Why parametric insurance fits DeFi

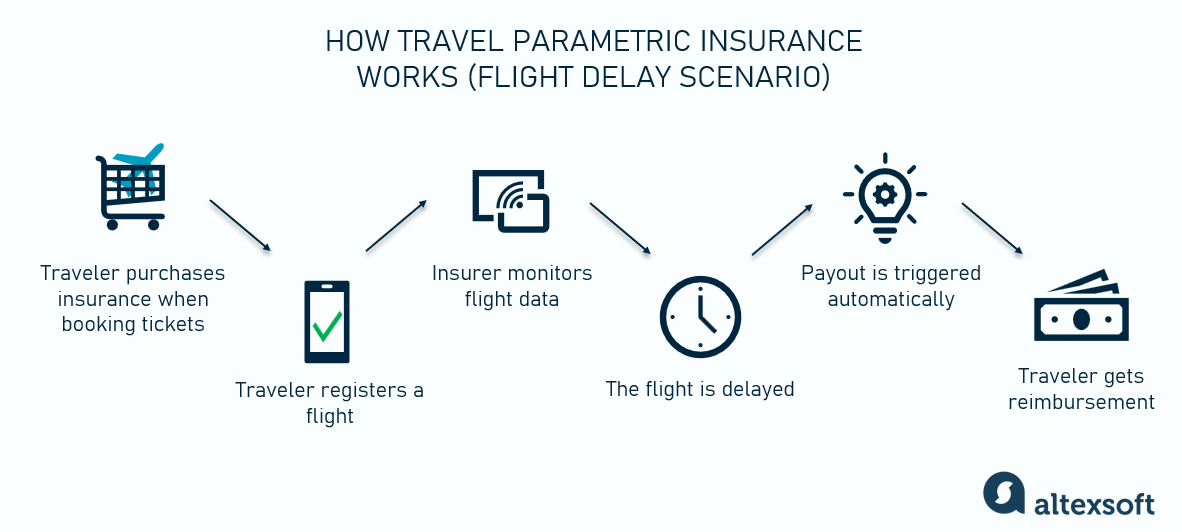

Traditional indemnity insurance relies on a lengthy process: assess damage, determine liability, and negotiate payouts. In the world of Decentralized Finance (DeFi), this timeline is a liability. Smart contract exploits or oracle failures happen in seconds, and the window to mitigate further loss or recover funds is equally narrow. Waiting weeks for a claim settlement offers no protection against the immediate volatility and capital flight inherent in crypto markets.

Parametric insurance solves this by replacing subjective damage assessment with objective, pre-defined triggers. Instead of proving how much money was lost, the policy pays out automatically when a specific condition is met—such as a price drop below a certain threshold or a confirmed blockchain exploit. As noted by Swiss Re, this model expands coverage beyond physical assets, filling protection gaps left by traditional indemnity insurance, particularly where standard deductibles or excluded perils would leave a protocol exposed 1.

Aon describes this approach as a "simple, straightforward and fast-paying risk transfer solution" 2. For a DeFi risk transfer strategy, speed is not just a convenience; it is the core value proposition. By removing the ambiguity of claims adjustment, parametric insurance provides immediate liquidity when it is needed most, allowing protocols to stabilize or users to exit positions before further erosion occurs.

This structure aligns perfectly with the automated nature of DeFi. Just as smart contracts execute code without human intervention, parametric policies execute payouts based on immutable data feeds. This reduces counterparty risk and administrative overhead, creating a more efficient risk transfer mechanism for digital assets.

Designing onchain trigger logic

Building a parametric insurance strategy for DeFi risk transfer requires shifting from subjective loss assessment to objective, data-driven execution. Unlike traditional insurance, which relies on claims adjusters to determine payout eligibility, onchain parametric policies use smart contracts to automate the entire process. The core mechanism is a simple "if/then" condition: if a specific external event occurs, the contract executes a payout automatically.

This automation eliminates administrative friction and reduces the risk of fraud or delayed payments. However, the system’s reliability depends entirely on the accuracy of the data feeding it. Without human intervention to interpret ambiguity, the smart contract must rely on precise, verifiable data points to function correctly.

