The parametric insurance limits to account for

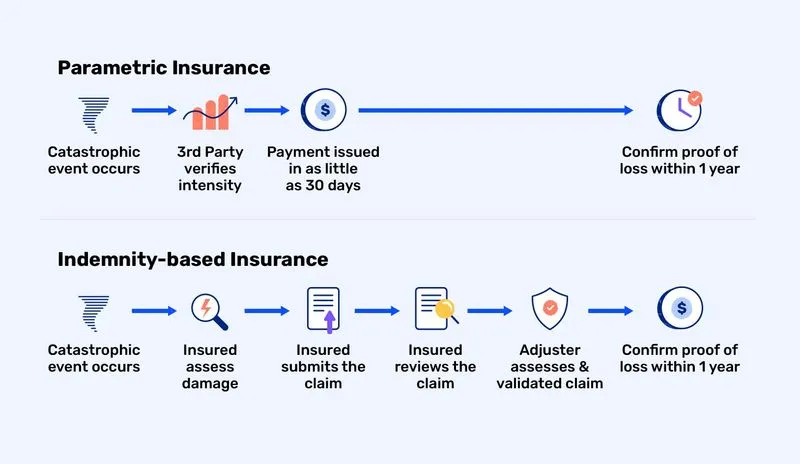

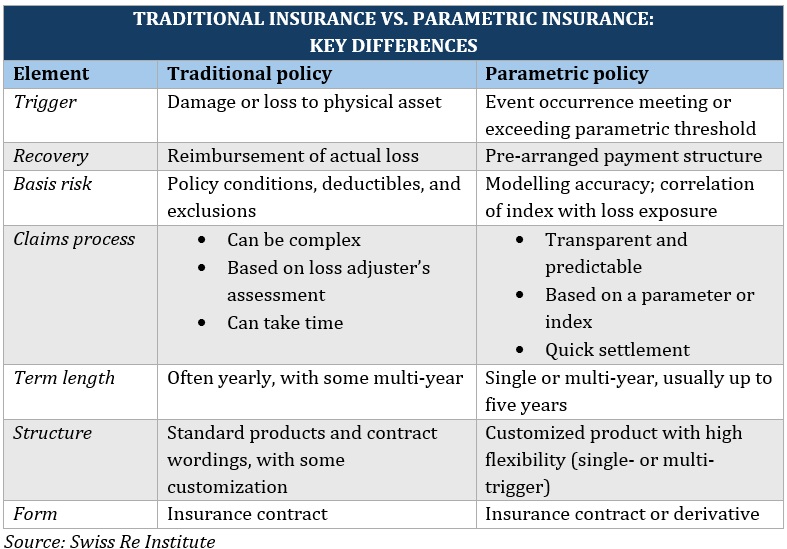

Parametric insurance solves a specific gap in traditional risk transfer: the time and friction of claims. Unlike indemnity policies that require proof of actual loss, parametric contracts trigger payouts when a predefined threshold is breached. This mechanism is particularly useful for covering deductibles, excluded perils, or income loss that standard policies leave exposed.

However, the model introduces a distinct constraint known as basis risk. Basis risk occurs when the parametric trigger activates, but the insured party has not suffered a proportional financial loss, or vice versa. For example, a hurricane might pass near a farm, triggering a rainfall-based payout, while the crops remain largely intact. Conversely, a localized hailstorm could devastate a field without registering enough regional wind data to trigger the contract.

In the context of a 2026 Parametric Insurance guide for DeFi, this constraint is amplified by data granularity. Onchain infrastructure can provide near-instant settlement, but it relies entirely on the accuracy and specificity of the oracle data feeding the smart contract. If the trigger parameter is too broad, the insurance becomes a speculative layer rather than a precise hedge. If it is too narrow, it fails to cover the actual volatility the protocol faces.

Designing resilient strategies requires balancing these tradeoffs. The goal is not to eliminate basis risk entirely, which is often impossible, but to minimize it through precise parameter selection and diversified trigger sources. This ensures the payout aligns closely with the economic reality of the risk being transferred.

Parametric insurance choices that change the plan

Parametric insurance offers speed and certainty by paying out when a predefined threshold is breached, but it requires accepting specific structural risks. Unlike indemnity policies that cover actual loss, these contracts rely on external data triggers. This creates a distinct set of tradeoffs that risk managers must evaluate before deploying capital in DeFi or traditional markets.

The primary advantage is the elimination of lengthy claims assessments. Payouts are automated and immediate, reducing administrative overhead and providing liquidity during crises. However, this efficiency comes with basis risk—the possibility that the trigger does not perfectly align with your actual financial exposure. A hurricane may hit a region, triggering a payout, while your specific asset remains unharmed, or vice versa.

Basis risk is the most critical factor to assess. It arises when the index used for the trigger diverges from your individual loss profile. For example, a crop insurance policy triggered by rainfall in a specific weather station may not reflect the drought conditions on a farm five miles away. In DeFi, a protocol might be hacked while the broader market index remains stable, leaving the parametric hedge ineffective.

Evaluating Basis Risk

Basis risk measures the disconnect between the trigger event and your actual loss. High basis risk means you might pay premiums for coverage that never pays out, or suffer losses without triggering a payout. To mitigate this, choose indices that closely correlate with your specific exposure. Use local data sources rather than broad regional averages where possible.

Assessing Liquidity and Trigger Design

The speed of payout is a major benefit, but it depends on the reliability of the data oracle. If the oracle fails or is manipulated, the contract may not execute. Ensure the trigger mechanism is transparent and based on reputable, tamper-resistant data feeds. Test the contract under stress scenarios to verify that payouts occur as expected when thresholds are breached.

