Why parametric insurance fits DeFi

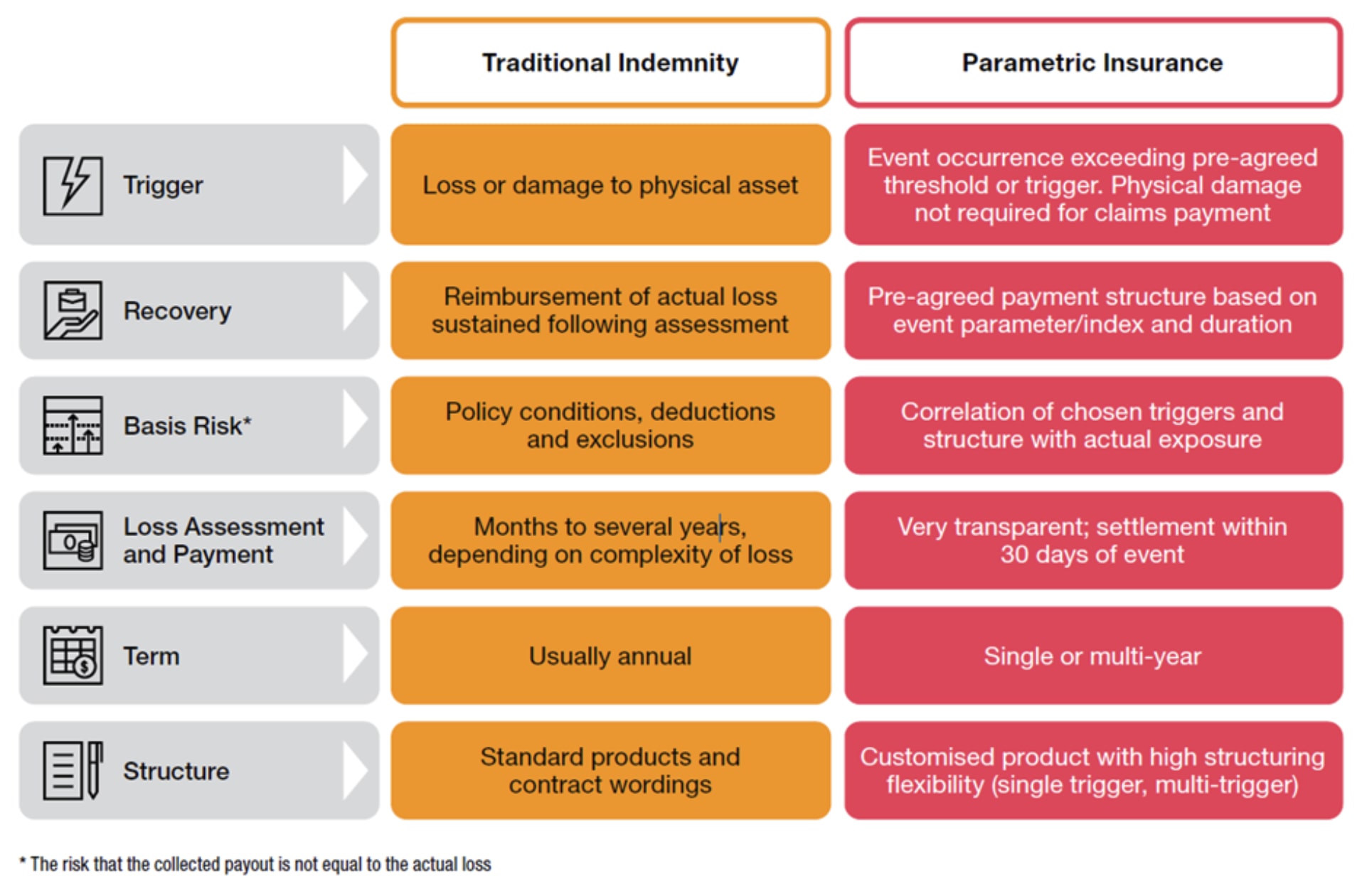

Traditional indemnity insurance relies on proving loss after the fact. You file a claim, submit receipts, wait for an adjuster, and hope for a payout. In DeFi, this model collapses under the weight of opacity and speed. Smart contracts execute in seconds, not months. If a protocol suffers a exploit or a bridge drains, the window to recover assets closes almost immediately. Waiting for a traditional claims process is not just slow; it is functionally useless for onchain risk transfer.

