Defining the parametric insurance strategy

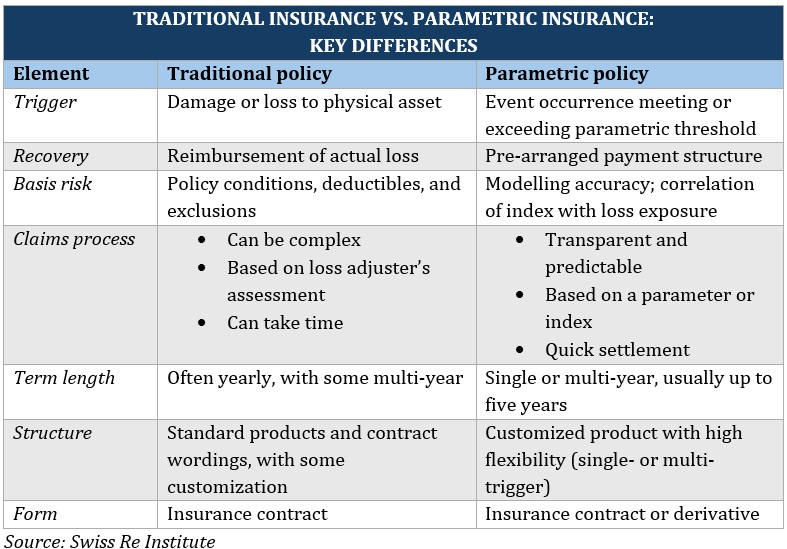

Parametric insurance is a risk transfer mechanism that pays out based on the occurrence of a specific, pre-defined trigger event rather than an assessment of actual financial loss. Unlike traditional indemnity models, which require lengthy claims adjustments to verify damage, parametric insurance relies on objective data points—such as wind speed, seismic magnitude, or cryptocurrency price drops—to determine payouts. This structure shifts the focus from how much was lost to whether a specific threshold was breached.

In the context of DeFi, this distinction is critical. Traditional insurance struggles with smart contract risks because proving the exact value of a hack or exploit can be complex and contested. A parametric insurance strategy, however, can be programmed to automatically execute a payout when an oracle records a price drop below a set level or when a known exploit signature is detected on-chain. As noted by Aon, this offers a "simple, straightforward and fast-paying" solution that eliminates the ambiguity of loss verification.

This approach aligns with the World Economic Forum’s observation that parametric models bolster transparency and resilience by relying on immutable triggers. For DeFi protocols, this means liquidity can be restored almost instantly after a crisis, reducing the "basis risk" of waiting weeks for a traditional underwriter to approve a claim. The strategy essentially treats insurance like a smart contract: if condition X happens, payout Y occurs, with no middleman to negotiate the details.

By decoupling the payout from the actual loss, parametric insurance removes the friction that often makes traditional coverage impractical for fast-moving digital assets. It transforms insurance from a reactive administrative process into a proactive, automated safety net, allowing protocols to maintain operational continuity even during severe market or technical shocks.