The Role of Oracles

Smart contracts cannot access real-world data on their own. They are isolated from external information sources by design. To bridge this gap, you must integrate oracles—decentralized networks that fetch and transmit off-chain data to the blockchain. For a parametric insurance strategy, the oracle acts as the single source of truth.

If the oracle provides inaccurate or manipulated data, the smart contract will execute based on false premises. This is known as the "oracle problem." To mitigate this, sophisticated systems often aggregate data from multiple independent sources. For example, a weather-based policy might pull data from several meteorological satellites rather than relying on a single local station. This redundancy ensures that the trigger condition reflects reality, not a glitch or a malicious attack.

Defining the Trigger Conditions

The trigger is the mathematical definition of the insurance event. It must be binary and unambiguous. Vague language like "significant damage" is useless in code; instead, you define specific thresholds, such as "wind speed exceeds 120 mph" or "ETH price drops below $2,500 in the last hour."

These triggers are hardcoded into the smart contract’s logic. When the oracle delivers data that meets or exceeds the threshold, the contract automatically releases the stablecoin or token payout to the policyholder’s wallet. This process happens in seconds, providing immediate liquidity for recovery or hedging. The speed and transparency of this mechanism are what make parametric insurance distinct from traditional financial instruments.

Visualizing the Trigger

To understand how these triggers function in practice, consider a hypothetical volatility spike. The following chart visualizes a scenario where a price drop triggers a pre-defined insurance payout. The contract does not need to "know" why the price dropped; it only needs to verify that the threshold was crossed.

This visualization demonstrates the mechanical link between market events and contract execution. The trigger logic ignores the narrative behind the price movement and focuses solely on the data point. This objectivity is critical for high-stakes financial decisions in DeFi, where trust in the counterparty is replaced by trust in the code.

Liquidity and capital efficiency

Building a resilient parametric insurance strategy requires a shift in how capital is viewed. In traditional models, insurers hold large, static reserves to cover potential catastrophic losses. In DeFi, capital is dynamic. It sits in liquidity pools, earning yield when not deployed, and moves instantly when a trigger fires. This efficiency reduces the cost of capital but introduces new risks around solvency and slippage.

The core mechanic is simple: you need enough locked value to cover the maximum possible payout for a specific trigger event. If your pool lacks liquidity, the smart contract may fail to pay out, or worse, drain the protocol. This is why reserve management isn't just about having money; it's about having accessible money.

Capital allocation models

The table below compares how traditional reinsurance reserves stack up against on-chain liquidity pools in a parametric insurance strategy. Traditional models rely on actuarial tables and regulatory capital requirements, which can take months to adjust. On-chain models adjust in real-time, but require constant monitoring of oracle reliability and pool depth.

| Model | Capital Efficiency | Payout Speed | Primary Risk |

|---|---|---|---|

| Traditional Reinsurance | Low (static reserves) | Slow (weeks/months) | Counterparty default |

| On-Chain Liquidity Pool | High (yield-bearing) | Instant (block-time) | Oracle manipulation |

The oracle problem

Liquidity is only as good as the data that triggers it. If an oracle reports a false positive, the pool drains. If it reports a false negative, the insured is left exposed. This is why the most robust parametric insurance strategies prioritize oracle diversity over pure capital efficiency. A slightly less efficient pool with three independent oracles is safer than a highly efficient one with a single source.

Managing the spread

When a trigger event occurs, the protocol must pay out immediately. This can cause a "flash crash" in the pool's value if the liquidity is thin. To mitigate this, many protocols implement a "spread" or a small fee on payouts during high-volatility events. This fee acts as a buffer, ensuring that the pool remains solvent for subsequent claims. It’s a small trade-off: slightly slower net payouts for guaranteed solvency.

Common Trigger Design Mistakes

Designing the trigger for a parametric insurance strategy is the most critical technical decision in your DeFi risk transfer model. A poorly constructed trigger doesn't just delay payouts; it breaks the core value proposition of parametric insurance: speed and certainty. When the mechanism fails, you are left with the very basis risk you sought to eliminate.