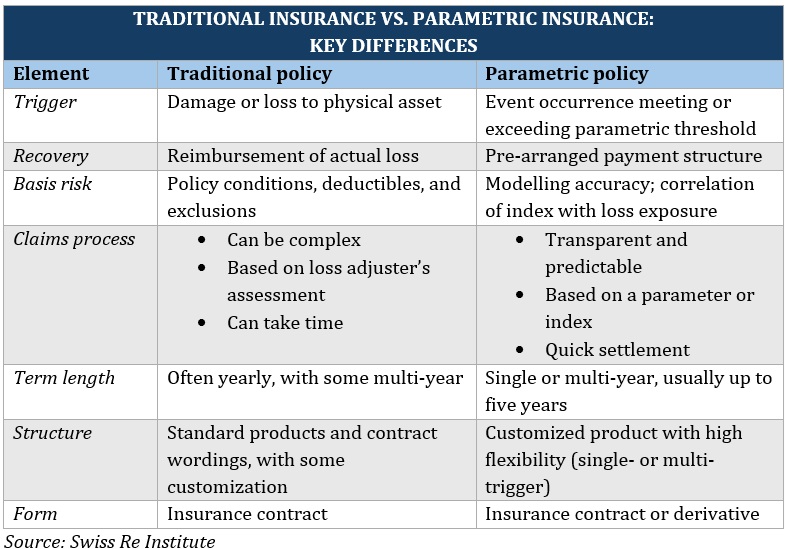

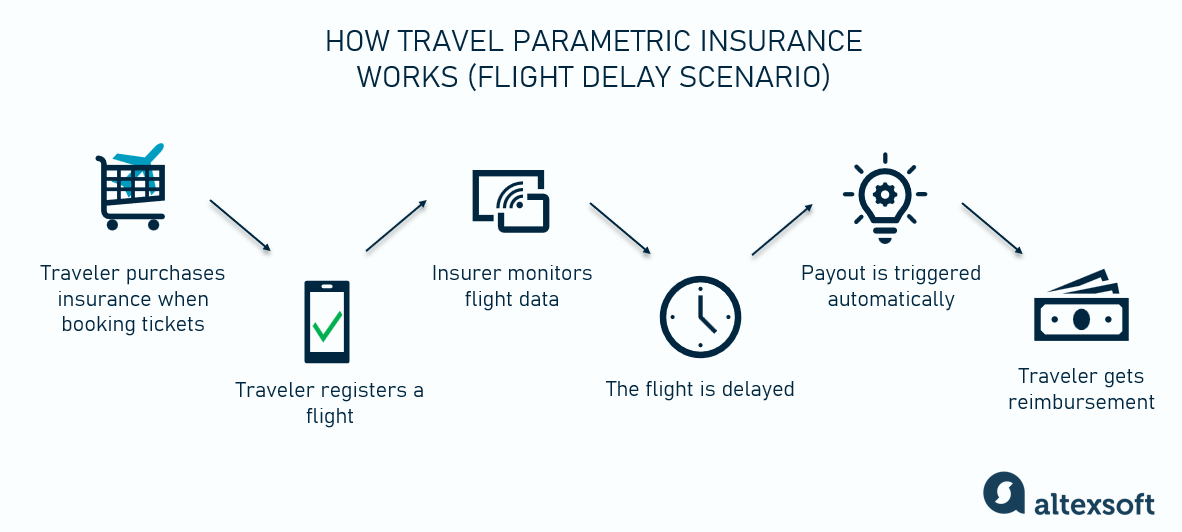

Parametric insurance solves this by removing the need to prove loss. Instead of investigating what happened, the policy pays out when a specific, pre-defined event occurs. As Aon notes, this is a "simple, straightforward and fast-paying risk transfer solution that is triggered by a specific, pre-defined event." The trigger is objective data—a price drop, a transaction hash, or an oracle reading. If the data hits the threshold, the smart contract pays out automatically.

This shift from subjective assessment to objective triggering aligns perfectly with the core values of decentralized finance. It eliminates the latency and opacity that plague traditional insurance. For a parametric insurance strategy to work in DeFi, it must be as programmable and transparent as the protocols it protects. This isn't just about faster payouts; it's about making risk transfer native to the blockchain environment.