How onchain infrastructure enables coverage

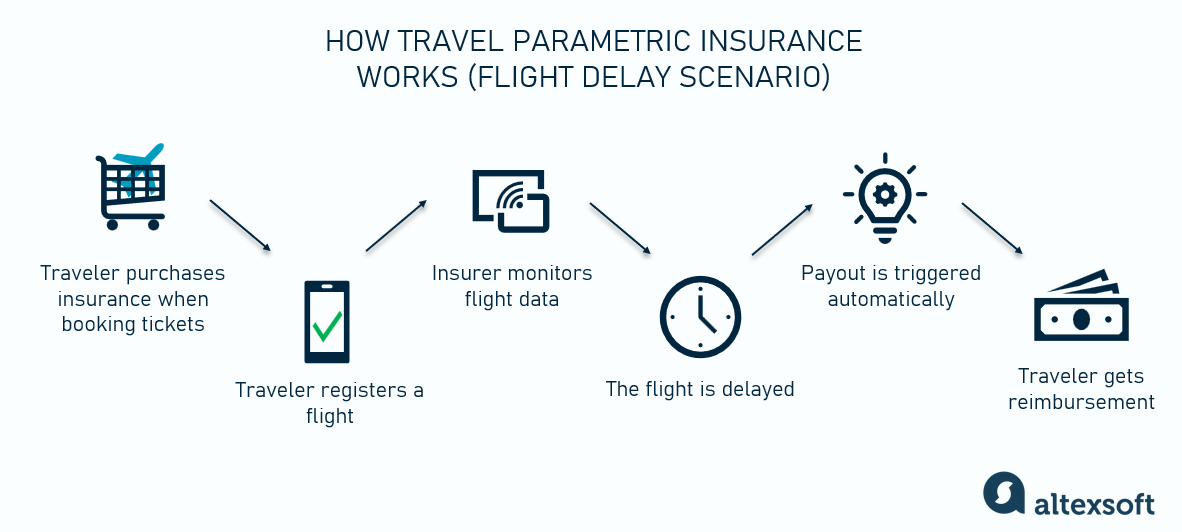

A parametric insurance strategy relies on the same technical stack as decentralized finance: smart contracts and oracles. Unlike traditional policies that require adjusters to assess physical damage, on-chain coverage executes payouts automatically when predefined data thresholds are met. This removes the need for loss verification, turning insurance into a programmable, trustless utility.

The core engine is the oracle. Oracles act as the bridge between off-chain reality and on-chain code. They fetch external data—such as weather patterns, flight delays, or asset prices—and feed it into the smart contract. Without a reliable oracle, the contract cannot verify if the trigger event has occurred. The security of your parametric insurance strategy therefore depends entirely on the integrity and decentralization of the data feed provider.

Once the oracle delivers the data, the smart contract executes the logic. The code checks the incoming value against the agreed-upon parameters. If the condition is met, the payout is triggered instantly. This process eliminates administrative delays and reduces operational costs. The result is a seamless mechanism where coverage is defined by code, not by legal interpretation.

To understand how these triggers function in practice, consider the correlation between asset prices and contract execution. The chart below illustrates a hypothetical scenario where a specific oracle price feed triggers a smart contract event, demonstrating the direct link between market data and automated response.

This infrastructure enables a new class of financial protection. By leveraging official data sources and robust smart contract architecture, you can build a parametric insurance strategy that is transparent, efficient, and resilient to manual interference.

Designing triggers for real-world events

Setting up a robust parametric insurance strategy requires moving beyond vague risk assessments to precise, binary parameters. The core challenge isn't just identifying what to insure, but defining exactly when the payout occurs. This design phase is where you minimize basis risk—the gap between the trigger's activation and your actual financial loss. If the trigger is too sensitive, you face frequent, unnecessary payouts that drain liquidity. If it's too loose, the insurance becomes useless when you need it most.

Choosing the right data source

Your trigger is only as reliable as the data feeding it. In DeFi, this means selecting oracles that are both decentralized and resistant to manipulation. For weather-based parametric products, you might rely on established meteorological data providers. For market volatility triggers, on-chain price feeds from reputable sources like Chainlink are standard. The goal is to use a single, authoritative source of truth that cannot be easily gamed by bad actors.

Aon and other enterprise risk consultants emphasize that data integrity is the foundation of trust in these contracts. If the oracle fails or is manipulated, the entire insurance mechanism collapses. Therefore, your parametric insurance strategy must prioritize oracles with a proven track record of uptime and accuracy over those offering lower fees.

Setting thresholds and time windows

Thresholds define the severity of the event. For example, a flood insurance policy might trigger if water levels exceed 10 feet for more than 24 hours. This time window is critical. A sudden spike that lasts only minutes might cause physical damage but shouldn't necessarily trigger a full payout if your business operations aren't actually halted.

