Defining onchain parametric coverage

Traditional insurance relies on a slow, often contentious process: an adjuster visits a site, assesses the damage, and determines the payout. Parametric insurance flips this model. Instead of measuring loss, it measures the event itself. If the data hits a specific threshold, the payout happens automatically.

In decentralized finance (DeFi), this mechanism is entirely onchain. The "adjuster" is code, and the "data" comes from oracles—trusted feeds that report real-world events like earthquake magnitude, flight delays, or weather indices. There is no claims form. There is no waiting period for an appraisal. The smart contract checks the oracle data, and if the condition is met, funds are released instantly to the policyholder.

This distinction is critical for high-stakes finance. As Swiss Re notes, parametric solutions cover the probability of a loss-causing event rather than the actual financial impact on an individual. This shift from indemnity to index-based coverage removes human bias and administrative friction. For DeFi users, it means liquidity can be deployed and recovered with algorithmic precision, turning insurance from a reactive cost center into a proactive risk management tool.

The result is a system where trust is not placed in an insurance company’s willingness to pay, but in the integrity of the data source and the execution of the smart contract. This onchain approach is particularly valuable for covering risks that are difficult to underwrite traditionally, such as crop failure or supply chain disruptions, where data is abundant but loss verification is slow.

Market Growth and Institutional Adoption

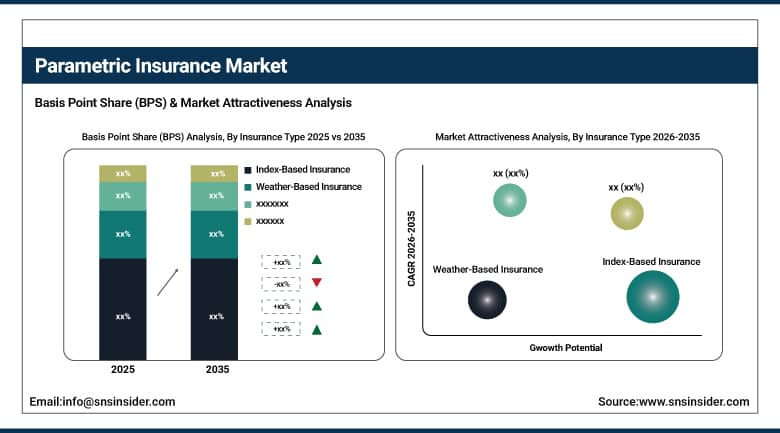

The parametric insurance sector has moved past its experimental phase, transitioning into a core component of institutional risk management. According to GM Insights, the global parametric insurance market size crossed USD 19.4 billion in 2025. This valuation reflects a significant acceleration in adoption, driven by the increasing complexity of global supply chains and the rising frequency of climate-related disruptions that traditional indemnity models struggle to address efficiently.

The trajectory for the next decade remains steep. The market is projected to observe a compound annual growth rate (CAGR) of around 12.2% from 2026 to 2035. This growth is not merely a reflection of higher premiums but of a structural shift in how corporations and governments hedge against volatility. The speed of payout inherent in parametric contracts—triggered by objective data rather than loss assessment—has made them indispensable for liquidity management during crises.

Institutional players are increasingly viewing parametric coverage not as a niche alternative, but as a complementary layer to traditional insurance. This hybrid approach allows organizations to maintain the broad protection of indemnity policies while using parametric triggers for specific, high-frequency, or hard-to-quantify risks. The result is a more resilient financial architecture that can respond to shocks in near real-time, reducing the operational drag associated with prolonged claims processing.

As the market matures, the integration of onchain scaling and AI oracles is further lowering the barriers to entry. These technologies are automating the verification of triggers, reducing basis risk, and enabling granular, micro-level coverage that was previously economically unviable. This technological underpinning is what will sustain the projected growth, transforming parametric insurance from a specialized product into a standard risk management utility.

AI Oracles and Data Integrity

The biggest risk in parametric insurance isn't the payout; it's the trigger. If the data feeding the smart contract is wrong, the contract pays out for nothing—or worse, denies a valid claim. This is the classic "garbage in, garbage out" problem. AI-driven oracles solve this by acting as intelligent validators, ensuring that real-world events match the onchain code before any funds move.

Traditional oracles often rely on single data sources, creating a single point of failure. AI oracles change this by cross-referencing multiple streams. They might compare satellite imagery of flood levels with local weather station readings and historical climate models. If the data points align, the oracle confirms the event. If they diverge, it flags a discrepancy for review. This layer of validation adds a critical shield against manipulation and error.

The International Association of Insurance Supervisors (IAIS) has highlighted parametric insurance as a key tool for closing the global protection gap against natural catastrophes. However, their insights also stress that the credibility of these products depends entirely on the integrity of the underlying data. AI oracles provide that credibility by making the verification process transparent and robust.

