How parametric insurance works in DeFi

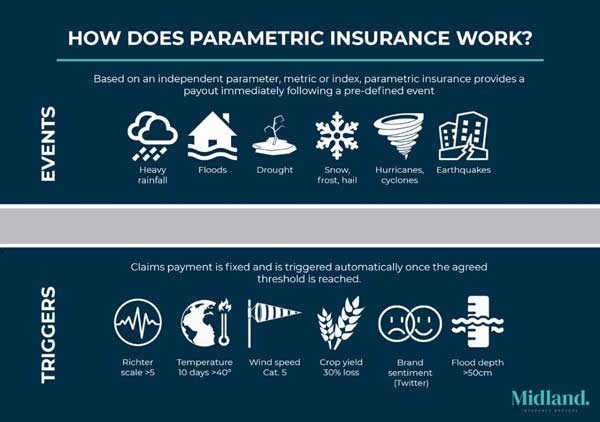

Parametric insurance replaces the slow, subjective process of traditional claims with a deterministic, index-based mechanism. In standard insurance, payouts are indemnity-based, meaning an adjuster must assess physical damage to determine value. Parametric insurance skips this entirely. Instead, it relies on a pre-agreed trigger—such as a specific price drop, a weather event threshold, or a smart contract exploit metric—to automatically release funds.

This shift is critical in DeFi, where speed and transparency are paramount. By using AI oracles to verify real-world data, parametric policies ensure that payouts are immediate and unbiased. There is no need for claims adjusters or lengthy negotiations. If the data matches the trigger condition, the smart contract executes the payout automatically. This eliminates counterparty risk and ensures liquidity is available exactly when the risk materializes.

The reliability of this system hinges on the quality of the data source. If the oracle feeding the trigger data is compromised or inaccurate, the entire mechanism fails. Therefore, selecting robust, decentralized oracle networks is as important as choosing the right trigger index. This approach transforms insurance from a reactive repair process into a proactive risk transfer tool, aligning perfectly with the automated nature of decentralized finance.

| Feature | Traditional Insurance | Parametric Insurance |

|---|---|---|

| Payout Trigger | Loss Assessment | Pre-defined Index |

| Claim Process | Manual Adjusters | Automated Smart Contract |

| Speed | Weeks to Months | Minutes to Hours |

| Subjectivity | High | None (Data-Driven) |

How AI Oracles Verify Real-World Events

Parametric insurance removes the friction of traditional claims by paying out based on predefined data triggers rather than physical damage assessments. In decentralized finance (DeFi), this mechanism relies entirely on AI-enhanced oracles to bridge the gap between on-chain smart contracts and off-chain reality. These oracles act as the nervous system of parametric products, continuously monitoring external data sources to verify events like weather patterns or market crashes with minimal latency.

The core challenge in parametric insurance is ensuring the integrity of the input data. AI oracles solve this by aggregating information from multiple independent sources, such as satellite imagery for crop yields or exchange price feeds for market volatility. Machine learning models then analyze this data to detect anomalies or verify that a trigger condition has been met. This automated verification process eliminates the need for human claims adjusters, reducing administrative costs and preventing fraud. As noted by industry leaders like Swiss Re, the reliability of these data feeds is the single most critical factor in the viability of parametric risk transfer.

To understand how these triggers function in practice, consider the volatility of crypto assets. A parametric insurance product might be designed to pay out if the price of Bitcoin drops below a certain threshold within a specific timeframe. The oracle monitors the price across several major exchanges, using AI to smooth out temporary spikes or "wicks" that don't represent a genuine market shift. This ensures that payouts are triggered only by sustained trends, protecting both the insurer and the insured from manipulation or noise.

The integration of AI into oracle networks also allows for more complex, multi-dimensional triggers. For example, a flight delay insurance product might not just look at the scheduled departure time but also factor in weather conditions, air traffic control data, and airline historical performance. AI models can weigh these variables to determine if a delay was caused by an insurable event (like a storm) or an operational issue (like crew scheduling). This nuanced analysis is what makes AI oracles superior to simple data feeds, providing the accuracy needed for high-stakes financial instruments.

Real-world DeFi coverage examples

Traditional indemnity insurance struggles in DeFi because proving loss requires forensic audits that take weeks or months. By the time a claim is settled, the capital is often gone. Parametric insurance solves this by using objective triggers—such as a stablecoin dropping below a specific peg or a price index hitting a volatility threshold—to release payouts instantly.

This approach turns complex risk transfer into a simple data verification problem. According to Swiss Re, parametric insurance expands coverage beyond physical assets to fill protection gaps left by traditional models, such as excluded perils or scarce adjusters. In DeFi, the "peril" is a smart contract exploit or market crash, and the "adjuster" is an oracle.

Flash loan and exploit protection

Flash loan attacks exploit price manipulation on decentralized exchanges. A parametric policy can monitor the spread between a DEX price and a trusted oracle (like Chainlink). If the spread exceeds a set percentage within a single block, the insurance triggers automatically. This protects liquidity providers from the immediate drain of capital without waiting for a community vote or legal ruling.