Basis Risk: The Mismatch Problem

Basis risk occurs when the parametric trigger does not align with your actual financial loss. In traditional insurance, an adjuster verifies the damage. In parametric models, you rely entirely on the data source. If your strategy hedges against Ethereum gas price spikes but the trigger monitors Bitcoin volatility, you are exposed. The payout may occur, but it won't cover your specific DeFi position's shortfall, or worse, no payout occurs when you suffer a real loss.

To mitigate this, ensure your underlying asset and the oracle data source are mathematically correlated to your specific risk exposure. A generic "market crash" trigger is rarely precise enough for specialized DeFi protocols. You must map the trigger directly to the smart contract's vulnerability points, such as liquidation thresholds or specific protocol reserve ratios.

Oracle Manipulation and Data Integrity

Your parametric strategy is only as secure as your oracle. If the data source is susceptible to manipulation, your trigger can be gamed. Attackers can exploit low-liquidity markets to temporarily spike a price feed, triggering a false positive payout or, conversely, hiding a real crisis until the funds are drained.

Relying on a single data point or a single oracle provider is a fatal flaw. Implementing a medianizer that aggregates data from multiple reputable sources, or using time-weighted average prices (TWAP) over a sufficient window, neutralizes short-term manipulation attempts. Always audit the oracle's update frequency and fallback mechanisms. If the oracle goes offline or returns stale data, your parametric insurance strategy effectively freezes, leaving you unprotected during the most volatile periods.

Implementing your parametric insurance strategy in 2026

Deploying a parametric insurance strategy requires moving from theoretical design to functional smart contracts. Unlike traditional indemnity claims, which rely on damage assessments, parametric payouts trigger automatically when specific data points are met. This shift demands rigorous technical preparation to ensure liquidity and oracle reliability.

1. Define precise risk parameters

Start by identifying the exact variable that triggers a payout. Whether it is a specific weather threshold, a price drop, or a network outage, the parameter must be objective and verifiable. Swiss Re notes that parametric insurance fills protection gaps left by indemnity insurance, particularly for excluded perils or deductibles. Ensure your parameter aligns with the actual risk exposure you intend to hedge.

2. Select a trusted oracle provider

The oracle is the bridge between real-world data and your smart contract. Choose a provider with a proven track record of data integrity and resistance to manipulation. Since payouts depend entirely on this data feed, any delay or error can invalidate the coverage. Prioritize oracles that offer decentralized consensus mechanisms to minimize single points of failure.

3. Establish liquidity pools

Payouts must be immediate and guaranteed. Set up a dedicated liquidity pool with sufficient reserves to cover worst-case scenarios. This pool acts as the insurance fund, ensuring that users receive their compensation without delay. Consider staking mechanisms or reinsurance partnerships to backstop the pool during extreme events.

4. Audit and test the contract

Before launch, conduct a comprehensive security audit of your smart contract code. Focus on the oracle integration and payout logic, as these are the most vulnerable points. Test the contract in a simulated environment using historical data to verify that triggers and payouts function as intended under various conditions.

5. Launch and monitor performance

Go live with a limited scope to gather real-world data and user feedback. Monitor the oracle data feeds and contract performance closely. Be prepared to adjust parameters or liquidity levels based on initial results. Continuous monitoring ensures the strategy remains effective as market conditions evolve.

Identify the exact variable triggering payout. Ensure it is objective, verifiable, and aligns with the risk exposure. Swiss Re highlights this approach for filling coverage gaps left by traditional indemnity insurance.

Choose an oracle with proven data integrity and decentralized consensus. This component is critical as it directly determines the validity of any payout.

Fund the contract with sufficient reserves to cover worst-case scenarios. Immediate liquidity ensures user trust and operational reliability.

Conduct security audits focusing on oracle integration. Simulate historical data to verify trigger accuracy and payout logic before mainnet deployment.

Deploy with a limited scope. Monitor data feeds and performance closely, adjusting parameters as needed based on real-world results.

