Why parametric insurance fits DeFi

Decentralized finance operates on a 24/7 clock where smart contracts execute in seconds, yet traditional indemnity insurance moves at the speed of human bureaucracy. When a protocol suffers a hack or a flash loan attack, the window to contain damage and compensate users closes rapidly. Waiting months for an adjuster to verify loss amounts is not a viable risk management strategy for digital assets that never sleep.

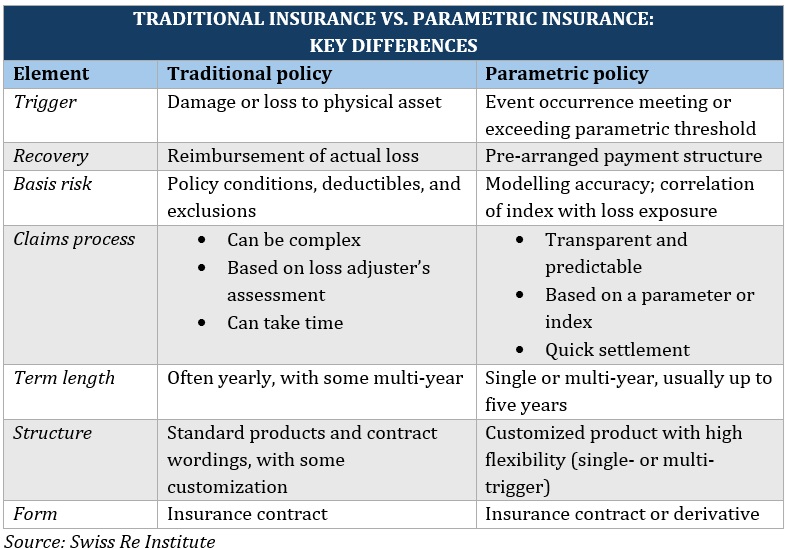

Parametric insurance solves this latency problem by replacing subjective loss assessment with objective, pre-defined triggers. Instead of proving how much money was stolen, the payout is triggered when a specific condition is met—such as a price dropping below a threshold or a known exploit address interacting with the contract. This shift from indemnity to trigger-based payouts ensures that capital is available exactly when the protocol needs it most.

This model aligns perfectly with the infrastructure of DeFi. Reputable carriers like Swiss Re and Aon have increasingly focused on parametric solutions because they remove the ambiguity of post-event investigation. For a protocol builder, this means replacing the uncertainty of a claims process with the certainty of a coded payout, ensuring that risk transfer actually functions as a safety net rather than a bottleneck.

Designing onchain risk triggers

Parametric insurance replaces subjective loss assessment with objective, data-driven payouts. In DeFi, this means the trigger must be an onchain index that is transparent, immutable, and resistant to manipulation. The goal is to create a system where the payout condition is binary: either the data meets the threshold, or it does not.

Selecting the Right Index

The foundation of any parametric policy is the underlying index. For DeFi risk, this is typically a price feed or a volatility metric. You must choose a data source that accurately reflects the asset’s market value without being susceptible to short-term manipulation.

Oracles like Chainlink provide decentralized price feeds that aggregate data from multiple sources, reducing the risk of a single point of failure. However, not all indices are created equal. A simple average price over a block might be vulnerable to flash loan attacks. Instead, consider using time-weighted average prices (TWAP) or volatility indices that smooth out transient market noise.

The chart above illustrates how Bitcoin’s price can fluctuate. A parametric trigger designed to protect against a sudden crash would need to account for these daily swings. If the trigger is too sensitive, it may pay out during normal market corrections, draining the insurance pool. If it is too loose, it fails to protect against genuine systemic risks.

Preventing Manipulation

Once you have selected an index, the next challenge is ensuring it cannot be gamed. Manipulation in DeFi often involves exploiting liquidity gaps or oracle delays. To mitigate this, triggers should rely on data that is difficult to influence at scale.

One effective strategy is to use multiple data sources and require consensus. For example, a trigger might only activate if three independent oracles report a price drop below a certain threshold within a specific time window. This adds a layer of security, making it significantly harder for an attacker to manipulate all sources simultaneously.

