametric models and traditional indemnity insurance. Parametric insurance expands coverage beyond physical assets to fill protection gaps left by indemnity insurance, such as deductibles, excluded perils, and scarce data availability [src-serp-1]. While this offers speed and transparency, it introduces basis risk—the potential disconnect between the trigger event and your actual financial loss.

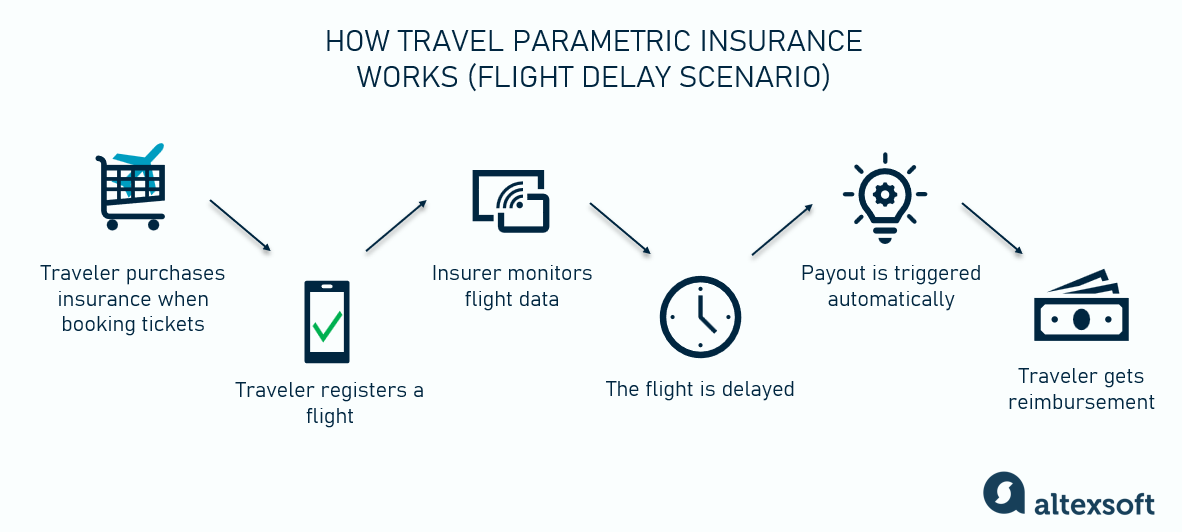

The primary tradeoff lies in precision versus speed. Traditional insurance pays based on verified damage, which is slow but accurate. Parametric insurance pays based on a pre-agreed index, such as a specific earthquake magnitude or a DeFi protocol’s total value locked dropping below a threshold. This eliminates claims processing delays but requires careful calibration of trigger parameters to avoid under-insurance.

To navigate these tradeoffs, compare the following factors when selecting a parametric coverage layer:

| Feature | Traditional Indemnity | Parametric Onchain | Primary Risk |

|---|---|---|---|

| Payout Speed | Weeks to months | Seconds to days | Liquidity crunch |

| Basis Risk | Low | High | Trigger mismatch |

| Underwriting Cost | High (claims adjusters) | Low (smart contracts) | Smart contract exploits |

| Coverage Scope | Physical asset damage | Index events (weather, TVL) | Data oracle failure |

| Transparency | Opaque claims process | Public onchain ledger | Complexity for users |

When evaluating onchain parametric products, the reliability of the data oracle is as critical as the coverage itself. If the oracle feeds incorrect price data or weather metrics, the smart contract will execute the wrong payout. This creates a unique class of counterparty risk where the insurer’s code, rather than their balance sheet, becomes the primary point of failure. Always audit the oracle source and the trigger logic before committing funds.

Choosing the right parametric solution

Selecting a parametric product requires shifting from traditional risk assessment to index-based verification. Unlike indemnity insurance, which pays out based on actual loss severity, parametric coverage triggers automatically when a predefined threshold is breached. This distinction dictates the entire selection process, prioritizing data integrity and basis risk management over asset valuation.

To navigate this landscape effectively, evaluate potential solutions against these four practical criteria:

The foundation of any parametric policy is the underlying data source. Ensure the index is immutable, transparent, and maintained by a reputable provider. For onchain applications, this means verifying the oracle mechanism and the smart contract address. Avoid solutions reliant on third-party reports that can be delayed or disputed, as speed is the primary advantage of parametric triggers.

Basis risk occurs when the index moves but your specific asset does not experience equivalent loss. For example, a hurricane may trigger a payout for a region, but your specific property might remain untouched. Quantify this gap by modeling historical scenarios. If your tolerance for basis risk is low, consider hybrid models that combine parametric triggers with traditional indemnity elements for the most critical exposures.

Triggers must be binary and unambiguous. Whether using wind speed, rainfall levels, or crypto price drops, the condition must be objectively measurable. Avoid complex formulas that require manual interpretation. In DeFi contexts, this means setting clear liquidation thresholds or price deviation limits that are enforceable by code, eliminating the need for claims adjusters or legal disputes.

Determine how the payout is calculated and delivered. Fixed-amount payouts offer simplicity but may not cover escalating losses. Index-linked payouts are more precise but require robust financial modeling. For onchain solutions, ensure the protocol has sufficient liquidity in the reserve pool to honor payouts immediately upon trigger activation, preventing settlement delays during market stress.

By focusing on these operational details, you can select a parametric framework that aligns with your specific risk profile and technological infrastructure.

Watch out for weak parametric options

Many DeFi projects market "parametric insurance" as a panacea, but the infrastructure often lacks the rigorous data feeds required for reliable payouts. Without trusted oracles, the trigger mechanism becomes a single point of failure rather than a risk transfer tool. You must verify that the underlying index is immutable and resistant to manipulation before deploying capital.

Another common pitfall is the disconnect between the trigger event and actual user loss. A protocol might pay out when Bitcoin drops 10%, but your portfolio suffers from smart contract exploits or liquidity crunches unrelated to price action. Parametric coverage only fills specific gaps; it does not replace comprehensive smart contract audits or general insurance.

Finally, beware of vague policy terms that leave room for interpretation. Unlike traditional indemnity claims, parametric contracts are binary. If the data source is ambiguous or the calculation method is opaque, disputes are inevitable. Stick to protocols with open-source code and publicly verifiable logic to ensure your risk transfer is real, not just marketing.

Parametric insurance: what to check next

Parametric insurance pays out based on measurable triggers—like earthquake magnitude or wind speed—rather than assessed losses. This structure removes the traditional claims adjustment process, offering speed and certainty that traditional indemnity policies often cannot match. Below are the practical objections and tradeoffs you should weigh before deploying onchain coverage.

The core advantage of this model is transparency. Every parameter, trigger, and payout condition is visible on the blockchain before you buy. This eliminates the ambiguity of traditional policy language, allowing you to verify exactly what you are buying. However, this clarity also means you bear the full weight of designing the right trigger, as there is no claims adjuster to interpret "fair" damage.

No comments yet. Be the first to share your thoughts!