Why parametric insurance strategy matters now

DeFi protocols operate at the speed of code, but traditional insurance moves at the speed of bureaucracy. When a smart contract is exploited or a liquidity pool drains, the window to recover funds is measured in minutes, not months. This mismatch is why a parametric insurance strategy is no longer optional for serious risk management—it is essential.

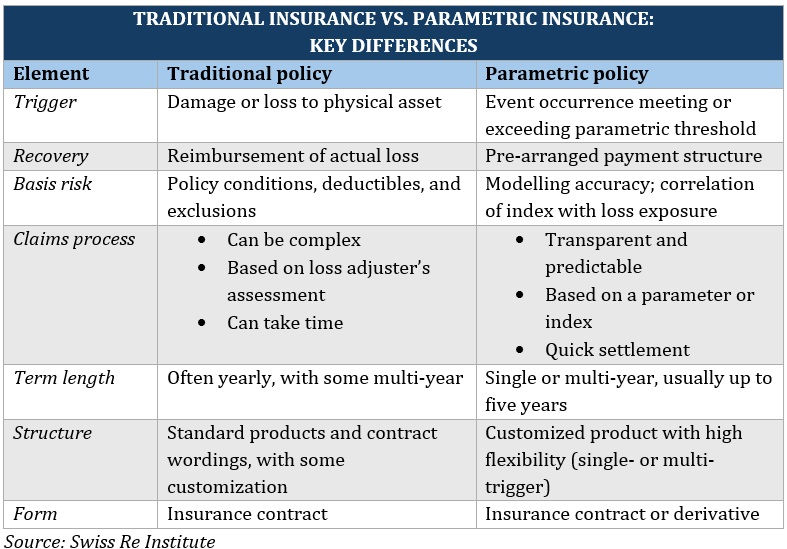

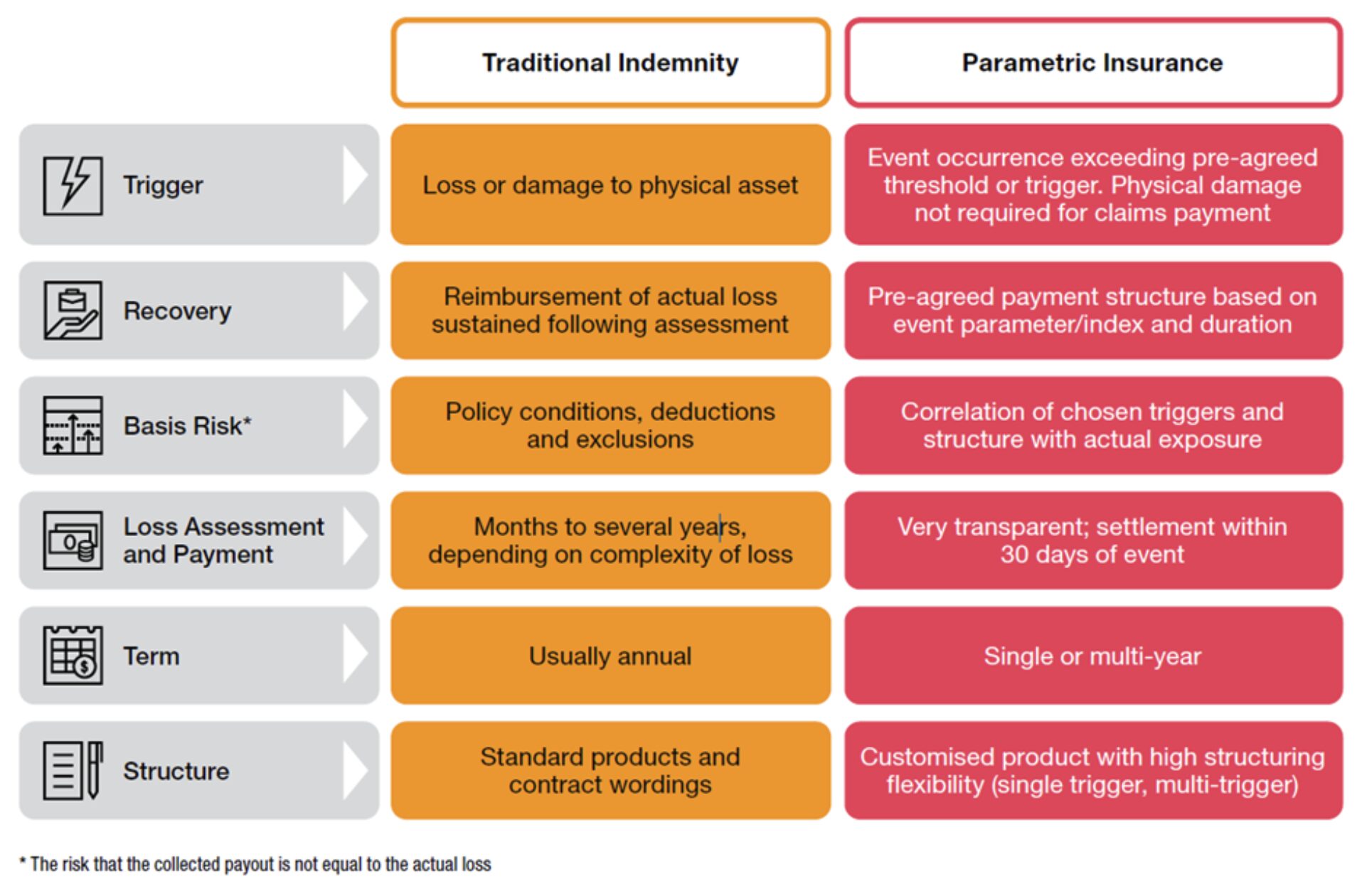

Unlike indemnity models that require lengthy claims assessments and loss verification, parametric insurance pays out automatically when a predefined trigger is met. According to the World Economic Forum, this model bolsters transparency and resilience by removing the ambiguity of subjective loss evaluation WEF. In the context of DeFi, that trigger might be a specific drop in token price, a confirmed exploit on a blockchain explorer, or a stablecoin depeg.

The result is immediate liquidity when it is needed most. For protocol treasuries and users alike, waiting weeks for an insurance payout often means the damage is already done. By integrating parametric coverage, you align your risk mitigation with the real-time nature of digital assets, ensuring that capital is available to stabilize operations or compensate users without delay.

Core components of onchain coverage

Building a parametric insurance strategy for DeFi risk requires shifting away from traditional claims adjustment. Instead of proving loss after the fact, the system relies on pre-agreed data triggers. This infrastructure rests on three technical pillars: oracles for data verification, smart contracts for logic execution, and precise trigger mechanisms that define exactly when coverage activates.

Oracles as the single source of truth

In traditional insurance, an adjuster visits a site. In DeFi, oracles provide the immutable data layer. These networks fetch external information—such as price feeds, volatility indices, or protocol TVL—and feed it on-chain. The security of your parametric insurance strategy depends entirely on the oracle’s integrity. If the data source is compromised or delayed, the payout logic fails. Most robust implementations use decentralized oracle networks to prevent single points of failure, ensuring that the data reflecting market conditions is accurate and tamper-resistant.