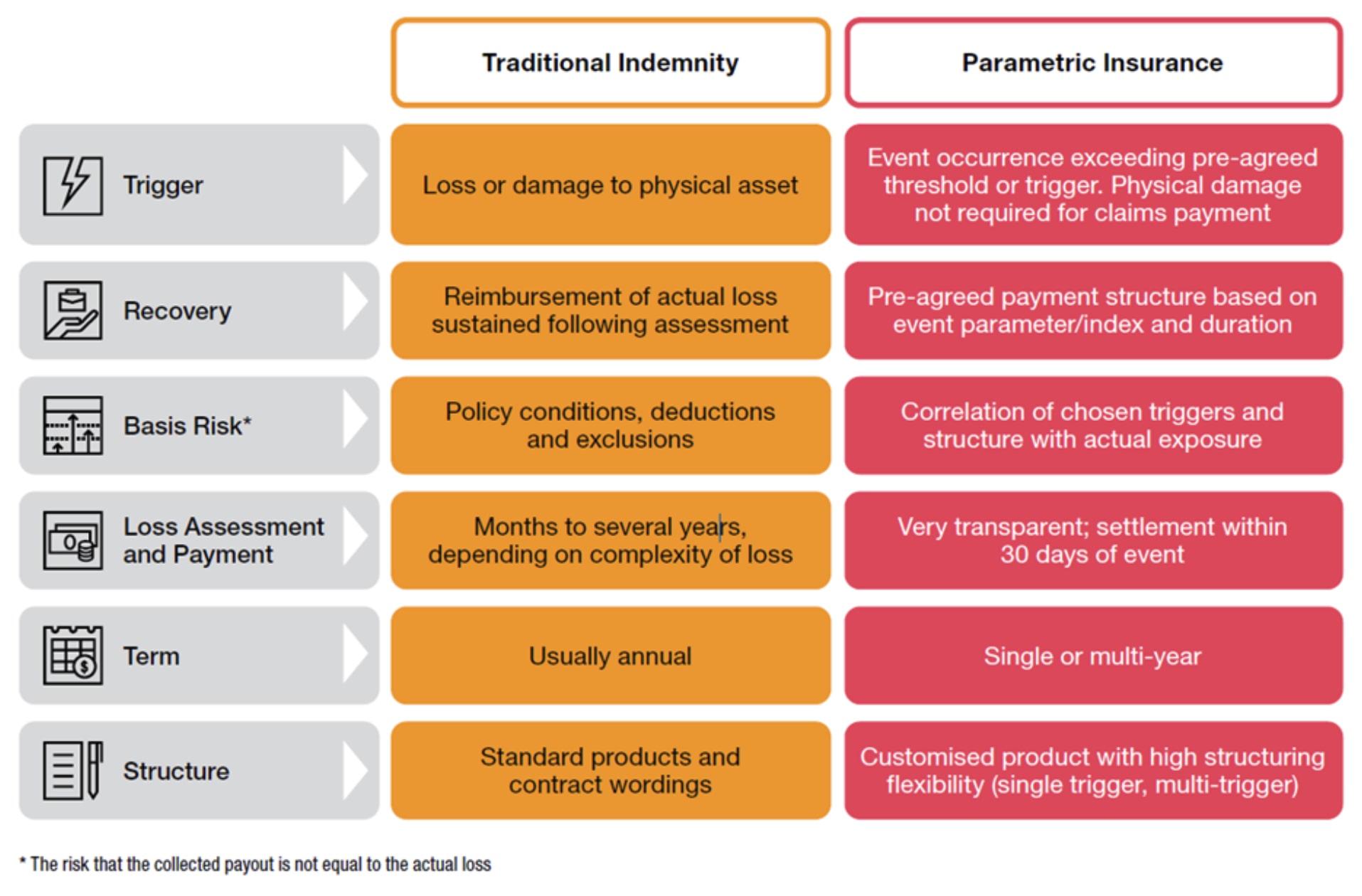

| Aspect | Traditional Indemnity | Parametric Insurance |

|---|---|---|

| Trigger | Damage assessment | Pre-defined data point |

| Payout Speed | Weeks to months | Minutes to hours |

| Transparency | Low (private claims) | High (on-chain data) |

The transition to parametric insurance in 2026 is about precision and speed. By following these steps, you can build a robust risk transfer mechanism that operates independently of traditional insurance bottlenecks.

No comments yet. Be the first to share your thoughts!