Swiss Re highlights that parametric insurance expands coverage beyond physical assets to fill protection gaps left by indemnity models. In DeFi, these gaps are vast. Standard policies don't cover smart contract bugs, oracle failures, or liquidity pool exploits. By defining clear parameters for these digital risks, you create a safety net that actually works for onchain actors. This approach turns insurance from a reactive administrative burden into a proactive, automated component of your risk management stack.

Core infrastructure layers

Building a parametric insurance strategy for DeFi requires a technical stack that replaces traditional underwriting with code and data. Unlike conventional policies that assess individual loss severity, this model relies on pre-defined triggers to execute payouts automatically. The system functions like a vending machine: you insert the correct data inputs, and the policy dispenses the agreed-upon capital without human intervention.

This architecture rests on three interdependent components: oracles for data verification, smart contracts for logic execution, and liquidity pools to ensure payouts are available when triggers fire.

Oracles bridge the gap between on-chain smart contracts and off-chain reality. In a parametric insurance strategy, the oracle is the single point of truth that verifies whether a trigger event has occurred. For example, if your policy is tied to ETH price drops, the oracle must reliably report the current market price from a trusted source. Without a secure oracle, the contract cannot distinguish between a genuine market crash and a data error, making security paramount.

Smart contracts serve as the policy’s legal framework, encoded directly into the blockchain. They contain the specific parameters that define coverage, such as the trigger threshold, payout amount, and validity period. Once the oracle delivers the data, the contract autonomously evaluates the conditions. If the data meets the criteria, the contract executes the payout immediately, eliminating the delays and administrative costs associated with traditional claims processing.

Liquidity pools provide the capital necessary to settle claims. Users deposit assets into these pools, often in exchange for yield or governance tokens, effectively acting as the insurers. When a trigger event occurs, the smart contract draws the required funds from the pool to pay out to policyholders. This mechanism ensures that capital is always available for immediate disbursement, provided the pool has sufficient reserves to cover the aggregate claims.

The interaction between these layers creates a trustless insurance environment. By removing intermediaries, the system reduces friction and ensures that payouts are deterministic based on the data provided. However, this efficiency introduces new risks, particularly regarding oracle manipulation and smart contract vulnerabilities, which must be carefully mitigated in any robust parametric insurance strategy.

Designing effective triggers

The most common failure in a parametric insurance strategy is basis risk. This happens when the trigger fires, but the user hasn't actually suffered a loss, or vice versa. In traditional insurance, an adjuster verifies the damage. In DeFi, the code is the adjuster, and if the code is misaligned with reality, the payout is meaningless.

Consider a trigger based on the price of ETH dropping below $2,000. If the market crashes, the insurance pays out. However, if the protocol was exploited while ETH was stable, the policyholder receives nothing. The trigger measured market volatility, not protocol security. This mismatch is basis risk in its purest form.

To minimize basis risk, you must choose triggers that closely correlate with actual protocol losses. Event-based triggers, such as a verified contract exploit or a specific governance vote, are often more precise than price-based triggers. Price triggers are easier to implement but introduce significant noise. An event-based approach ensures that payouts happen only when the specific risk materializes, not just when the broader market gets nervous.

Comparing Trigger Structures

The table below outlines the trade-offs between the two primary trigger types used in DeFi parametric products.

| Trigger Type | Basis Risk | Oracle Dependency | Implementation Complexity |

|---|---|---|---|

| Price-Based | High (Market vs. Protocol) | Standard (Price Feeds) | Low |

| Event-Based | Low (Direct Correlation) | High (Verified Data) | High |

Price-based triggers rely on standard price oracles, which are widely available and relatively simple to integrate. However, they suffer from high basis risk because a token's price can drop for reasons unrelated to the protocol's health, such as macroeconomic news or a competitor's success. Event-based triggers require more sophisticated oracles that can verify on-chain events, such as a failed transaction or a known exploit signature. While this increases implementation complexity, it dramatically reduces the chance of paying out for non-events.

When designing your strategy, prioritize triggers that are specific to the risk you are insuring. If you are covering smart contract risk, use an event-based trigger tied to verified exploit data. If you are covering liquidity risk, use a price-based trigger tied to the specific pool's reserves. Aligning the trigger with the actual loss mechanism is the only way to make parametric insurance a viable safety net.