Smart contracts for automated execution

Once data arrives, the smart contract acts as the underwriter. It contains the immutable code that defines the policy terms. Unlike traditional contracts that require legal interpretation, these smart contracts execute automatically when conditions are met. This eliminates administrative overhead and human error. The code must be rigorously audited, as any vulnerability can be exploited not just for theft, but to manipulate the payout logic itself. The contract’s role is purely computational: verify data input, check against thresholds, and release funds if the criteria are satisfied.

Defining trigger mechanisms

The trigger is the specific condition that initiates the payout. It must be binary and objectively measurable. Common triggers in DeFi include price drops below a certain threshold, sudden spikes in network gas fees, or the failure of a specific protocol component. According to Aon, parametric coverage allows risk managers to clearly define events that will and will not pay claims, removing ambiguity. The trigger mechanism must be carefully calibrated to avoid basis risk—the danger that the index moves but the actual user loss does not, or vice versa.

Integration and latency

The final component is the integration layer that connects these elements. The oracle must deliver data to the contract within the required time window, and the contract must execute the payout transaction efficiently. High latency can turn a timely payout into a useless one, especially in fast-moving crypto markets. Therefore, the entire stack—from data feed to transaction confirmation—must be optimized for speed and reliability. This technical infrastructure transforms insurance from a reactive service into a proactive, programmable risk management tool.

Managing basis risk in DeFi protocols

Basis risk is the single biggest hurdle in building a reliable parametric insurance strategy. It happens when the trigger event occurs, but your protocol doesn’t suffer a proportional loss—or worse, when your protocol is drained, but the trigger never fires. This mismatch creates a gap between the insurance payout and the actual financial damage, leaving you underinsured or, in rare cases, overcompensated.