Comparing Parametric Options

Different parametric structures offer varying levels of protection and complexity. Use the table below to compare common approaches based on their trigger mechanisms, basis risk levels, and suitability for different asset types.

| Structure | Trigger Mechanism | Basis Risk | Best Use Case |

|---|---|---|---|

| Index-Based | Broad market index or weather station | High | Portfolio hedging against systemic shocks |

| Location-Specific | GPS data or local sensor | Medium | Physical assets in defined zones |

| Protocol-Specific | Smart contract event or oracle price | Low | DeFi protocol protection |

| Hybrid | Combination of index and actual loss verification | Low | High-value, complex exposures |

Understanding these tradeoffs allows you to build a resilient risk transfer strategy. Parametric insurance is not a one-size-fits-all solution. It requires careful calibration of triggers to match your specific risk profile, ensuring that the speed of payout does not come at the cost of inadequate coverage.

Choosing the Right Parametric Structure

Traditional indemnity insurance pays out based on actual loss, which can take months to assess and often leaves gaps for excluded perils or deductibles. Parametric insurance replaces this subjective assessment with an objective trigger. When a predefined metric—such as wind speed, earthquake magnitude, or temperature—crosses a set threshold, the payout happens automatically. This structure shifts the focus from how much was lost to whether a specific event occurred.

For DeFi risk transfer and onchain infrastructure, this distinction is critical. You are not insuring a physical warehouse; you are insuring a contract’s exposure to a specific onchain or offchain event. The decision framework below outlines four common parametric triggers and how they apply to digital asset risk.

Use this for physical asset exposure linked to digital operations. If your DeFi protocol relies on physical infrastructure (e.g., mining farms or data centers), a weather trigger based on local meteorological data can cover business interruption. The payout is fixed per degree-day or wind speed, removing the need for damage assessments. This is ideal for filling coverage gaps where traditional policies exclude climate-related perils.

Protect against market instability rather than physical loss. A trigger can be set on a specific DEX pool’s liquidity depth or trading volume. If liquidity drops below a certain threshold within a 24-hour window, the protocol receives compensation to cover slippage losses or operational costs. This directly addresses the volatility risk inherent in DeFi strategies without relying on traditional insurance adjusters.

Cover technical failure rather than malicious exploit. While traditional cyber insurance covers hacks, parametric policies can cover failure to perform. If a critical oracle fails to update for more than X minutes, or a bridge’s finality time exceeds a set limit, the payout triggers. This covers the opportunity cost and reputational damage of technical downtime, providing immediate liquidity when the system is stuck.

Hedge against broader market shifts affecting collateral value. If the price of a major asset (like ETH or BTC) drops by a certain percentage within a specific timeframe, or if the Federal Funds Rate changes by a set basis point, the policy pays out. This is less about specific protocol failure and more about protecting the overall portfolio against systemic macroeconomic shocks that traditional insurance cannot touch.

Evaluating the Trade-offs

When selecting a trigger, you must balance precision with basis risk. Basis risk occurs when the trigger does not perfectly align with your actual loss. For example, if your mining farm in Texas shuts down due to grid overload, but your weather trigger is based on temperature, you might not get paid even though you suffered a loss. Always choose triggers that are directly correlated to your specific risk exposure.

| Trigger Type | Best Use Case | Basis Risk Level |

|---|---|---|

| Weather | Physical infrastructure | Medium |

| Onchain Volume | DEX/AMM protocols | Low |

| Contract Execution | Oracle/Relayer services | Low |

| Macro Index | Portfolio hedging | High |

The goal is to find a trigger that is objective, transparent, and hard to manipulate. Onchain data is inherently transparent, making it the preferred source for triggers in DeFi. Offchain data requires reliable oracles, which introduces a second layer of trust. Always audit the data source before finalizing your policy structure.

Spotting Weak Parametric Options

Not all on-chain parametric products deserve capital allocation. While Swiss Re notes that parametric insurance fills protection gaps left by traditional indemnity models, the DeFi space is littered with structurally weak instruments that mimic coverage without providing real resilience [src-serp-1]. Before integrating any protocol into your risk stack, scrutinize the trigger mechanics and settlement logic.

Vague or Manipulatable Triggers

Many projects advertise "weather" or "volatility" triggers without specifying the data source or aggregation method. If a contract relies on a single, unverified oracle for a complex index, the trigger becomes a single point of failure. Robust designs use median aggregation from multiple reputable sources, such as Chainlink or official government APIs, to prevent oracle manipulation.

Liquidity Traps in Payout Pools

A common mistake is assuming that a parametric pool always has sufficient liquidity to pay out during a crisis. When a trigger event occurs, demand often spikes simultaneously. If the pool is under-collateralized or lacks a backstop mechanism from a reinsurance partner, payouts may be delayed or reduced. Always verify the pool's health ratio and the existence of a liquidity buffer before committing funds.

Misaligned Correlation

Some products claim to hedge specific risks but actually correlate positively with the asset they are meant to protect. For example, a DeFi protocol token insurance that pays out only when the protocol's own revenue drops may fail during a market-wide downturn when both the token price and revenue collapse together. Ensure the trigger event is truly orthogonal to your primary exposure to achieve effective risk transfer.

Parametric insurance: what to check next

Parametric insurance in DeFi relies on smart contracts and oracles to automate payouts, removing the need for traditional claims adjustment. This structure offers speed and transparency but introduces specific technical risks that require careful evaluation.

No comments yet. Be the first to share your thoughts!