Sourcing capital for a parametric insurance strategy

Building a robust parametric insurance strategy requires more than just code; it demands a carefully balanced pool of capital. In the DeFi landscape, this capital serves two competing masters: yield generation and solvency. If you prioritize yield too heavily, your protocol becomes vulnerable during black swan events. If you hoard capital to ensure safety, your returns stagnate, and liquidity dries up. The goal is to find the equilibrium where your parametric insurance strategy remains solvent without becoming inefficient.

Capital efficiency is often measured by how much leverage you can apply to your reserves. In traditional finance, institutions like Swiss Re and Aon highlight that parametric models reduce basis risk—the gap between the index and the actual loss—allowing for tighter capital requirements. In DeFi, this principle translates to deploying idle assets into yield-bearing protocols while keeping a portion liquid for immediate parametric triggers. However, this introduces smart contract risk. If the yield source fails, your solvency buffer evaporates.

To manage this, many protocols use a layered capital structure. The bottom layer consists of stablecoins or low-risk assets to cover frequent, smaller parametric payouts. The upper layer might include volatile assets or leveraged positions to boost overall portfolio returns. This structure ensures that even if the high-yield portion suffers a drawdown, the core insurance promises remain intact.

Understanding the cost of capital is essential. When you allocate funds to a parametric pool, you are essentially selling put options on specific risks. The premium you collect must exceed the expected loss plus the cost of capital. If your parametric insurance strategy relies on stablecoins like USDC or USDT, their live market value provides a baseline for liquidity depth.

Build your parametric insurance strategy

Implementing a parametric insurance strategy in DeFi requires shifting from loss-adjustment logic to trigger-based execution. Unlike traditional policies that assess damage after the fact, parametric contracts pay out automatically when a predefined event occurs, such as a volatility spike or a liquidity pool drain.

Follow this workflow to structure your coverage:

Identify the specific on-chain or off-chain data point that signals danger. For DeFi, this might be a token price dropping below a certain threshold or a governance proposal passing. The trigger must be objective, verifiable, and resistant to manipulation.

Your strategy depends entirely on data integrity. Connect your smart contract to a trusted oracle network like Chainlink or Pyth Network to fetch the trigger data. Ensure the oracle has sufficient decentralization to prevent a single point of failure from compromising your payout conditions.

Encode the payment terms directly into the smart contract. Decide whether the payout is a fixed amount, a percentage of the position, or a sliding scale based on the severity of the trigger. This code becomes your binding agreement, removing the need for claims adjusters.

Parametric contracts require upfront liquidity to ensure payouts are available when triggers are hit. Deposit stablecoins or relevant assets into the designated contract wallet. This capital is locked until the condition is met, providing certainty to the buyer.

Before deploying mainnet funds, run a comprehensive test suite. Simulate various trigger scenarios to ensure the contract executes correctly under stress. Verify that gas costs and oracle delays do not prevent timely payouts during volatile market conditions.

By following these steps, you create a transparent, automated layer of protection. This approach aligns with the broader shift toward parametric disaster insurance, where speed and certainty replace lengthy claims processes.

Common questions on parametric coverage

Understanding how a parametric insurance strategy functions requires looking past traditional indemnity models. Unlike standard policies that assess individual damage, parametric contracts pay out based on objective data triggers, such as wind speed or rainfall levels, rather than actual loss verification.

What does parametric mean in insurance?

In insurance, "parametric" refers to policies where payouts are determined by the intensity of a predefined event rather than the cost of repairs. As noted by Mapfre, the payout is triggered when specific parameters—like seismic magnitude or temperature thresholds—are met, ensuring rapid liquidity without lengthy claims investigations.

What is a parametric insurance example?

A common example involves agricultural protection. If rainfall in a designated region drops below a set threshold, such as 50mm during the monsoon season, the policy automatically triggers a payout. This mechanism, described by ICICI Lombard, allows farmers to receive funds immediately to cover crop losses without proving individual farm damage.

What is the future of parametric insurance?

The market is projected to grow at a 7.8% CAGR from 2025 to 2035, driven by climate adaptation needs and technological advancements. Swiss Re highlights that parametric products are expanding beyond physical assets to fill protection gaps left by traditional indemnity insurance, particularly for excluded perils and deductibles.

No comments yet. Be the first to share your thoughts!