Think of basis risk as the distance between a thermometer reading and the actual temperature in the room. If the thermometer is broken or placed in the wrong spot, you can’t trust it to tell you when to turn on the AC. In DeFi, relying on a single, broad metric like total Ethereum gas prices to trigger a payout for a specific lending protocol’s liquidation cascade is a recipe for disaster. The metrics might correlate loosely, but they rarely move in perfect lockstep.

Mitigating this risk requires choosing triggers that closely mirror your protocol’s specific risk exposure. Instead of relying on generic market movements, look for data points that are intrinsic to your smart contract’s logic. For example, if your protocol is vulnerable to oracle manipulation, a trigger based on price divergence between your oracle and a decentralized data feed is far more accurate than a simple price drop threshold.

Research from Swiss Re and PwC highlights that parametric insurance expands coverage beyond traditional indemnity models, but it introduces this unique basis risk challenge. To build a robust strategy, you must rigorously backtest your triggers against historical events. Look for scenarios where the trigger fired but no loss occurred, or where a loss happened without a trigger. This historical analysis is the only way to calibrate your parameters for accuracy.

Ultimately, a parametric insurance strategy is only as good as its triggers. Don’t settle for convenience. Take the time to define metrics that are tightly coupled with your protocol’s actual vulnerability surface. This precision is what separates a functional insurance layer from a mere marketing feature.

Integrating DeFi risk transfer layers

A parametric insurance strategy works best when it sits inside a layered risk transfer stack. Instead of relying on a single coverage source, you can layer parametric triggers alongside traditional indemnity policies and reinsurance capital. This approach lets you target specific vulnerabilities—like smart contract failures or oracle manipulation—while leaving broader, hard-to-model risks to traditional markets.

Parametric contracts act as the first line of defense. Because payouts are triggered by objective data points, such as a price drop or a protocol exploit confirmation, they provide immediate liquidity. This speed is critical in DeFi, where protocol solvency can evaporate in minutes. Traditional insurance, by contrast, requires lengthy loss adjustment and verification processes that often leave protocols undercapitalized during the critical recovery window.

To understand the structural differences, compare how parametric and traditional indemnity models handle the core mechanics of risk transfer:

| Feature | Parametric | Traditional Indemnity |

|---|---|---|

| Payout Speed | Minutes to hours | Months to years |

| Basis Risk | High (trigger vs. actual loss) | Low (based on actual loss) |

| Transparency | High (on-chain data) | Low (private underwriting) |

| Cost Structure | Lower premiums, higher basis risk | Higher premiums, lower basis risk |

Integrating these layers requires careful calibration. If your parametric triggers are too sensitive, you face frequent basis risk where payouts occur without actual protocol damage. If they are too loose, you miss the liquidity needed during a crisis. The goal is to use parametric insurance for high-frequency, low-severity events where speed matters most, while reserving traditional reinsurance for catastrophic, low-frequency events that require deep capital reserves.

This hybrid approach mirrors how institutional investors manage portfolio risk. Just as a fund might use options for short-term hedging and long-duration bonds for stability, a DeFi protocol uses parametric triggers for immediate resilience and traditional layers for long-term solvency. By clearly defining which risks fall into which bucket, you create a robust defense that doesn't rely on the weaknesses of any single model.

Steps to implement your strategy

Building a parametric insurance strategy requires moving from abstract risk models to executable smart contract logic. This workflow guides protocol teams through the critical phases of design, testing, and deployment.

Begin by mapping the specific vulnerabilities your protocol faces. Unlike traditional insurance, parametric models require precise, measurable events. Define whether your primary risk is price volatility, oracle manipulation, or smart contract failure. This clarity dictates the entire structure of your coverage.

The integrity of your payout depends entirely on the data feeding your triggers. Choose established oracles with proven track records in your specific market segment. Avoid single-point failures by aggregating data from multiple reputable sources to ensure the trigger mechanism remains robust against manipulation.

Establish binary conditions that remove human judgment from the claims process. A trigger might be "ETH price drops below $1,500 on Uniswap for 15 minutes." These parameters must be indisputable. As noted in industry guides, this index-based approach allows claims to be paid within days, eliminating lengthy assessment periods.

Before locking capital, deploy your smart contracts to a testnet environment. Simulate extreme market conditions to verify that triggers activate correctly and payouts distribute as intended. This step is non-negotiable for high-stakes DeFi protocols, where code errors can lead to total loss of user funds.

Ensure sufficient liquidity is available to cover both premium collection and potential payouts. Structure your treasury to handle peak claim periods without causing solvency issues for the protocol. Consider dynamic premium models that adjust based on market volatility to maintain long-term sustainability.

No comments yet. Be the first to share your thoughts!