Additionally, consider implementing a delay mechanism. Instead of triggering a payout immediately when the threshold is breached, wait for a confirmation period. This allows the market to stabilize and provides time to investigate potential anomalies before funds are disbursed.

Testing and Validation

Before launching a parametric insurance product, rigorous testing is essential. Backtest your triggers against historical market data to see how they would have performed during past crises. This helps you calibrate the thresholds to balance protection with cost-effectiveness.

The widget above shows the current market price of Bitcoin. Use such live data tools to monitor your triggers in real-time during the testing phase. This ensures that your onchain logic aligns with actual market conditions.

By carefully selecting indices, preventing manipulation, and validating through testing, you can design robust onchain risk triggers that provide reliable protection for DeFi users.

Integrating with DeFi protocols

Building a parametric insurance strategy for DeFi risk requires connecting on-chain data to automated smart contracts. The goal is to ensure funds are available immediately when triggers fire, removing the need for manual claims processing. This integration relies on three core components: reliable oracles, precise contract logic, and accessible liquidity pools.

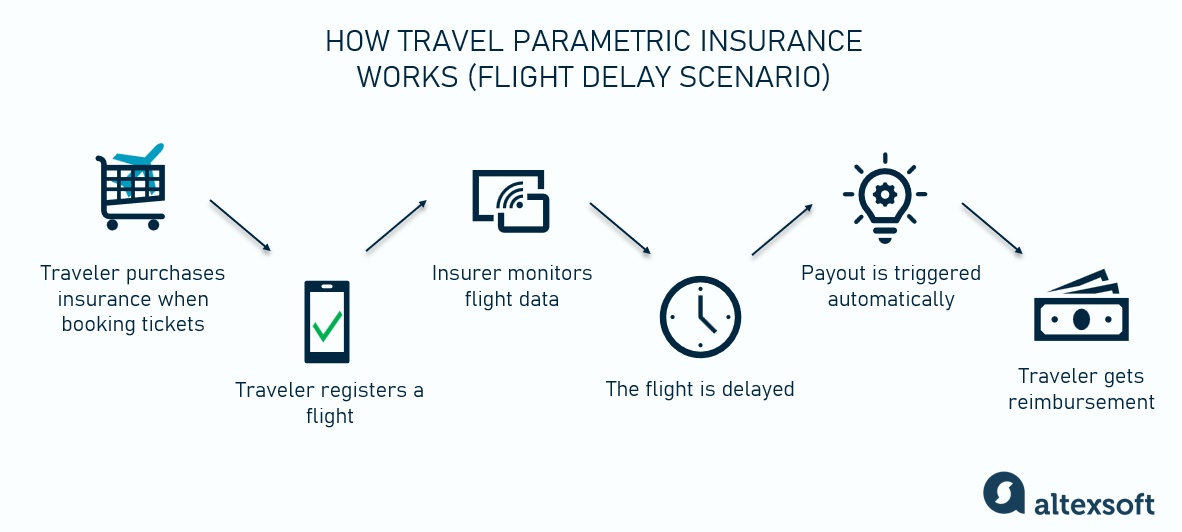

Smart contracts cannot access real-world data on their own. You must integrate decentralized oracle networks like Chainlink to fetch external data points, such as weather metrics or flight delays. These oracles aggregate data from multiple sources to prevent manipulation and ensure the trigger conditions are met accurately. Without a trusted data feed, the insurance contract cannot verify if an event has occurred.

Once data feeds are connected, encode the specific trigger thresholds into the smart contract code. For example, if rainfall exceeds 50mm in a 24-hour period, the contract should automatically flag the event for payout. These conditions must be binary and unambiguous to prevent disputes. The contract logic acts as the sole arbiter, executing payouts based strictly on the data received from the oracles.

Pre-funded liquidity pools ensure that payouts are immediate when triggers are met. Instead of waiting for capital calls or reinsurance recoveries, the smart contract draws directly from these on-chain reserves. This structure provides the rapid, flexible payouts that define parametric insurance, bolstering transparency and financial resilience for policyholders. Adequate funding levels must be maintained to cover potential cluster events.