Stablecoin depeg events

Stablecoins are the backbone of DeFi, but they carry depeg risk. Instead of waiting for a protocol to prove insolvency, parametric coverage can be tied to the market price of the asset. If USDC or USDT drops below $0.95 for more than five minutes, the smart contract releases stablecoin payouts to affected wallets. This ensures immediate liquidity during crises, preventing cascading failures across lending protocols.

Extreme volatility hedging

For yield farmers, extreme volatility can liquidate positions even if the underlying asset recovers later. Parametric insurance can offer coverage based on volatility indices (like the CVOL index) rather than just price direction. If the 24-hour volatility of ETH exceeds 15%, payouts are triggered to cover liquidation costs or funding rate spikes, acting as a shock absorber for high-leverage strategies.

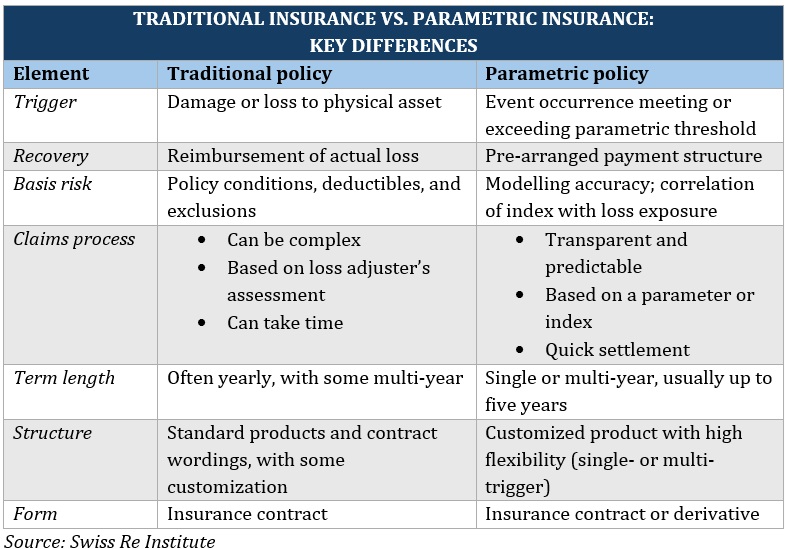

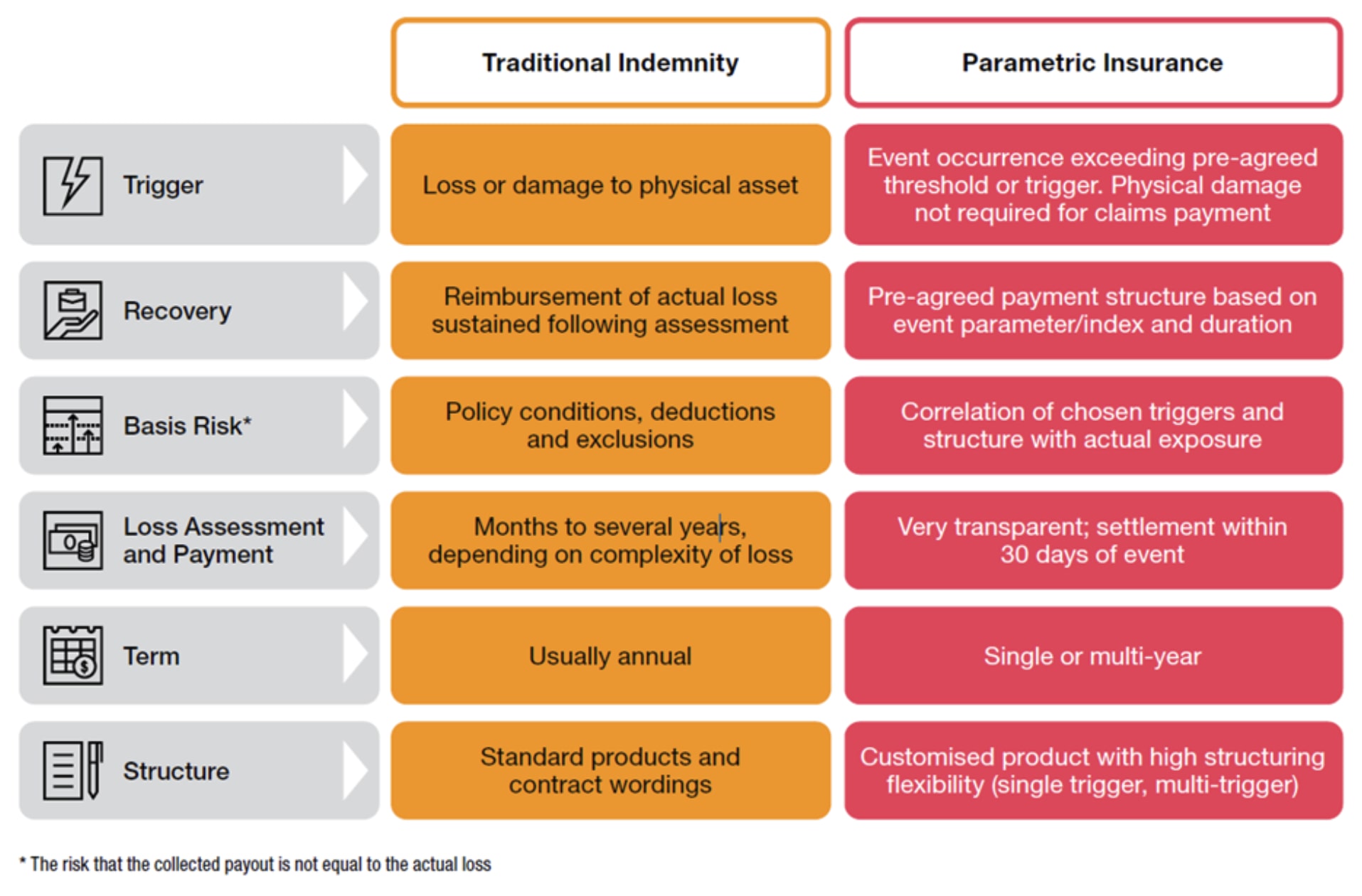

Traditional vs. Parametric DeFi Insurance

The shift from claims-based to trigger-based models changes the economics of risk. Traditional insurance is slow and opaque; parametric insurance is fast and transparent.

This efficiency makes parametric insurance a viable tool for high-stakes finance, where speed is as valuable as the payout itself. By removing the human element from claim assessment, protocols can offer coverage that is both affordable and reliable.

Designing a parametric insurance strategy

Building a parametric insurance strategy requires moving beyond generic coverage models to define precise, automated triggers. Unlike traditional insurance, which relies on claims adjusters to assess physical damage, parametric policies settle based on independently verified data points. This shift demands that protocol developers and users rigorously define the metrics that matter most to their specific risk profile.

The foundation of any parametric policy is the index source. For DeFi protocols, this often means selecting a reliable oracle network that feeds real-time market data. The source must be resistant to manipulation and capable of delivering data with low latency. Swiss Re notes that the reliability of the underlying data is the single most critical factor in preventing basis risk, where the payout does not align with actual losses.

Triggers must be binary and unambiguous. Instead of vague "market downturn" clauses, use specific metrics like a 20% drop in ETH price over a 1-hour window. This clarity ensures that smart contracts can execute payouts automatically without human intervention. Ambiguity in trigger definitions is the primary cause of dispute in parametric insurance, so precision is non-negotiable.