This isn't just about speed; it's about trust. When an AI oracle confirms a drought or earthquake, the payout is immediate and indisputable. The system doesn't need adjusters to visit a site or wait for paperwork. It relies on code and data, verified by AI, to deliver financial resilience when it's needed most. This shift transforms insurance from a reactive administrative process into a proactive, automated safety net.

Reducing basis risk in DeFi protocols

Basis risk is the silent killer of parametric insurance. It occurs when the index trigger—such as a specific wind speed or earthquake magnitude—does not perfectly align with the actual financial loss suffered by the policyholder. In traditional indemnity insurance, payouts are based on verified damage assessments, which minimizes this mismatch but introduces massive delays and administrative costs. In the DeFi space, where speed is the primary value proposition, basis risk can erode trust if smart contracts pay out when no real harm occurred, or fail to pay when significant losses were incurred.

The core technical challenge lies in oracle precision. DeFi protocols rely on external data feeds to trigger smart contracts. If an oracle reports a 150 mph hurricane wind speed at a designated weather station, but the actual structural damage to a portfolio of assets occurred at 140 mph due to local microclimates, the contract has failed its fundamental purpose. This is not just a data error; it is a structural flaw in the insurance design. High-stakes finance demands that the trigger mechanism be as robust as the underlying asset it protects.

Mitigating this risk requires moving beyond single-point data sources. Leading protocols are experimenting with multi-source oracle aggregation and spatial interpolation to better approximate actual conditions rather than relying on the nearest weather station. For instance, instead of trusting a single node, an oracle might aggregate data from multiple satellites and ground stations, applying geographic weighting to estimate conditions at the specific location of the insured asset. This approach reduces the likelihood of false positives or negatives, ensuring that payouts are triggered only when the parametric event genuinely correlates with financial impact.

The trade-off is clear: higher precision requires more complex data pipelines and potentially higher oracle fees. However, the cost of basis risk—manifested as capital inefficiency or user attrition—is far greater. By prioritizing data integrity over simplicity, DeFi insurance protocols can bridge the gap between the speed of blockchain and the reliability of traditional risk transfer.

| Feature | Traditional Indemnity | Parametric (DeFi) |

|---|---|---|

| Payout Speed | Weeks to months | Minutes to hours |

| Basis Risk | Low (verified loss) | High (trigger mismatch) |

| Administrative Cost | High (adjusters, legal) | Low (automated code) |

Real-world use cases and liquidity

Parametric insurance is no longer theoretical. It is actively being deployed to protect farmers from climate shocks and DeFi protocols from oracle failures. The mechanism works by tying payouts to objective, verifiable data points rather than traditional loss assessment. This shift from subjective claims to objective triggers is what allows for near-instant liquidity when disaster strikes.

Climate resilience in agriculture

In developing economies, parametric insurance provides a critical safety net for smallholder farmers. Instead of waiting months for adjusters to assess crop damage after a drought or flood, payouts are triggered automatically when satellite data confirms rainfall levels fall below a specific threshold. This speed is vital for farmers who need immediate capital to replant or buy supplies. The World Economic Forum highlights that these AI-driven models are building climate resilience by reducing the time between disaster and financial support from months to days.

DeFi protocol protection

The decentralized finance (DeFi) sector has adopted similar logic to protect against smart contract exploits and oracle manipulation. Protocols use on-chain data to trigger insurance payouts or pause operations when price deviations exceed set limits. This automated response prevents further capital flight during market volatility. By removing human intervention, these systems ensure that liquidity remains available exactly when it is needed most, stabilizing the ecosystem during high-stress events.

Market growth and adoption

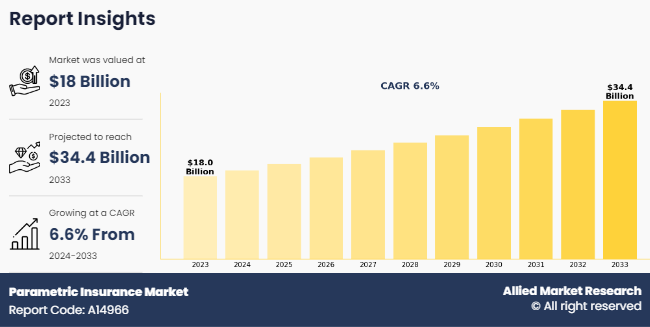

The market for parametric insurance is expanding rapidly as both institutional and retail participants recognize its efficiency. According to recent industry reports, the global parametric insurance market is projected to grow significantly through 2033, driven by increasing climate risks and the maturation of blockchain technology. This growth is not just about volume; it is about the deepening integration of these products into mainstream financial infrastructure.

No comments yet. Be the first to share your thoughts!