Before going live, rigorous testing is essential to verify that data feeds, contract logic, and liquidity withdrawals work together seamlessly. Simulate various trigger scenarios to ensure payouts execute correctly under stress. Smart contract audits by reputable firms help identify vulnerabilities that could be exploited. This step protects the integrity of the parametric insurance strategy and builds trust within the DeFi community.

| Oracle Provider | Reliability | Cost | Data Types |

|---|---|---|---|

| Chainlink | High | Moderate | Weather, Finance, Sports |

| API3 | High | Low | Custom Feeds, IoT |

| Pyth Network | High | Low | Financial Markets |

Integrating these elements creates a robust parametric insurance strategy for DeFi risk. By automating the link between real-world events and on-chain settlements, you eliminate delays and reduce administrative overhead. This approach aligns with the broader goal of building climate resilience through transparent, data-driven financial instruments.

Avoiding basis risk in coverage

Basis risk is the gap between the parametric trigger and your actual financial loss. In traditional insurance, an adjuster verifies your damage. In DeFi, the smart contract pays out based on a predefined data point, such as an oracle price drop or a block timestamp. If the trigger fires but your portfolio remains intact—or if you suffer heavy losses without hitting the trigger—you have experienced basis risk. This mismatch is the primary failure mode of parametric strategies.

The most common source of basis risk is data latency or source mismatch. Consider a scenario where you hold ETH on a Layer 2 network like Arbitrum, but your insurance policy uses the Ethereum Mainnet spot price as its trigger. If a flash crash occurs on the L2 due to a liquidity gap, but the Mainnet price remains stable because of deeper liquidity, the oracle may not report a trigger event. Your L2 assets are devalued, yet the insurance payout remains zero. The trigger did not fire, even though you suffered a proportional loss.

To mitigate this, you must align the trigger source with your specific exposure. If you are hedging against a specific bridge failure or L2 congestion, ensure the policy’s oracle reflects the data from that specific ecosystem. Relying on a single, broad market index (like a generic ETH/USD pair) often fails to capture the idiosyncratic risks of niche DeFi positions. For broader market exposure, you can use live data to verify current market conditions and ensure your hedge is active.

Another layer of basis risk comes from the settlement asset. If your policy pays out in stablecoins but your loss is in volatile tokens, the value of the payout may not match the cost of replacing your lost assets. Always check the settlement terms. A payout of $1,000 USDC is only useful if you can buy back the equivalent amount of the lost asset at a reasonable price. If the market is in a freefall, slippage can erode the value of that payout, effectively increasing your basis risk.

Finally, verify the oracle’s update frequency. If your strategy relies on minute-by-minute volatility, but the oracle updates only every hour, you might miss the trigger window. Ensure the oracle’s reporting interval matches your risk tolerance. When the data source, the trigger logic, and your actual exposure are misaligned, the insurance becomes a financial instrument with no protective value. Align them precisely to avoid paying premiums for coverage that never triggers when you need it most.

Checking your parametric setup

Before deploying capital or purchasing coverage, verify that your parametric insurance parameters align with both market conditions and smart contract logic. A mismatch between the trigger event and the actual risk exposure can leave a portfolio underinsured or result in failed payouts.

Use a

to visualize recent volatility spikes. This helps ensure your trigger thresholds (e.g., price drops or time-based deltas) are set within realistic bounds rather than reacting to noise.

Confirm liquidity availability in the payout pool. Even if the trigger fires correctly, insufficient funds in the smart contract will delay or prevent compensation. Cross-reference the protocol’s reserve ratios with the Swiss Re parametric insurance guide to understand standard reserve requirements for similar coverage types.

- Verify trigger accuracy against on-chain data sources.

- Check liquidity depth in the payout contract.

- Confirm gas costs do not exceed potential payout value.

- Test edge cases with historical data simulations.

No comments yet. Be the first to share your thoughts!