Determine the maximum payout cap based on your protocol’s liquidity reserves. Over-insuring can drain treasury funds during frequent, low-impact events, while under-insuring leaves you exposed to catastrophic risks. Use historical volatility data to model potential scenarios. The goal is to balance premium costs with the probability of a trigger event, ensuring the strategy remains economically viable over time.

To visualize the volatility that triggers these events, consider the price action of major assets.

When comparing different parametric insurance providers, focus on the mechanics of their oracle integration and payout speed. A comparison table helps clarify these operational differences.

| Provider | Oracle Source | Payout Speed | Min Coverage |

|---|---|---|---|

| DeFi Guard | Chainlink | < 24 hours | $100k |

| Risk Shield | Pyth Network | < 1 hour | $500k |

| Parametric Core | Custom Oracle | < 48 hours | $50k |

Finally, evaluate providers based on their track record in handling extreme market conditions. A robust parametric insurance strategy is not just about technology; it is about aligning financial resilience with operational reality. By following these steps, you can create a coverage model that protects your protocol without the bureaucratic delays of traditional insurance.

Common parametric insurance: what to check next

Does parametric insurance require claims adjusters?

No. Unlike traditional coverage, a parametric insurance guide reveals that these policies do not require physical damage assessments or claims adjusters to determine losses. Instead, claims are settled automatically based on independently verified data, such as wind speed or earthquake magnitude. This eliminates the lengthy appraisal process, allowing payouts to trigger as soon as the predefined parameters are met.

Can the data triggering a payout be manipulated?

Data integrity is the cornerstone of parametric insurance. Because payouts are tied to specific metrics, the reliability of the oracle is critical. Reputable providers use multiple independent data sources to prevent single-point failures. For context on how these financial instruments interact with broader markets, you can monitor the performance of related volatility indices below.

How does parametric insurance compare to traditional policies?

The main difference lies in the trigger mechanism. Traditional insurance pays based on the actual verified loss amount, which can take months. Parametric insurance pays a fixed amount when an external event occurs, regardless of the actual financial impact on the insured asset. This makes it ideal for liquidity needs rather than full replacement coverage.

| Feature | Traditional | Parametric |

|---|---|---|

| Payout Trigger | Actual verified loss | Predefined event data |

| Claims Process | Adjusters and appraisal | Automated data verification |

| Speed | Months | Days or hours |

No comments yet. Be the first to share your thoughts!