You can compare the efficiency of this automated approach against traditional claims handling:

| Feature | Parametric | Traditional |

|---|---|---|

| Payout Speed | Seconds to minutes | Weeks to months |

| Dispute Potential | Low (data-driven) | High (assessment-driven) |

| Cost Structure | Lower administrative costs | Higher administrative costs |

As the table shows, the primary advantage is speed. Traditional insurance relies on adjusters to assess damage, a process that is slow and expensive. Parametric insurance removes the adjuster entirely. The smart contract checks the data source against the threshold. If the condition is met, the payout executes automatically. This eliminates the need for proof of loss documentation, which is often a bottleneck in DeFi liquidity management.

Managing basis risk

Basis risk remains the biggest hurdle. No trigger perfectly correlates with every individual loss. A hurricane might hit a region, triggering your policy, but miss your specific warehouse. Conversely, a localized fire might cause significant damage without triggering a broader weather index.

To mitigate this, designers often use conservative thresholds or aggregate data from multiple sources. For instance, combining satellite imagery with ground-level sensor data can provide a more nuanced view of the event. This complexity increases development costs but significantly improves the reliability of your parametric insurance strategy. The trade-off is clear: higher accuracy requires more sophisticated data inputs, but it ensures that your liquidity is preserved for genuine risks.

Implementing the strategy in DeFi portfolios

Building a parametric insurance strategy for DeFi risk requires shifting from reactive loss mitigation to proactive, code-enforced protection. Unlike traditional indemnity models that rely on post-event claims adjustment, parametric coverage pays out automatically when a predefined trigger is met. This eliminates administrative friction and ensures liquidity is available exactly when market volatility spikes.

To integrate this into your portfolio, follow these steps to align coverage with your specific asset exposure.

Map your portfolio’s vulnerabilities to specific, measurable parameters. For DeFi, this often means tracking oracle price feeds, liquidation thresholds, or protocol-specific health factors. Define the exact metric—such as ETH dropping below $1,500—that would trigger a payout to cover your potential losses.

The integrity of your policy hinges on the data source. Choose an oracle network with a proven track record for accuracy and resistance to manipulation, such as Chainlink or Pyth. Verify that the oracle’s aggregation method matches the trigger logic defined in the smart contract to prevent false positives or gaming.

Compare the premium cost against the potential payout and the probability of the trigger event. Parametric premiums are often lower than traditional insurance because they exclude moral hazard and fraud, but they may not cover partial losses. Ensure the coverage amount aligns with your actual exposure without leaving significant gaps.

Once the policy is issued, deploy the coverage contract to your wallet. Set up alerts to monitor the trigger parameters and the oracle’s status. Regularly review your coverage limits as your portfolio grows or market conditions shift, adjusting the parameters to maintain adequate protection.

By treating parametric insurance as a dynamic component of your risk management framework, you can reduce exposure to black swan events while maintaining operational efficiency in your DeFi activities.

Common misconceptions about parametric coverage

The biggest hurdle for a parametric insurance strategy is basis risk—the gap between the trigger event and your actual financial loss. Because payouts rely on objective data points like wind speed or rainfall rather than an assessment of your specific damages, you might receive a payout even if your assets were untouched, or conversely, receive nothing despite significant losses if the trigger wasn't met. This disconnect is often misunderstood as a flaw, but it is the very mechanism that eliminates the lengthy claims adjustment process.

Many assume parametric insurance is a direct substitute for traditional indemnity policies. It is not. Traditional insurance covers the cost to repair or replace what was damaged, addressing the 'how much did it cost' question. Parametric insurance addresses the 'when can we recover' question by providing immediate liquidity. As noted by the NAIC, these policies pay set amounts based on event parameters rather than verified losses, making them ideal for cash-flow protection rather than asset replacement.

Think of traditional insurance as a repair shop that fixes your car after a crash, while parametric insurance is like a rapid-response loan that pays out the moment a specific accident report is filed. You use both to ensure the car is fixed and the business keeps running. For DeFi protocols, this means using parametric coverage to bridge the gap during liquidity crises, while relying on traditional audits and smart contract security for the actual technical integrity.

Frequently asked: what to check next

Parametric insurance strategy relies on objective data rather than subjective loss assessment. This approach accelerates capital deployment in DeFi risk management by removing the friction of traditional claims processing. Below are common queries regarding mechanics and definitions.

No comments yet. Be the first to share your thoughts!